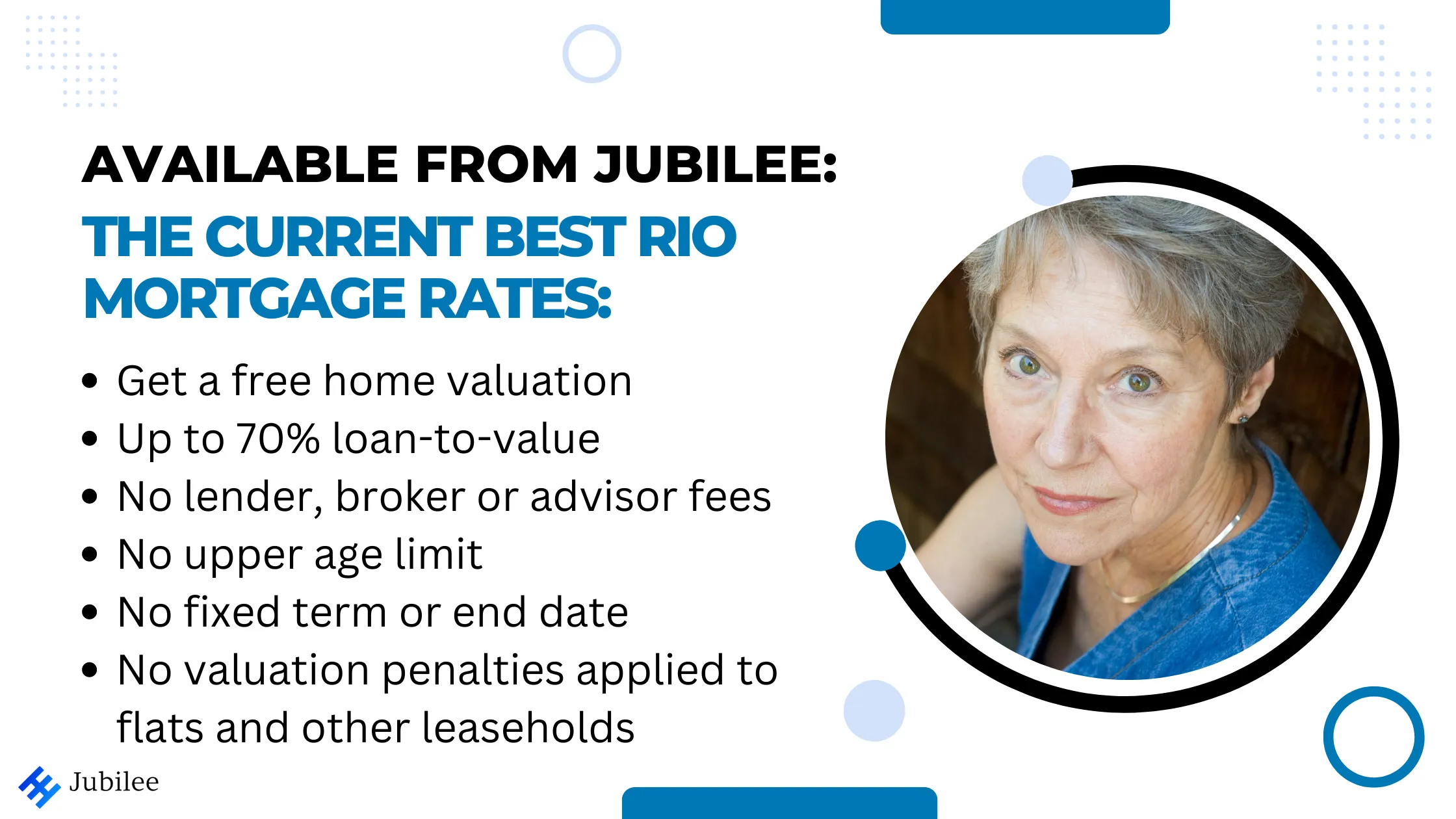

Available from Jubilee 2000, the current best RIO Mortgage Rates are as follows:

- 4.81% Fixed for life, so there are affordable monthly payments

- Ideal to pay off an existing mortgage that has come to the end of its term

- Free desktop automated home valuation – no in-person visit required

- No penalties for flats and other leasehold titles – full market value applied

- No application fee

- A direct lender, so no broker or advisor fees

- Up to 70% loan-to-value

- Interest-only or repayment mortgage payments

- No early repayment charges

- Portable mortgage ready if you need to move

- No upper age limit or mortgage term

- Ideal for IHT and other tax planning

- Remortgage your existing home or move and buy a new home

- Fast completions in as little as two weeks

- A decision in principle can be given based on a soft credit search

For example, if your home is worth £310,000, you can borrow £217,000, interest-only or repayment.

"*" indicates required fields

Many interest-only mortgage holders are reaching retirement and need a way to repay or replace their existing mortgage. Retirement interest-only (RIO) mortgages are designed for that purpose.

RIO mortgages can suit retirees with a reliable income but limited accessible cash. Comparing rates, fees and loan-to-value limits helps you find the right deal.

Jubilee 2000 compares later-life mortgage options across the market, including interest-only deals for retirement borrowers.

Lenders now offer more products for later life, so careful comparison matters.

That includes standard RIO mortgages, interest-only remortgages and fixed-rate options.

IN SUMMARY – Retired Mortgages Interest-Only Products:

- An overview of retirement interest-only mortgages in the UK, including smaller building societies.

- How to compare rates and products for retirement planning.

- The difference between fixed and variable options.

- What to check in the terms before applying.

- How market trends can affect available rates.

- Why provider comparison matters.

- How to choose a deal that fits your long-term plans.

Comparing Best RIO Mortgage Rates in the UK

When comparing RIO mortgages, look at the rate, fees, loan-to-value limit and affordability rules.

The lowest rate is not always the best deal if the product fee is high or the criteria do not suit you.

The aim is to find a mortgage that supports your retirement plans without creating unnecessary cost or risk.

| Building Society Lender | RIO Mortgage Rate | Loan to Value Ratio | Affordability Criteria | Product Fees |

|---|---|---|---|---|

| Buckinghamshire Building Society | 5.42% | 60% | Income proof required | £999 |

| Family Building Society | 4.92% | 75% | Pension statements | £1,499 |

| Hanley Building Society | 4.16% | 70% | Asset assessment | £749 |

| Hinckley and Rugby Building Society | 4.06% | 50% | Expenditure review | No fees |

Comparing these details helps narrow the shortlist quickly.

Choosing a later-life mortgage is a major retirement decision, so rate comparison should always sit alongside affordability and suitability.

Key Factors That Influence RIO Mortgage Rates

RIO mortgage pricing depends on your circumstances and on wider market conditions.

Age and Eligibility Criteria for the Best Lifetime Interest-Only Mortgage Rates

RIO mortgages are aimed at older homeowners, often aged 55 or over. Lenders assess age, eligibility and sometimes health when setting terms.

Income Verification and Affordability Checks to access the best retirement mortgage rates

Lenders check pension income, investments and regular outgoings to confirm the mortgage remains affordable.

Property Value and Loan-to-Value Ratios for an over-55 interest-only mortgage

Your property value and loan-to-value ratio also affect the rate. Lower borrowing against higher equity usually attracts better pricing.

| Loan-to-Value Ratio | Typical Interest Rate Range | Comments |

|---|---|---|

| Less than 40% | 2.05% – 3.62% | Typically enjoys the lowest rates due to high equity. |

| 40% – 60% | 3.15% – 4.13% | Moderate equity, moderate rates. |

| 60% – 75% | 3.41% – 5.19% | Higher rates reflect increased lender risk. |

In most cases, stronger affordability and lower LTV improve the options available.

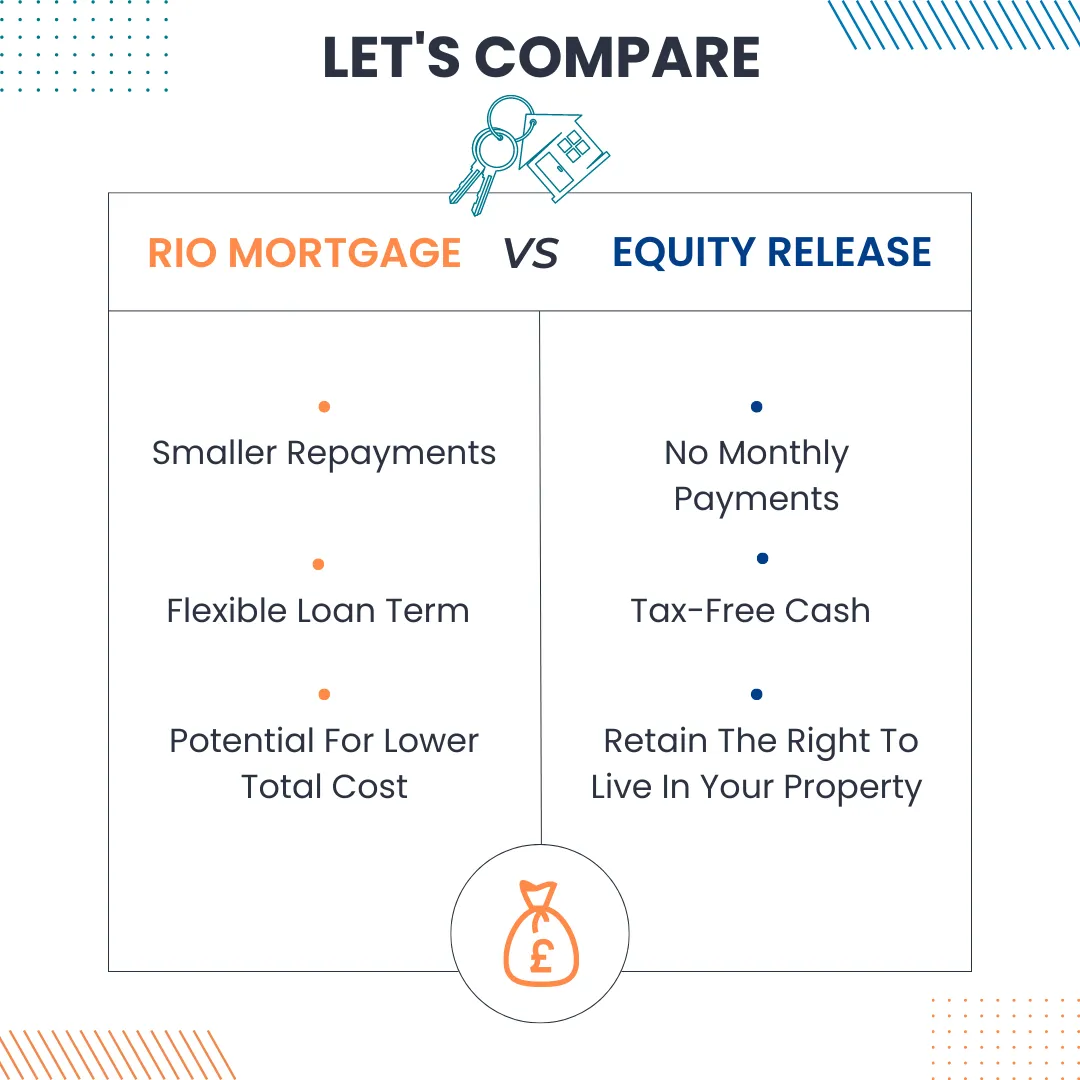

Assessing Retirement Mortgage Options and Other Interest-Only Lifetime Mortgage Providers

Retirement borrowing can include RIO mortgages, lifetime mortgages and drawdown plans. The right choice depends on income, objectives and estate planning.

Lifetime Mortgages Explained with and without monthly interest payments

Lifetime mortgages release equity from your home. Some allow monthly interest payments, while others roll interest into the loan balance.

The Flexibility of Drawdown Plans Detailed By A Mortgage Broker

Drawdown plans let you take funds in stages rather than as one lump sum. This can reduce unnecessary interest build-up.

Impact of Health Conditions on Mortgage Offers and the best Rio mortgage providers’ interest rates

Health and lifestyle can affect some later-life mortgage offers, especially in the equity release market.

| Mortgage Type | Key Feature | Advantages | Considerations |

|---|---|---|---|

| Retirement Interest-Only Mortgage Hodge Bank | Interest-only payment | Lower payments during retirement | Requires regular income |

| Lifetime Mortgage Leeds Building Society | Loan secured against home | No monthly payments; interest compounds | Reduces inheritance |

| Drawdown Lifetime Mortgage Mansfield Building Society | Withdraw funds as needed | Flexibility; control over loan size | Interest may accumulate quickly if large sums are drawn |

Each option solves a different problem, so it is worth comparing them before deciding.

Understanding equity release options and Home Reversion Plans VS mortgages for pensioners, interest-only for repayment of a standard residential mortgage

Equity release lets older homeowners access money from their property while continuing to live there.

The two main types are lifetime mortgages and home reversion plans.

With a lifetime mortgage, you borrow against your home, and the balance is usually repaid when the property is sold after death or a move into long-term care.

With home reversion, you sell part or all of the property in return for cash while keeping the right to remain in the home.

Both options can affect inheritance, so independent advice is important.

When comparing home reversion and lifetime mortgages, focus on ownership, long-term cost and the impact on your estate.

Now, let’s look at who can get these plans:

- Home reversion plans usually need you to be at least 65.

- Lifetime mortgages are available to people aged 55 and over.

- Your property should be your main home and worth at least £70,000.

It is also worth checking how these plans could affect means-tested benefits or taxes.

Private pension income can help some borrowers pass affordability checks for RIO mortgages.

A RIO mortgage may also suit borrowers who want to improve their home or help family without selling.

The Role of Loan-to-Value in RIO Mortgages and Existing Customers

Loan-to-value affects both the rate and the amount you can borrow on an RIO mortgage.

Lower LTV usually means lower risk for the lender and better pricing for the borrower.

Let’s look at a comparison:

| Criteria | Fixed for Life Rates | Variable Interest Rates |

|---|---|---|

| Stability of Payments | High stability with consistent payments | Variable, with the potential for both increases and decreases |

| Response to Market Changes | Often higher due to the locked-in rate | Rates can fluctuate according to market conditions |

| Long-term Financial Planning | Ease of budgeting and financial forecasting | Requires contingency plans for rate changes |

| Early Repayment Charges | This could result in savings if interest rates decrease | Typically lower or non-existent |

| Overall Cost Effectiveness | Potentially more expensive long-term if market rates fall | Could result in savings if interest rates decrease |

Fixed-for-life rates can offer certainty, while variable rates may offer more flexibility.

Top RIO Mortgage Providers Catering to Seniors

Comparing providers means looking beyond the headline rate.

Fees, flexibility, service and underwriting approach can all make a difference in later life.

Holistic Comparison of RIO Mortgage Lenders

A useful comparison reviews terms, fees, criteria and how well a lender understands retirement borrowing.

Profiles of Market-Leading RIO Mortgage Providers

Some lenders stand out for flexibility, others for pricing or customer support.

| Provider | Interest Rates | Products Offered | Customer Reviews | Additional Services |

|---|---|---|---|---|

| Marsden Building Society | Competitive fixed, variable rates | Range of RIO mortgage options | High satisfaction, support quality | Equity release advice |

| Melton Building Society | Tailored rates for individuals | Flexible drawdown facilities | Positive feedback on advisor expertise | Pension planning services |

| Newbury Building Society | Market-adjusted rates | Bespoke mortgage solutions | Commendable customer care | Retirement planning |

The best provider for you will depend on your income, equity, objectives and preference for flexibility.

How to Qualify for the Best RIO Mortgage Rates

Strong affordability, clear documentation and realistic borrowing needs all help when applying for a RIO mortgage.

Navigating the Application Process: Unlike standard mortgages for retired borrowers

Start by reviewing lenders, rates and criteria. Then check your retirement income, property value and likely loan size.

Advice can help if you are unsure which RIO mortgage, remortgage, or equity release product is more suitable.

You should also be ready to explain how the capital will be repaid, typically through the future sale of the property.

Essential Documentation for Mortgage Approval

Lenders usually want evidence of income, identity, property value, credit history and existing debts.

| Document | Description | Reason for Requirement |

|---|---|---|

| Proof of Income | A recent report from a trusted agency. | To show you can pay the interest. |

| Identification | Valid passport or driving licence. | For identity and legal status checks. |

| Property Valuation | Current property market value appraisal. | Important for setting loan terms. |

| Credit Report | Recent report from a trusted agency. | To evaluate your credit history. |

| Debt Information | Info on mortgages or large debts. | For a full financial review. |

| Repayment Strategy | A detailed loan repayment plan. | To ensure you borrow responsibly. |

Having these ready can speed up the application and reduce avoidable delays.

Interest-only lifetime mortgages and interest-only equity release

These options can help later-life borrowers stay in their home, release funds or manage retirement borrowing more efficiently.

They should always be weighed against long-term cost and effect on inheritance.

Financial institutions that offer interest-only lifetime mortgages

One of the main lenders for later life mortgages is Santander.

Exploring Interest-Only Mortgages for Over 60s

Interest-only mortgages can help some over-60s reduce monthly outgoings because only the interest is paid each month.

They can support cash flow in retirement, but the capital must still be repaid later.

- Eligibility criteria usually include age, property value, income and the proposed repayment plan.

- Risk centres on how the capital will be repaid in future, often through the sale of the home or the estate.

- Benefits can include lower monthly payments and more flexibility in retirement.

These mortgages should be considered alongside pensions, savings and wider retirement plans.

Advice can help you judge whether they fit your long-term needs.

| Benefits | Considerations | Eligibility Criteria for later life mortgages |

|---|---|---|

| Lower monthly payments | Repayment of loan capital | Minimum age requirement |

| Flexibility for other investments | Potential impact on inheritance | Equity in property |

| Preservation of capital | Interest rate fluctuations | Proof of income/financial stability |

Any later-life mortgage needs careful planning, especially if health, housing needs or care costs may change.

For the right borrower, an interest-only mortgage can still be a practical option.

Costs Associated With Retirement Mortgages

Retirement mortgages can involve arrangement fees, valuation fees, legal costs and, in some cases, advice fees or early repayment charges.

Assessment of fees with Santander Retirement Interest-only mortgages

Fees vary by lender, so compare the full cost and not just the rate.

Evaluating the Long-term Impact of Costs on Your Finances with the best retirement interest-only mortgage rates

Even modest charges can add up, especially over longer terms.

Here’s a table showing how fees can accumulate, impacting your mortgage’s total cost:

| Fee Type | One-time Costs | Recurring Costs | Total Impact |

|---|---|---|---|

| Arrangement Fee | £1,500 | N/A | £1,500 |

| Advice Fee | £500 | N/A | £500 |

| Valuation Fee | £300 | N/A | £300 |

| Legal Fees | £850 | N/A | £850 |

| Annual Service Charge | N/A | £50 | £500 (over 10 years) |

| Early Repayment Charge | Varies* | N/A | Varies* |

| Total Estimated Cost | Costs can exceed £3,650, exclusions apply. | ||

*Early repayment charges vary based on the loan balance and remaining mortgage time.

| RIO Mortgage Feature | Relevance to Demographic Changes | Future Adaptations and the maximum loan |

|---|---|---|

| Flexible Repayments Nottingham Building Society | Meets the need for adjustable budgeting in retirement – just the interest is payable | Adapt to pension fluctuations and economic trends but still subject to the lender’s affordability assessment. |

| Inclusive Eligibility Penrith Building Society | Addresses the diverse financial situations of retirees | Broaden to accommodate a wider age range and equity levels |

| Early Repayment Options Saffron Building Society | Security of remaining in the home despite financial shifts | Introduce more flexible penalties or penalty-free periods |

| Lifetime Tenure Scottish Building Society | Broaden to accommodate a more comprehensive age range and equity levels | Align mortgage tenure with increasing life expectancy |

A low monthly payment with no maximum age limit – the key is a good credit history

Later-life lending is evolving, with more flexible products for older borrowers.

Good preparation and realistic affordability remain central to a successful application.

Use equity tied up in your home to get financial freedom with no maximum age limit

Your home equity, income and future plans will all affect which retirement mortgage is most suitable.

Comparing lenders and taking advice can help you avoid an unsuitable deal.

Get a free valuation on your current home before long-term care

A valuation is often one of the first steps in understanding how much you may be able to borrow.

Other things to consider that are important:

- Do you want to repay the mortgage early?

- Would a mainstream lender be suitable?

- Do your bank statements show gambling activity?

- Would you want to move home later?

- Could pension savings be an alternative?

- How could means-tested benefits be affected?

- Would a standard mortgage product be better?

- Is your lender or broker authorised by the Financial Conduct Authority?

FAQ for A Repayment Mortgage or the main Rio Mortgage Deals

What are the benefits of choosing a RIO mortgage from the Suffolk Building Society?

A RIO mortgage can offer lower monthly payments than repayment borrowing and may suit retirees who fall outside standard mortgage criteria.

How do Tipton and Coseley Building Society RIO mortgages address the challenges of interest-only mortgages?

They are designed for borrowers who need an interest-only solution in retirement, with repayment usually coming from the future sale of the property.

How do age and eligibility criteria impact Vernon Building Society RIO mortgage rates?

Age, income, property type and overall eligibility all affect the rate and terms a lender may offer.

What is the role of income verification and affordability checks in Beverley Building Society RIO mortgages?

Lenders use them to check that the monthly interest payments are affordable over the long term.

How do property value and loan-to-value ratio affect Ipswich Building Society RIO mortgage rates?

Higher equity and lower LTV usually improve pricing, while higher borrowing can push rates up.

How does the loan-to-value ratio impact Loughborough Building Society RIO mortgage rates?

A lower LTV generally means less lender risk and can lead to better rates.

What are the pros and cons of fixed-for-life rates in Bath Building Society RIO mortgages?

They offer payment certainty, but may cost more overall if market rates fall later.

Which are the top RIO mortgage providers catering to seniors?

Suitable providers depend on your circumstances, but the comparison should focus on rates, fees, flexibility, and service.

How can I qualify for the best RIO mortgage rates?

Strong affordability, clear documentation and careful lender comparison can all improve your chances of getting a better deal.

Are there Saga interest-only mortgages available for individuals over 60?

Some later-life lenders offer products aimed at older borrowers, but availability depends on current lending criteria.

What costs are associated with retirement mortgages?

Common costs include arrangement fees, valuation fees, legal fees and possible early repayment charges.

How does your credit score impact mortgage rates?

A stronger credit profile can improve the products and pricing available.

What are the innovative Buckinghamshire Building Society mortgage solutions for later life plans?

Later-life lending now includes more flexible products such as RIO mortgages, lifetime mortgages and drawdown options.