What is a Scottish Trust Deed?

A Trust Deed is a debt management solution for residents of Scotland, and it is an agreement that is legally binding between a debtor and creditors. The debtor agrees to repay an affordable amount during a specified period, and creditors agree to refrain from further action. It is similar to an IVA (which is available to residents of England and Wales) and is a formal type of debt management plan (DMP) based upon Scottish insolvency legislation.

This page features the Trust Deed questions we most frequently receive from Scottish residents seeking debt advice and the answers to each of them. If the information does not answer all of your questions, contact us to get a fast and courteous response.

The Trust Deed period usually runs for four years, and when it concludes, the debtor is not required to repay any balances for included unsecured debts further. Only a licensed Insolvency Practitioner can establish a Trust Deed. If enough creditors do not object to a Trust Deed, the agreement becomes protected, binding the creditors and the debtor to the arrangement.

Find Out If A Trust Dead Is The Right Solution For You

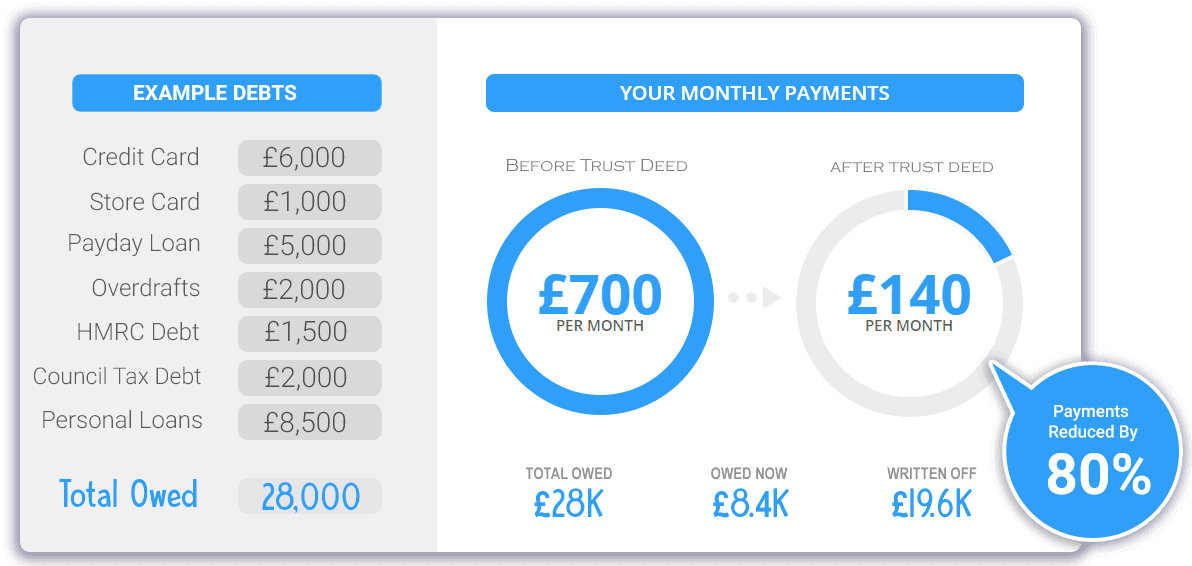

What A Typical Trust Deed Might Look Like

It takes only four steps to establish a Trust Deed using Jubilee Debt Management:

Step #1: Contact us so a debt management expert can discuss and review your financial situation. Our debt professional will request information about your income, expenses, and creditors. Based on this information, we’ll be able to advise you whether a Trust Deed is a suitable debt management solution. These details will also be used to calculate an affordable monthly payment for unsecured debts after accounting for living expenses and secured debt payments.

Step #2: Have an in-person or telephone meeting with our recommended Scottish insolvency practitioner professionals. This expert will review the Trust Deed process, answer your questions, and provide you with a Trust Deed proposal. After reading and confirming that you understand this document, you will be asked to approve it.

Step #3: The appointed insolvency and debt management expert will provide the Trust Deed proposal details to your unsecured creditors. The information will also be made publicly accessible via the Register of Insolvencies. This provides an opportunity for your creditors to object to your Trust Deed within the five-week period allowed to them.

Step #4: If fewer than 50 percent of creditors in number, or those who represent less than one-third of the debt, object within the five-week timeframe, your Trust Deed is granted legal protection (a “protected trust deed”).

You’ll then carry on making the agreed payments during the Trust Deed period in order to be discharged from the included debts when the Trust Deed concludes.

Why Do People Use A Trust Deed?

As a debt management solution, a Trust Deed offers several benefits. Monthly payments can be customized for the financial situation of the debtor in line with affordability. The Insolvency Practitioner serves as the contact person for the Trust Deed, providing knowledgeable assistance and support.

A Trust Deed provides the debtor with a defined date that included debts will be repaid or discharged. With a Trust Deed in place, a debtor does not feel as much pressure from creditors regarding possible legal action.

Another attractive benefit is that a Trust Deed does not require court attendance. It helps consumers handle their debt without recourse to sequestration (bankruptcy). Some people may find that a trust deed is less professionally damaging than bankruptcy. Homeowners are not necessarily required to sell their homes to enter into a Trust Deed, though equity in such assets will need to be dealt with.

Why Is An Insolvency Practitioner Required For A Trust Deed?

Formal insolvency like a Trust Deed requires oversight by someone qualified and experienced in these matters. A licensed Insolvency Practitioner, or IP, is often also a solicitor or an accountant and as such, this person has the knowledge and skills required. The IP will prepare a Trust Deed that is in the best interest of the debtor and creditors, present this to the creditors, and oversee the Trust Deed through to completion.

Why Would A Creditor Want To Accept My Trust Deed?

Creditors may feel comfortable that the Insolvency Practitioner will prepare a Trust Deed that considers their interests in addition to yours. They realize that they may receive more money from a Trust Deed than through an alternative debt management solution like sequestration. A Trust Deed also allows them to avoid legal action, which can be time-consuming and very expensive.

How Much Does A Trust Deed Cost?

The cost of a Trust Deed is typically based on how much the debtor can afford after daily living expenses and priority debts are paid. Therefore your budget will be restricted during the period that you’re in this type of debt management arrangement.

If creditors think a debtor is spending too much money on non-essential items, they may ask the debtor to reduce budgeted spending in these areas. To increase the sum of money available, homeowners with equity in their properties may have to release some equity from their home.

Trust Deed costs and fees are deducted from payments made by the debtor. Before committing to a Trust Deed, the debtor knows how much must be paid based upon their circumstances at the time. Creditors are aware of how much they are likely to receive.

Once you stop paying your creditors directly, it’s likely that you will fall into arrears or further into arrears on your credit accounts.

Is Four Years The Standard Term?

Most Trust Deeds now last for four years, but there are exceptions. A Trust Deed period may be extended in certain circumstances.

As A Homeowner, What Can Happen To My Property With A Trust Deed?

If the IP determines that you have equity in an asset that you own, you may have to release equity in that asset. If you’re a homeowner with equity, you will need to carefully consider how this equity amount will be raised in the future, or your home may be placed in jeopardy. The Trust Deed will only cover unsecured debts. Secured debts, like a mortgage, will be not become included, so payments toward these must continue.

What Are The Consequences Of Defaulting On Monthly Payments?

The consequences of payment default vary. If failure to pay is not the fault of the debtor due to situations like a pay decrease or temporary unemployment, the monthly payment figure may be reviewed and could be changed. The Trust Deed period could be extended, so the debtor has time to make up for payments missed.

If payments were missed because the debtor is uncooperative, the Trust Deed might be terminated. This will remove the legal protection, and the debtor will need to find another debt management solution or repay the debts.

Where a trust deed fails, this might result in the contributions made being accounted for (partially or in full) by the trust deed fees. It might also result in the debtor becoming bankrupt.

After A Trust Deed Ends, What Happens?

Once the debtor has completed their obligations to their Trust Deed and the debtor has been discharged, the included debts are considered satisfied. Any covered liability that remains outstanding is written off so the debtor will not have to pay it. Any debts that aren’t included in a Trust Deed will remain unpaid.

Does My Ability To Receive Credit Get Affected?

A trust deed does not result in an obligation not to take on further credit.

A trust deed is recorded on your credit file and will remain there for a total period of six years. It will significantly affect your ability to get credit and the terms upon which credit might be offered to you.

However, the fact that debts are cleared will also later be reflected in the report. If a Trust Deed were not used, these debts could have remained or even grown. Therefore, though a Trust Deed damages the credit rating, the harm done by doing nothing or using a debt management solution involving a longer-term might have a longer-lasting effect.

Six years from the Trust Deed effective date, mention of the Trust Deed and the debts it covered should be removed from the credit report.