The buzz in the property market often overlooks a key fact that affects many who are about to retire. Nearly one in ten retirees depends on their property’s value to fund their retirement, as pensions shrink and living costs soar.

Now, retirement mortgages stand out as a vital part of ensuring a stable financial future in your retirement years.

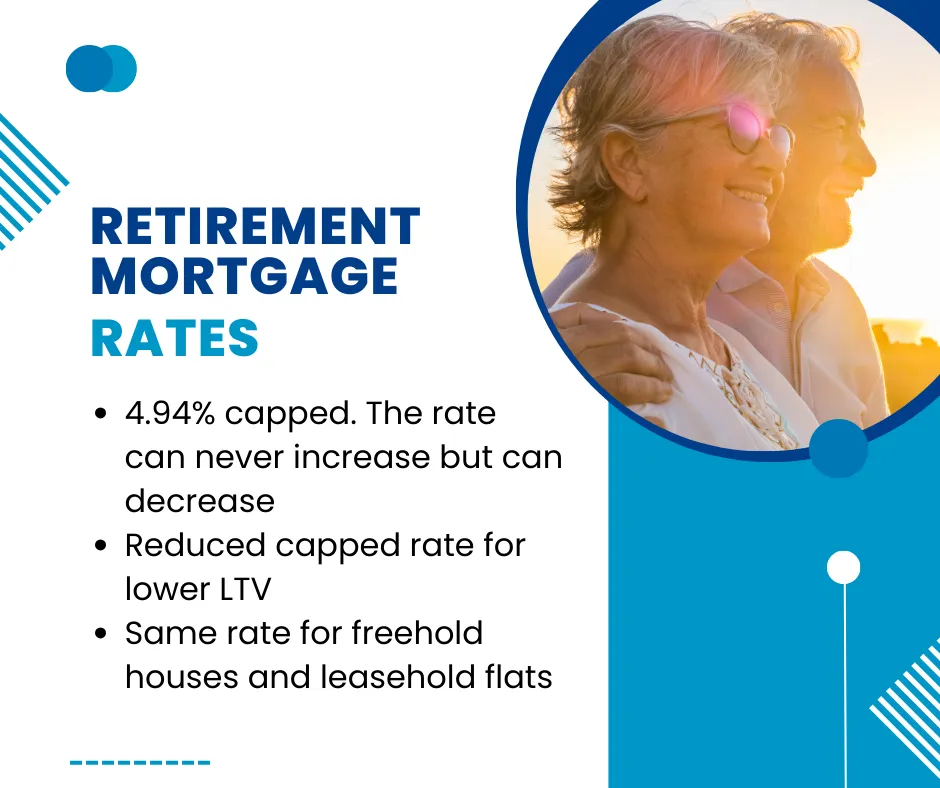

You can borrow up to 70% of the valuation of your home. So, for example, if your home is worth £200,000, you can borrow £140,000.

Some features include:

- New direct lender from 1st March 2026 is not available on comparison sites

- No broker or advisor fees

- No lender fees

- 70% loan-to-value

- Free automated desktop-based home valuation

- Full open market value applied to flats and other leaseholds

- Interest-only or repayment options

- No early repayment charges

- Portable product if you need to move house

- 4.94% fixed for life

- No upper age limit

- Many non-standard construction properties are considered

- Ideal for IHT and other tax planning

- Remortgage or property purchase

- Fast completions, sometimes as fast as 2 weeks

- The decision, in principle, is based on a soft credit search

"*" indicates required fields

As we live longer and our lifestyles change, our retirement planning must evolve too. Retirement mortgages have moved from a niche idea to a key strategy for a comfortable retirement.

They can offer a much-needed boost to your pension, providing peace and security in your later years. We must understand how these financial options can benefit us.

These days, more retirees are looking for innovative ways to maintain their standard of living. Retirement mortgages open up these opportunities by using the equity in their homes.

Let’s look at the various options and how they work. This could be the key to stable retirement planning:

Important points to consider:

- Retirement mortgages offer a financial lifeline to retirees by releasing equity from their property.

- The rise in property wealth among retirees highlights the potential of retirement mortgages to secure a comfortable lifestyle.

- With careful planning, retirement mortgages can enhance one’s financial stability and peace of mind during the golden years.

- Understanding the options and navigating the complexities of retirement mortgages is crucial for a secure financial future.

- Retirement mortgages are integral to retirement strategies, granting flexibility and control over financial resources in later life.

Understanding Retirement Mortgages: What You Need to Know

Retirees must understand retirement mortgages to maintain financial stability. These financial tools are unique and crucial during retirement. They help retirees better manage their money.

The Essence of Retirement Mortgages

Understanding retirement mortgages means knowing they’re for later life. The essence of retirement mortgages is that they allow homeowners to tap the value of their property to fund their retirement.

How Equity Release Could Benefit Retirees

Equity release is a key advantage. It’s financial help when regular income isn’t enough. The benefits of equity release include supplementing pensions and funding home repairs or unexpected costs.

The Eligibility Criteria for Retirement Mortgages

Understanding who can get a retirement mortgage is crucial. It depends on age, property value, and income.

| Eligibility Criteria | Typical Requirement | Details to Consider |

|---|---|---|

| Minimum Age | 55-60 years | Varies between lenders |

| Property Value | Typically £70,000 or more | Assessed by an independent valuer |

| Income Assessment | For interest-only options | Ensuring the affordability of interest payments |

First Direct’s Approach for Over 70’s Mortgages

First Direct understands that for retirees, a mortgage is more than just a financial product; it’s a key component of their overall retirement planning strategy. – First Direct representative on retirement solutions.

Below, we highlight First Direct’s mortgage options for those aged 70 or over. We outline the benefits, aiming to help retirees make informed choices for their unique situations.

| Feature | Benefit | Detail |

|---|---|---|

| Flexible Repayment Options | Customisable Installments | Retirees can choose how much they repay each month, adjusting to their disposable income. |

| Borrower Age Limit | Inclusive Lending Policy | High age limit, acknowledging rising life expectancy, allowing for longer-term planning. |

| Property Eligibility | Wide Property Acceptance | Includes a variety of property types to ensure many retirees can qualify. |

| Advice and Support | Personalised Assistance | Dedicated specialists offer guidance throughout the mortgage process. |

Mortgages for over 70’s can seem complex. Yet, companies like First Direct provide detailed options for this life stage. These products help ensure a financially secure retirement.

Understanding these mortgages helps First Direct deliver excellent service. It shows their dedication to retirees’ financial well-being.

Maximising Retirement Security Through Property Equity

Retirement security is important for many. As we enter our senior years, financial independence becomes essential. Property equity offers a ray of hope for retirees who wish to use their home’s value.

Benefits of Using Home Equity as Retirement Income

Using home equity for retirement can offer several advantages. It turns the wealth in your home into accessible money. This can boost your pension income, improve your house, or allow for a more exciting lifestyle. Home equity’s flexibility stands unparalleled.

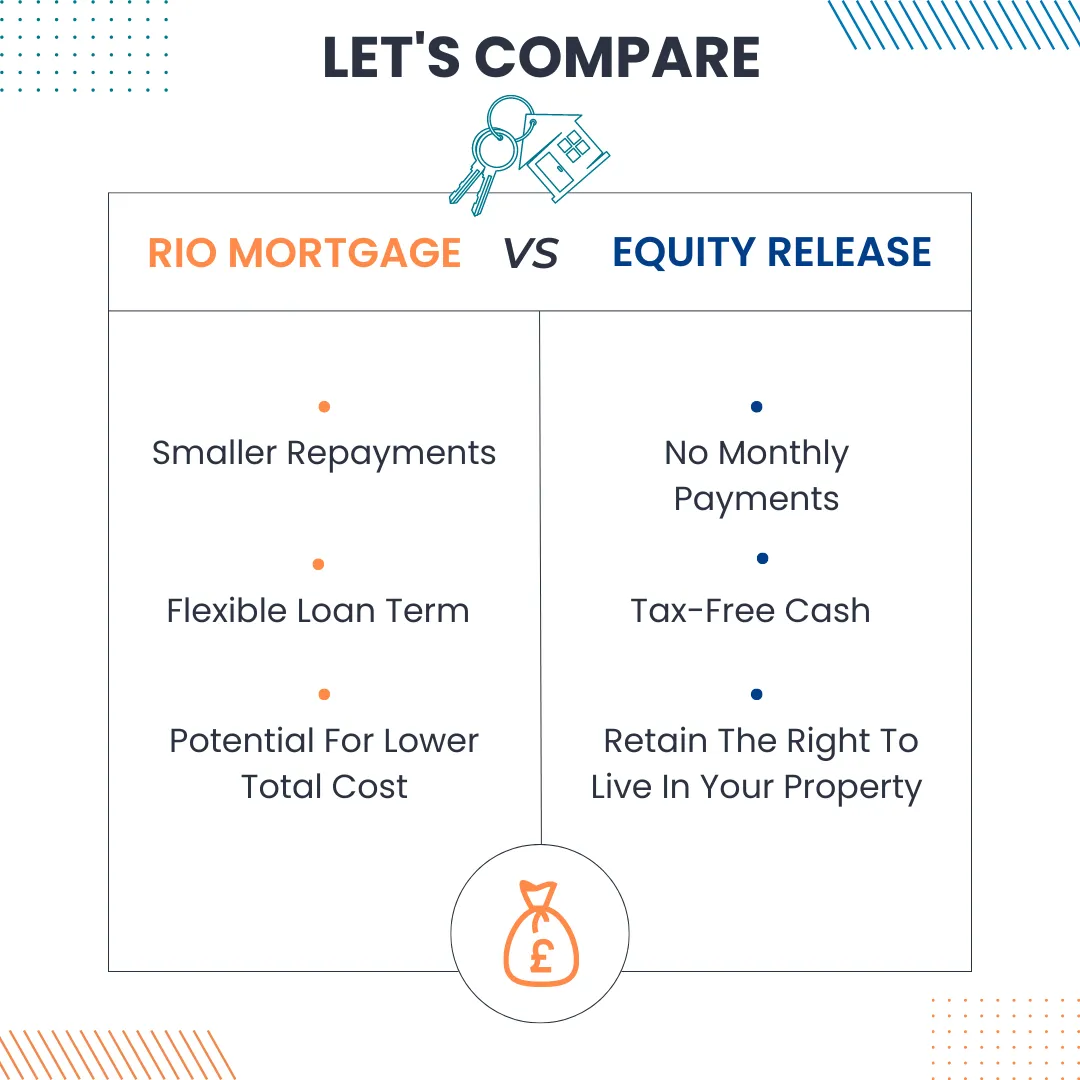

- Tax-free cash flow: Money from home equity is usually tax-free. You can enjoy the full amount.

- No monthly repayments: Some equity release plans don’t require monthly repayments, reducing financial stress for retirees.

- Stay in your home: Many schemes let you retain your home while benefiting from its value, without needing to move.

Impact on Long-Term Financial Stability

Incorporating home equity in retirement planning can make your finances more secure. It’s a strategy for lasting stability, not just a quick fix. This ensures peace of mind in your retirement years.

| Aspect of Stability | Home Equity Contribution | Regular Income Alternatives |

|---|---|---|

| Certainty of Funds | Substantial lump-sum or regular payouts | Variable, subject to investment risks |

| Flexibility | Adapt payments to suit changing needs | Fixed annuity payments are less adaptable |

| Legacy | Option to ring-fence inheritance | Dependent on investment performance |

Using property equity is like grabbing a lifeline to financial safety. An innovative plan for home equity as retirement income helps maintain economic strength. It allows retirees to protect their lifetime achievements and enjoy stable finances in later life.

The Comparative Benefits of Different Retirement Mortgage Products

Exploring retirement mortgage products is key to finding the right match. Each option has unique benefits that can suit various financial plans. It helps retirees make choices that best fit their needs.

Lump-sum lifetime mortgages give retirees a large one-time payment. This can be used for big purchases, paying down debt, or improving life in retirement. It’s an attractive option for those needing a large sum upfront.

Drawdown lifetime mortgages allow retirees to withdraw funds in instalments. This means interest accumulates only on the money taken out, leaving more of the property’s value intact. It’s a flexible way to manage funds and save equity.

Retirement interest-only mortgages let borrowers pay only the interest monthly, leaving the loan’s principal untouched. Suitable for retirees with steady incomes, it helps keep the estate value for heirs. A good fit for those wanting to leave an inheritance.

| Product Type | Payment Structure | Interest Impact | Best Suited For |

|---|---|---|---|

| Lump Sum Lifetime Mortgages | Single large payment | Interest compounds on the total loan | Large, immediate financing needs |

| Drawdown Lifetime Mortgages | Release funds as needed | Interest accrues only on funds released | Controlling loan costs |

| Retirement Interest-Only Mortgages | Regular interest payments | Asset-rich, cash-flow-stable retirees | Asset-rich, cash flow stable retirees |

Each retirement mortgage product serves different financial goals. Whether you want to keep your home’s value, handle interest costs better, or need a big sum, there’s an option for you.

We have tips to help you get the best deals:

- Shop around and don’t just take the first offer. Look at different lenders to find the best fit for you.

- Check your credit score, as a good score can help you get better rates. Make sure your credit report is correct.

- Consider fixed vs variable rates. Fixed rates offer certainty, while variable rates may start lower. Choose what fits your financial goals and risk level.

- Ask for professional advice and get personalised help from a financial adviser or a specialist.

Considering early repayment might be wise, as it can lower total interest. With this knowledge and these tips, we aim to find you the best retirement mortgage deals.

Customising Your Retirement Mortgage to Your Financial Situation

As we approach retirement, our financial situation becomes crucial for a peaceful later life. We understand that everyone’s finances are different. That’s why we focus on creating retirement mortgage plans tailored to you.

Junilee’s approach is to make your retirement planning special to you, filled with bespoke financial advice.

Personalised Retirement Planning

A retirement mortgage isn’t just any product; it’s key to your future. It should honour your past efforts, your dreams, and the legacy you want to leave.

We design your retirement mortgage by considering your assets, expected income, and potential lifestyle changes. This helps us create a plan that truly fits your future needs.

Assessing Financial Goals and Retirement Income

Financial goals are a priority in retirement. We find the best ways to support your income by carefully assessing your situation. Whether you want to enjoy a good lifestyle, have fun, or help your family, your mortgage plan must support these goals.

- Reviewing pension pots: We look at what you’ll get from your pension.

- Assessing investments and savings: We estimate the future value and the potential earnings for you.

- Property equity: We see how your property can help your retirement finances.

- Legacy ambitions: We consider your wishes to help your family after you’re gone.

| Strategy | How It Works | Benefit |

|---|---|---|

| Equity Release | Pulling funds from property value while retaining usage rights. | Reduces the taxable estate value, potentially decreasing inheritance tax. |

| Gifts Using Surplus Income | Allows growth outside of the estate and a repayable loan on demand. | Gradually transfers wealth during the retiree’s lifetime, utilising exemptions. |

| Loan Trusts | Setting up a trust with the mortgage as a loan to the trust. | Allows growth outside of the estate and a repayable loan on demand. |

| Mortgage Repayment Plan | Using life insurance to pay off the mortgage on death. | Ensures property passes with reduced or no debt, lessening the tax burden. |

Proactive management of property wealth offers significant benefits for inheritance tax. Smart planning and the right mortgage strategies can create a stronger legacy, reducing the burden on future generations.

Comprehensive Guide to the Types of Retirement Mortgages Available

There are many different types of retirement mortgages available to you. Knowing which mortgage type is best can boost your finances in retirement. You might prefer a drawdown scheme or a lump-sum plan.

Understanding lifetime mortgages well is key. Retirement interest-only mortgages offer more ways to manage money in retirement.

Lifetime Mortgages: Lump Sum vs. Drawdown

Lifetime mortgages let homeowners access the value of their property without having to move out. There are two options: lump-sum and drawdown.

- Lump Sum Lifetime Mortgages provide a large lump sum upfront. They’re good for paying off big debts or major home updates.

- Drawdown Lifetime Mortgages allow retirees to access equity when needed. This helps control loan size and reduce interest costs.

These options give retirees flexibility in their financial plans. They cater to different income needs and legacy-planning plans.

Retirement Interest-Only Mortgages Explained

Retirement interest-only mortgages (RIOs) are quite new. Borrowers pay only the monthly interest, and the loan amount doesn’t decrease. The full loan is paid when the home is sold, the borrower dies, or the borrower moves into care.

RIOs suit people with stable incomes who want to keep their capital. They often have fewer loan or property value limits than other loans.

We’ve looked at the market to help you understand each mortgage’s long-term costs and effects on inheritance.

Golden Years Gifting: Equity Release for Family Support

You need to think about our legacy and how we support our family. The idea of gifting in the golden years has become a meaningful way to help. It’s vital to understand how equity release can support family finances.

Equity release enables homeowners to access the value of their property. These funds can help family members during important times, such as buying a first home or paying for education.

The key benefit is making a big impact on our relatives’ lives without waiting for inheritance processes.

Now, let’s look at how these financial options can be crucial for gifting in our golden years:

- Releasing equity can help provide a living inheritance. Beneficiaries can use the funds when they really need them.

- It can also cut down inheritance tax, making the estate smaller over time.

- This offers a way to pick how much to release and when. It helps keep our finances secure.

However, it’s important to consider how this affects retirement benefits. Talking to a financial advisor is key to understanding this properly.

“Many see golden years gifting through equity release as a chance to see their hard work help their family when needed most. It’s a special part of passing on wealth.”

Lastly, equity release can be an effective way to build a family’s future. It helps the next generation succeed with support that goes beyond money. So, let’s think about the profound impact of golden years gifting on our legacies and our families’ growth.

| Market Condition | Impact on Property Market | Suggested Adaptation |

|---|---|---|

| Rising Interest Rates | Increased borrowing costs, decreased affordability | Consider fixed-rate mortgages to secure predictable repayments |

| Economic Downturn | Potential decrease in property values | Explore options for releasing equity or downsizing to lower- value risk |

| Increased Demand for Housing | Property values rise, creating equity growth | Assess the potential for property investment or equity release schemes |

Getting ready for retirement means understanding how the property market affects our finances. We must adapt to the ups and downs of property values and market conditions.

| Repayment Option | Monthly Repayment Content | Impact on Retirement Cash Flow | End of Mortgage Term Outcome |

|---|---|---|---|

| Interest Only | Interest payments only | Lower payments, better cash flow | Principal sum remains, repayment predominantly through property sale |

| Capital Repayment | Interest and principal | Higher payments, less disposable income | Debt decreases, resulting in potential inheritance |

Both repayment options have pros and cons for retirement mortgages. Deciding between interest-only and capital repayment depends on your situation, including your income, the level of financial freedom you want, and your estate planning wishes.

It’s best to carefully consider both options in light of your long-term retirement finances.

Retirement Mortgages Specialists

Understanding retirement mortgages can be tricky. That’s why expert guidance is so necessary. Retirement mortgage specialists like Jubilee 2000 provide expert advice tailored to retirees’ unique needs.

Professionals provide retirees with deep insights into various mortgage options. They explain the complicated legal and financial details. This help is key to making choices that fit retirees’ financial goals and life situations.

Here are several compelling reasons to consult specialists:

- Comprehensive analysis of current financial standing and projections for future needs.

- Detailed exploration of the mortgage market to identify the most suitable options.

- Guidance on the implications of estate planning and inheritance.

- Assistance with navigating the regulatory environment and compliance requirements.

- Support in risk assessment and the implementation of strategies to mitigate potential financial exposure.

For funding our retirement years, retirement mortgage specialists can really help.

These specialists keep their knowledge up to date. They track changes in the market, laws, and financial products, which means they always offer relevant and helpful advice.

Application Process for Securing a Mortgage in Retirement

Getting a mortgage in your later years might seem difficult. But our step-by-step guide is here to make it easier. Knowing what documents you need makes the process less stressful.

The Step-by-Step Guide to Applying

The steps to getting a retirement mortgage require careful attention. Our guide helps you understand each phase and ensures you’re ready to move forward confidently.

Here are the key steps:

- Initial Consultation: Talk to your lender about your needs and learn about their offers.

- Mortgage Pre-approval: Get a pre-approval to see how much money you can borrow.

- Documentation: Gather all necessary documents, such as proof of income and ID.

- Application Submission: Complete and send off the mortgage application with your documents.

- Property Valuation: The lender checks the property’s value.

- Mortgage Offer: If all goes well, you’ll get a mortgage offer to accept.

- Legal Process: Work with a solicitor on the legal bits of your mortgage.

- Completion: After everything is done, the funds are released, and your mortgage starts.

Documents and Information Required

You need to collect certain documents for your mortgage application.

These are crucial:

| Document Type | Description | Examples |

|---|---|---|

| Proof of Identity | Legal documents to confirm who you are. | Passport, Driving Licence |

| Proof of Income | Documents to show how much money you make. | Pension statements, Investment returns |

| Proof of Address | Proof of where you live. | Utility bills, Council tax statement |

| Credit History | A record showing how good you are at paying back money. | Solicitor’s contact information, Letter of Engagement |

| Property Details | Information about the property you want to mortgage. | Title deeds, Property valuation |

| Legal Representation | Information about your lawyer. | Solicitor’s contact information, Letter of engagement |

Preparing your documents will help you with your mortgage application. It’s a step towards a secure retirement. You’ll be closer to securing your financial future with everything in order.

Assessing the Risk Factor: Retirement Mortgages and Your Financial Future

Retirement mortgages can make later life more comfortable, but we must consider the risks. Every financial choice brings possible risks. Understanding these risks will help us handle them better. We will look into the key concerns and how to address them safely.

Analysing Potential Risks and How to Mitigate Them

Retirement mortgages allow homeowners to access the value of their homes for cash. However, they come with specific risks.

Let’s look at these risks:

- Interest Rate Variations: Changes in rates can affect monthly payments and total interest.

- Property Value Depreciation: A fall in property value can affect available equity and inheritance.

- Lifetime Commitment: This financial choice may restrict your ability to move or sell.

- Inheritance Reduction: Using equity now might mean less for your heirs.

A good plan is necessary to manage these risks. Fixed-rate mortgages can help with interest rate changes. A ‘no negative equity’ guarantee offers protection if property values drop. Talking to family ensures they understand the impact of inheritance.

The Role of Mortgage Insurance in Securing Your Legacy

Mortgage insurance is vital for securing your legacy with a retirement mortgage. It covers any remaining mortgage debt, allowing the property to pass to heirs without major financial troubles.

Considering mortgage insurance helps ensure your family’s financial goals are protected.

| Risk Factor | Impact Without Mitigation | Impact With Mortgage Insurance |

|---|---|---|

| Interest Rates Increase | Higher repayments, increased debt | Debt settled, preserving inheritance |

| Property Market Downturn | Potential negative equity | Debt cleared, no negative equity concern |

| Health Issues or Early Death | Impact of Mortgage Insurance | Loan repaid, family home secured |

Exploring retirement mortgages means preparing for the risks involved. Mortgage insurance is not just an option; it’s how we can keep our promise to protect our family’s future, no matter what happens.

FAQ

What is a retirement mortgage, and why is it important?

A retirement mortgage helps retirees access home equity to support their financial needs. It ensures a secure and comfortable future without having to sell the home.

How does a retirement mortgage differ from a traditional mortgage?

Retirement mortgages are tailored for retirees. They have flexible repayments based on reduced retirement incomes. This allows access to home equity without moving.

What is equity release, and how can it benefit retirees?

Equity release lets retirees access the value of their home without selling. It offers a lump sum or income, helping them maintain their retirement lifestyle without having to relocate.

What are the eligibility criteria for retirement mortgages?

Eligibility for retirement mortgages includes being 55 or older, meeting minimum property value requirements, and having a stable income to support affordability.

What borrowing options does First Direct offer for individuals over 70?

First Direct has retirement mortgages for those over 70. They help retirees access their home equity.

How can retirees maximise their retirement security through property equity?

Retirees can boost their financial security by tapping into their home’s equity. This provides extra retirement income, ensuring stability.

What are the benefits of using home equity as retirement income?

Using home equity aids retirees by enhancing their income, supporting their lifestyle, and ensuring financial stability without moving.

What are the different types of retirement mortgage products available?

Retirees can choose from lump-sum, drawdown, or interest-only mortgages. Each offers unique benefits to fit various needs.

What are the emerging trends in retirement lending?

New trends in retirement lending include more flexible products, tailored solutions, and a focus on later-life borrowing. They cater to retirees’ changing needs.

How can retirees find the best deals on retirement mortgages?

Retirees should compare rates and consider terms and fees to find the best mortgage deals. Shopping around is key.

How can retirees customise their retirement mortgage to their financial situation?

Retirees can tailor their mortgage by considering their financial goals and income. A mortgage specialist can guide them to the best fit.

How can retirees manage property wealth for future generations?

Retirees can use equity release to support loved ones financially. This helps pass on wealth while managing inheritance tax.

What are the different types of retirement mortgages available?

The main retirement mortgage options are lifetime and interest-only. They are designed to meet the specific financial needs of retirees.

What are the benefits and downsides of interest-only and capital repayment options for retirement mortgages?

Interest-only mortgages offer lower payments but require a repayment plan at the end of the loan. Capital-repayment mortgages ensure the loan is paid off, but require higher payments. Each has pros and cons.