Find out if Jubilee 2000 Mortgages for over 65s are ideal for your financial needs:

- No lender, advisor or broker fees

- Direct lender

- Free desktop-based home valuation with no visitors to your home

- 4.89% fixed for life

- No early repayment charges

- A portable mortgage is ready if you want to move house

- Ideal to pay off an existing mortgage at the end of its term

- A decision in principle based on a soft credit search

- Interest-only or repayment terms

- Up to 70% loan-to-value

- One penalty-free payment holiday per year

- There is no valuation penalty for flats and other leasehold properties

- No upper age limit or fixed term

- Fast completions in as little as two weeks

- Ideal for IHT and other tax planning

- Remortgage your existing home or move and buy a new home

For example, if your home is worth £345,000, you can borrow £241,500.

"*" indicates required fields

People who are not eligible for the Jubilee 2000 over 65 mortgage:

- People who do not own their home

- Bankrupt people

- People who have unspent criminal convictions for fraud or other dishonesty

- People who are under 65

- People who are currently in court, getting their homes repossessed

Properties that are not acceptable:

- Holiday homes with limited occupancy

- Park homes

- Caravans

- Properties that are in immediate need of significant structural repair

- Properties that have had significant floods in the last three years

- Homes owned by corporate structures or trusts

Today’s retirees are living longer, healthier lives. This means that more than 65% of people in the UK are getting mortgages. Despite this, it’s surprising that there’s a rise in Nationwide mortgages for over-65s across the UK. This shows lenders’ trust in older borrowers.

We’re seeing more over-65 mortgages as we look closer. Even though the financial world often favours the young, it’s key to understand the unique needs of those over 65 seeking a mortgage.

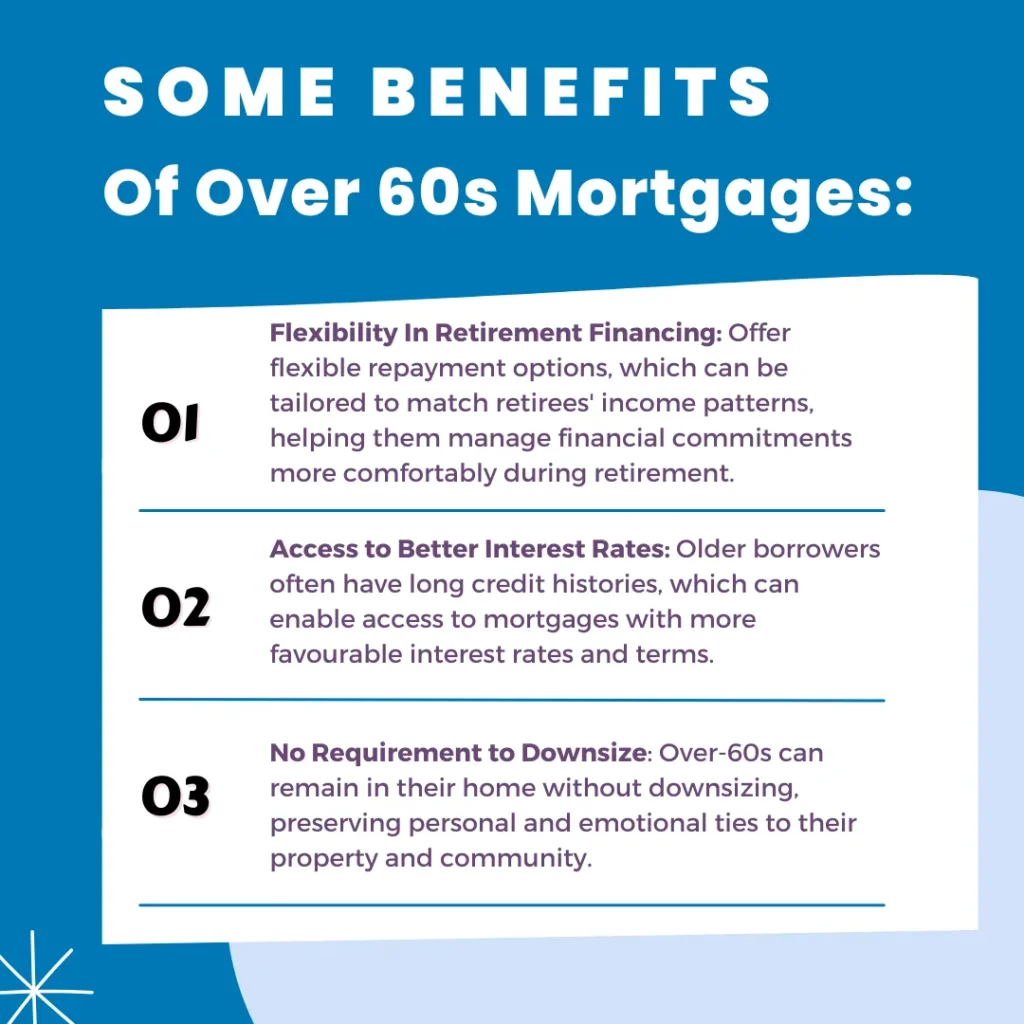

The start of retirement no longer means the end of mortgage payments for many. The market for mortgages over 65 is growing. They might want to move, downsize, or release equity. The UK recognises the value and flexibility of older people’s finances, offering more mortgages for over-65s.

Some IMPORTANT FACTORS TO CONSIDER:

- There has been a significant increase in the best mortgages for UK applicants over 65, reflecting changing market trends.

- Despite traditional views, retirees seek and obtain Martin Lewis over 65 mortgages for various financial strategies.

- The financial industry is responding with tailored mortgage for over 65 products to meet the demands of an ageing population.

- Understanding the unique opportunities and obstacles is crucial for securing a suitable mortgage 65 or older.

- Age should not be a barrier when considering a mortgages over 65, as options are more plentiful than often perceived.

The Range of Products Tailored for Pensioners – applying for a mortgage in 2026

Getting a mortgage at 65 is common, and yes, you can. Banks have made mortgages available to older individuals seeking loans. They offer interest-only and repayment mortgages, tailored to fit pensioners’ financial plans.

- Interest-only mortgages mean you only pay the monthly interest, without reducing the loan balance.

- Repayment mortgages help people over 65 pay off their loans and interest, eventually allowing them to own their homes outright.

Securing Competitive Rates: Possibilities and Challenges at the age of 65

Getting a good mortgage rate is possible even later in life. It requires some effort, especially for those after a pensioner mortgage. They must consider their income, property value, and current interest rates.

Banks aim to offer practical mortgage options to older customers through a range of products. However, pensioners face different conditions that affect their mortgage rates, like their credit history and income.

| Mortgage Type | Possible Rates | Key Considerations |

|---|---|---|

| Interest-only | Competitive, age-dependent | Lifetime income plan, estate size |

| Repayment | Fixed, Variable rates | Stable income, credit history |

Finding the right mortgage requires thorough research and careful consideration. Listening to those who’ve done it before can offer valuable insights.

“The process was smoother than I expected. Despite my age concerns, I found a lender that saw the value in my stable income,”

Said a pensioner who recently got through this process.

Barclays Mortgages for over 65s is more than just a financial matter; it’s about securing a stable future. Finding a mortgage that fits your retirement dreams is possible, offering peace of mind in later life.

Understanding Interest-Only Mortgages for Retirees VS lifetime mortgages

Retirement is meant to be a period of financial peace. Yet the cost of housing remains a major concern. For those of us looking at our options, interest-only mortgages for over-65-year-olds are a way to manage property investment without heavy monthly repayments.

By picking an interest-only mortgage for over 65, you pay just the interest on the loan monthly. This reduces your expenses compared to regular repayment mortgages. It allows you to use more of your retirement income for other essential or enjoyable activities. However, there’s more to it than just saving money now.

Choosing an interest-only mortgage for over-65s does come with certain risks. The total loan amount doesn’t decrease over time. This raises a big question: how will you repay the loan at the end of the term? Having a clear repayment plan is vital. This could include selling the property, using pension funds, investments, or savings.

- Monthly payments are lower than with standard repayment mortgages.

- It enables living in a more expensive home than might otherwise be possible.

- Demands a detailed plan for paying off the loan upon the term’s end.

When you weigh the pros and cons, it’s clear that interest-only mortgages for over-65s can be a smart retirement strategy for those with sufficient equity, pensions, or assets. Still, rushing into such a decision isn’t wise. Getting advice from financial experts is crucial.

Interest-only mortgages give retirees needed flexibility, but need a careful exit plan.

Remember, interest rates can change and may not stay the same. A fixed-rate mortgage means stable repayments for a while. But eventually, these mortgages usually convert to variable-rate mortgages, which could raise monthly costs later.

If you’re over 65 and considering an interest-only mortgage, consider your long-term finances. It’s crucial to talk to experienced mortgage advisors. They help you understand the benefits and challenges of such a mortgage as you age.

Eligibility and Age Considerations for Over 65 Mortgages

To understand the intricacies of Nationwide mortgages for over-65-year-olds, it’s vital to first understand how age and eligibility can affect the approval process. Age is not just a number in finance; it is a crucial element. It can affect the availability and terms of mortgagesfor older borrowers.

How Age Affects Your Mortgage Application

Lenders often have age-related criteria when considering mortgages for older people. Retirement usually means shifting from steady work income to pensions and savings.

This change can affect how lenders view your ability to pay back the loan. While some age limits are in place, many lenders, such as Nationwide Mortgages for the Over 60s, see the value in lending to older individuals.

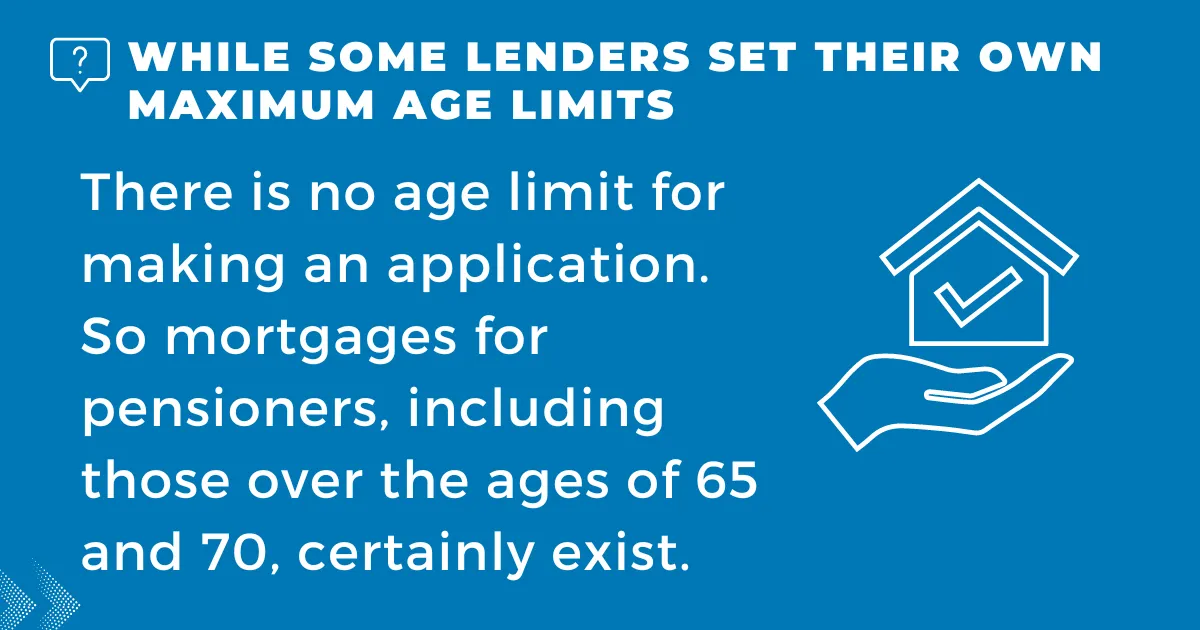

Navigating Maximum Age Limits with Lenders

When wondering “Can pensioners get a mortgage?” we see that the maximum age for a mortgage varies by lender, typically around 80 to 85. However, getting a mortgage for pensioners is still possible. It involves understanding lenders’ expectations and effectively showcasing your financial situation. You should prepare detailed income documentation, including pensions, investments, and part-time jobs.

A comparison of age policies among popular lenders shows it’s important to shop around for suitable mortgages for older borrowers:

| Lender | Max Age at Application | Max Age at End of Mortgage Term | Remarks |

|---|---|---|---|

| Lender A | 75 | 85 | Offers fixed-term repayment mortgages |

| Lender B | 80 | 95 | Provides equity release options |

| Lender C | No maximum age at application | 99 | Interest-only mortgages available |

Opportunities for mortgages extend beyond the traditional retirement age. A strong financial plan and good credit are vital for a mortgage later in life. We’ve seen clients in their 70s and 80s get mortgages by meeting the right conditions and presenting a solid application.

HSBC Mortgages for over-65-year-olds have become more inclusive. Age isn’t a barrier to getting a mortgage, but it’s a factor to consider in your application strategy. Options are available, such as nationwide mortgages for the over-60s, catering to the financial situations of older borrowers.

Santander Mortgages for Over 65s

Are you wondering: Can I get a mortgage at 65 or beyond? Yes, you can. Nowadays, finding a mortgage for those over 65 isn’t rare. There are unique products made for older borrowers. Let’s explore how to secure a mortgage at this life stage.

The mortgage market has changed to meet the needs of older adults. This is because people are living longer and retiring differently. Lenders have become more open to working with older borrowers. They check if you can afford the loan and if the property is valuable.

Lenders have made products for older borrowers. These are for those with pension income, investments, or still working. Many wonder, can you get a mortgage at 65? Yes, and there are choices for you.

Expect these features in mortgages for those 65 and up:

| Feature | Benefit | Challenge |

|---|---|---|

| Longer Loan Periods | Lower monthly payments | It might affect inheritance planning |

| Interest-Only Options | Improved cash flow management | Need to plan for eventual repayment of the principal |

| Equity Release | Access locked-in home equity | Might affect inheritance planning |

Lloyds Mortgages for over 65s offer financial freedom, or can help consolidate debts. They can also help you move or downsize. But remember, there are age-related limits when applying for or ending the mortgage term.

Understanding age restrictions is crucial. Some lenders limit the age at which a mortgage can be terminated. Yet seniors now have more chances to get a mortgage. This shows that getting older doesn’t stop you from making big financial choices.

Our goal is to clarify the mortgage process in your senior years. Mortgages for those over 65 are more than money. They’re about how you choose to live, and making an informed choice is key.

The Role of Income and Affordability in Obtaining Mortgages Over 65

Securing a mortgage as a pensioner involves understanding different sources of income. This is vital for our comfort in retirement, and a retirement income mortgage comes into play.

Income factors are crucial in getting mortgage approval in our later years. Let’s look at these factors closely.

Pension, Investments, and Alternative Incomes

A pension is often the main income for retirees. However, lenders also consider incomes from investments and other sources. They consider dividends, rental properties, or part-time work.

Each type of income is carefully reviewed. This ensures the mortgage is both manageable and lasting for a pensioner.

It’s about painting a full picture of your financial capacity, and every little bit contributes to the greater canvas that lenders will evaluate.

These income sources help show that you can handle mortgage payments. They also show lenders that your financial risk is spread out.

| Aspect of Retirement | Without Pensioner Mortgage | With Pensioner Mortgage |

|---|---|---|

| Home Renovations | Limited by Savings | Without a Pensioner Mortgage |

| Lifestyle & Leisure | Capital available to enhance the living environment | Flexible spending for travel, hobbies, etc. |

| Unexpected Expenses | Financial stress and potential debt accumulation | Readily accessible funds to handle emergencies |

Dealing with Bad Credit and Adverse Financial Situations when trying to sort out home improvements

Many think it’s impossible to get TSB mortgages for over-65s with bad credit. But life sometimes throws a wrench into our financial plans. We believe retirement should be worry-free. That’s why we help retirees with bad credit get pensioner mortgages.

Bad credit is a major hurdle to getting a mortgage, but being older shouldn’t make it harder. Fixing any credit issues is key. Start by getting your credit report and checking it. Correct mistakes and pay bills on time to better your credit score.

It’s essential to be honest with lenders about your past finances. Some lenders focus on working with those who’ve had money troubles. They might just need proof of reliable income, such as a pension, to trust that you can pay back.

There are special options for older folks with less-than-great credit. Equity release plans or retirement mortgages could work. But it’s vital to consider how these choices affect your money and property in the long run.

Finding pensioner mortgages for bad credit takes time and careful planning. A good mortgage broker can be a big help. They know about deals you might not find and can guide you through the complicated parts.

Every person’s financial situation is different. What’s hard for one might not be for another. With the right help and lots of effort, getting a mortgage in retirement with bad credit is possible.

The Impact of Market Trends on Mortgages for Older Borrowers before l

The Role of Mortgage Brokers in Facilitating a type of mortgage like Pensioner Mortgages

For older people seeking a mortgage, a mortgage broker’s knowledge is crucial. They have the skills and info needed to find the best deals in changing markets. They make sure retirees get mortgage deals that fit their retirement and financial needs.

Factors to Consider When Choosing a Mortgage Plan or a retirement interest-only mortgage

- Interest Rates: Assess whether a fixed, variable, or tracker-rate mortgage best suits your long-term financial plans.

- Loan Duration: Determining the mortgage term that coincides with your anticipated retirement timeline and ability to make repayments.

- Repayment Vehicle: Understanding the mechanisms, such as an endowment policy or an investment fund, that are designated to repay the loan’s capital upon maturity.

- Equity Release: Consider if a lifetime mortgage or a home reversion plan could provide additional financial respite.

We are dedicated to your financial well-being in retirement. This means planning for unexpected events is vital. It’s also essential to work with professionals who have your best interests at heart, especially when considering a mortgage for pensioners.

FAQ

Is it possible to get a mortgage at 65?

Yes, you can get a mortgage at 65. There are special mortgage options for those over 65.

What are the mortgage options available for individuals over 65?

Over 65s can choose between interest-only and repayment mortgages.

How do interest-only mortgages work for retirees?

With an interest-only mortgage, retirees pay only the loan’s interest monthly. The principal amount is due at the end of the term. This suits those over 65 with more assets than income.

What are the eligibility criteria for individuals over 65 applying for mortgages?

Eligibility is based on income, property value, and credit history. Age can affect applications, with some lenders setting age limits.

What role do income and affordability play in obtaining mortgages over 65?

For those over 65, income and affordability are key. Lenders consider pension income, investments, and other sources of income. They assess if the borrower can repay the mortgage.

What are the advantages of pensioner mortgages?

Pensioner mortgages are low-risk for lenders due to stable retiree income. They help retirees unlock the equity in their homes for a better life.

How can individuals with bad credit access mortgages over 65?

Bad-credit individuals can improve their credit and find suitable mortgages. A specialist mortgage broker can offer great help here.

Which mortgage providers are available for individuals over 65?

Providers include banks, building societies, and other lenders with good terms for over-65s.

How do market trends impact mortgages for older borrowers?

Market trends influence the terms, rates, and availability of mortgages for older borrowers. It’s crucial to stay updated and adaptable.

Why is expert advice important when selecting mortgages for older people?

Expert advice helps older people navigate mortgages. Mortgage brokers offer tailored recommendations and navigate the complex process.

What are the alternative financing options for individuals over 65?

Alternatives for over 65s include shared ownership and equity release. These options utilise their assets for financing.