"*" indicates required fields

Understanding the Basics of Remortgaging in the UK

The search for remortgages involves switching your current mortgage to a new deal, either with your existing lender or a new one. This can be a strategic move to reduce your monthly payments, borrow additional funds, or secure a better interest rate. Currently, lenders are keen to lend, and remortgages are a key focus for some specialist UK lenders.

Factors Influencing Remortgage Eligibility

Loan-to-Value (LTV): This is the ratio of your loan amount to your property’s value. Different LTV brackets, such as 95%, 90%, and 85%, can impact the mortgage offer terms.

Property Valuation: Your property’s market value is crucial in remortgaging. Many lenders offer a free valuation to facilitate the remortgage process.

Credit History: A history of bad credit, including CCJs, defaults, or arrears, can complicate remortgage approval but is not necessarily a disqualifier.

Remortgages Terms – Credit Checks and Mortgage Brokers

A soft credit search is often conducted initially to assess your eligibility without impacting your credit score. Mortgage brokers, who often do not charge broker fees, can facilitate this process, especially for complex cases.

Mortgage Rate Options

Choosing the right mortgage rate can significantly affect your financial health over time. Options include:

- Fixed Rates: These are available in 2-, 3-, and 5-year terms, and the interest rate remains constant.

- Discounted Rates: A reduction on the lender’s standard variable rate for a set period.

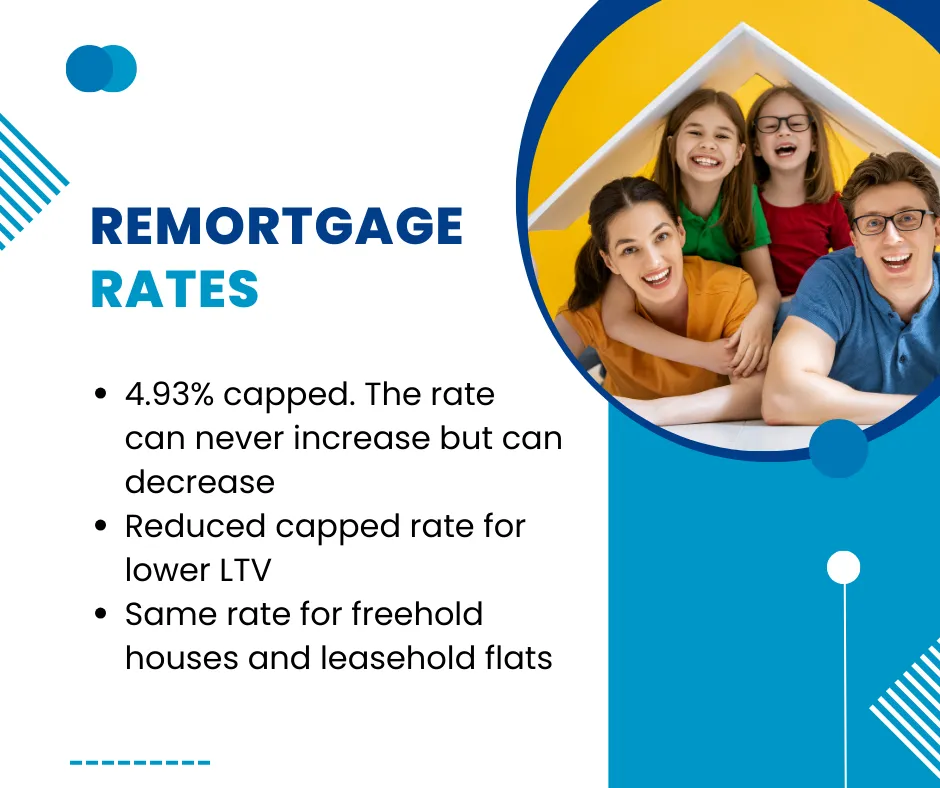

- Capped Rates: Similar to fixed rates, they allow some fluctuation within a set limit.

Special Considerations for Self-Employed Individuals

Self-employed individuals may face stricter scrutiny when remortgaging. Lenders will typically require detailed financial records and proof of steady income. However, several lenders are sympathetic to self-employed applicants, especially those with good financial records and a reasonable LTV.

Additional Financial Considerations

Debt Consolidation: Remortgaging can help consolidate debts, potentially lowering overall borrowing costs and simplifying monthly payments.

Divorce and Legal Considerations: Remortgaging may be necessary in a legal separation or divorce, allowing one party to buy out the other’s share of the property.

Understanding the Risks

Redemption Penalties and Early Repayment Charges are common in many fixed- and discounted-rate mortgages. These fees can make it expensive to switch mortgages before the end of a deal period.

High Loan-to-Value Challenges: Remortgaging might be more challenging for those with high LTV ratios. Specialised lenders might still provide options, albeit at higher interest rates.

Non-Standard Construction: Properties with non-standard construction can also pose challenges due to perceived higher risks.

Alternatives to Remortgaging

If remortgaging isn’t viable, secured loans or further advances from current lenders might be an alternative, particularly for temporary financial needs or specific projects.

Guide to Remortgaging for Individuals Over 55 in the UK

Remortgaging can enhance financial flexibility in later life for those aged 55 and above. Understanding your options is crucial, whether you’re releasing equity, reducing monthly payments, or securing a better interest rate.

Why Consider Remortgaging Over 55?

Equity Release: Many homeowners over 55 have significant equity in their homes, which can be accessed through remortgaging to support retirement plans, home improvements, or help family members financially.

Debt Consolidation: If you have multiple debts, remortgaging can consolidate them into a single manageable monthly payment, often at a lower interest rate.

Eligibility and Considerations

Lenders will consider your age and likely retirement age when assessing your application. It’s essential to demonstrate that you can manage repayments, especially if the mortgage term extends into retirement.

Mortgage terms may be shorter, and you might need to show detailed financial plans for your retirement income sources, such as pensions and investments.

Types of Remortgage Deals for Seniors

Choosing the right type of mortgage deal is crucial:

- Fixed-Rate Mortgages: Lock in your interest rate for a set period, which can help protect you from rate increases.

- Standard Variable Rate (SVR) Mortgages: The rate can change with the lender’s SVR, which may be suitable if you expect rates to fall or plan to pay off the mortgage soon.

- Lifetime Mortgages are a form of equity release in which you are not required to make monthly repayments. The loan and accrued interest are repaid when the home is sold, typically when you pass away or move into long-term care.

Key Features to Look For

No Early Repayment Charge (ERC): This feature is particularly valuable if you anticipate changes in your financial situation that might allow you to pay off your mortgage sooner than expected.

Flexible Repayment Terms: Some lenders offer the option to overpay, which can help reduce the amount owed more quickly.

Getting Professional Advice

It is highly recommended that you consult a qualified mortgage advisor specialising in mortgages for older individuals. They can provide tailored advice based on your personal circumstances and help you navigate the complex landscape of lending in later life.

A professional valuation of your property will generally be required to proceed with a remortgage application. This will ensure you receive the most advantageous terms based on your home’s current value.

Considerations Before Remortgaging

Considering how economic changes might affect your ability to repay a mortgage is vital. Interest rates, market conditions, and health can all influence your decision.

Also, consider long-term financial planning, especially if you are considering a remortgage that could extend beyond your working years into retirement.