Equity release mortgage lenders offer different interest rates for people across different age ranges and loan-to-value ratios. Jubilee 2000 has reviewed the best equity release companies and found one with excellent terms that should suit many homeowners’ needs.

Here are the key features:

- Free automated home valuation with no personal visit

- Loan to value up to 65%

- No lender, broker or advisor fees

- There are no valuation penalties for flats or other leasehold properties

- Voluntary repayments

- No early repayment penalties

- Ideal to pay off an old mortgage

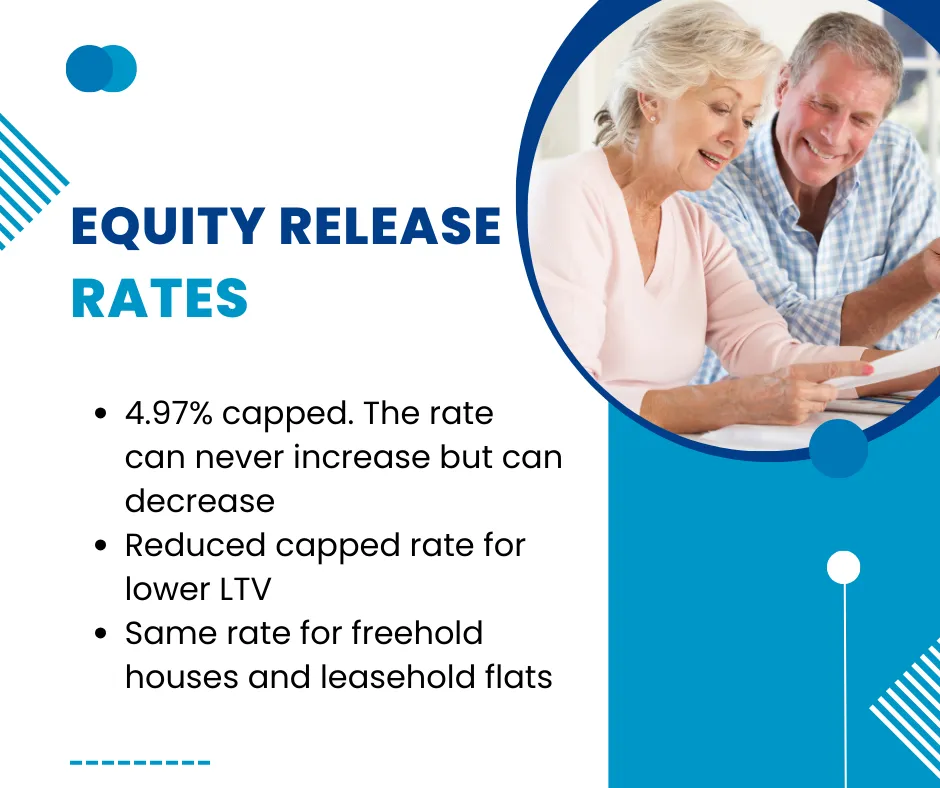

- 4.45% capped interest rate

- No upper age limits

- New product for March 2026

- No available on the leading comparison websites

Please complete the form below to find out more:

Please fill in your details below:

What are Equity Release Schemes, and what are the 2026 Equity Release interest rates?

Equity release schemes are designed to last the homeowner’s lifetime, and the cash can be used for any application the owner wishes.

The cash released from the home is repaid when the homeowner passes away or moves to a long-term care facility, at which point the house is typically sold.

The equity release will be repaid upon the sale of the house. Under these circumstances, the repayment period is 12 months, and any remaining funds will be distributed to beneficiaries.

Equity release schemes available in the United Kingdom have recently begun offering the option of making monthly payments toward the outstanding equity. The borrower can also pay just the principal balance or the principal and interest.

The decision to make monthly repayments will largely depend on the borrower’s finances, their ability to afford the additional payments, and the inheritance they wish to leave to beneficiaries.

What Types of Equity Release Plans are Available?

There are several equity release and lifetime mortgage schemes available to individuals aged 55 or over. Some of these options include Lifetime Mortgages, Interest Only Lifetime Mortgages, Drawdown Equity Release, Home Reversion, and Home Income Plan.

Choosing an equity release plan will always depend on the borrower’s unique circumstances, and care should be taken to make an informed decision about which scheme best fits their finances and overall needs.

Lifetime Mortgages are one of the most popular types of equity release schemes. These loans are secured against the home’s value and can be exchanged for a tax-free lump sum or as supplemental income.

Lifetime Mortgages charge a fixed interest rate and are not repaid by monthly payments; the interest is added to the overall mortgage balance. The balance, including all interest, is repaid when the property is sold, and the remaining funds are distributed to the beneficiaries.

Another popular equity release scheme is the Drawdown Lifetime Mortgage. This option is similar to the popular Lifetime Mortgage but with added flexibility. This scheme provides the borrower with a cash reserve facility, allowing them to withdraw any amount initially, with the remainder reserved for future withdrawal.

4 Little-Known Truths About Equity Release

Equity release is becoming an increasingly popular option for homeowners looking to unlock the value of their property. However, several aspects are not widely known. Here are four little-known truths about equity release:

- Equity release can provide a tax-free lump sum or regular income.

- It’s possible to remain in your home for life with specific schemes.

- Some plans allow you to guarantee an inheritance for your family.

- Equity release schemes are regulated by the Equity Release Council to ensure consumer protection.

Equity Release Council

The Equity Release Council is the industry body that ensures all equity release plans adhere to strict guidelines to protect consumers. This includes a “no negative equity guarantee,” which means you will never owe more than the value of your home.

Equity Release Horror Stories

While equity release can be a beneficial financial tool, there have been instances where people have encountered problems. These equity release horror stories often stem from a lack of full understanding of the terms of their agreement or from not seeking independent advice.

Saga Equity Release

Saga Equity Release offers a range of options tailored for people aged 55 and over, enabling them to release funds from their homes to enjoy a more comfortable retirement.

Legal and General Equity Release

Legal and General Equity Release is one of the leading providers in the market, offering competitive rates and flexible plans to suit different needs.

Santander Equity Release

Santander Equity Release offers options for unlocking the value of your home, with plans tailored to your individual circumstances.

Equity Release Northern Ireland

Equity release options are also available in Northern Ireland, providing benefits and protections similar to those in the rest of the UK.

Equity Release Supermarket

The Equity Release Supermarket offers a comparison service to help you find the best equity release deals from a wide range of providers. This ensures you get the best deal for your needs.

Explain Equity Release

Equity release is a way of accessing the equity tied up in your home. It can be done with a lump sum, a regular income, or a combination of both, without needing to move out.

More to Life Equity Release with no fees

More to Life Equity Release offers flexible plans that can adapt to changing needs and circumstances, providing peace of mind and financial stability.

Halifax Equity Release interest rates

Halifax Equity Release offers competitive rates and flexible terms, making it a popular choice for homeowners looking to release equity from their property.

How Do Equity Release Schemes Work?

Understanding how equity release schemes work is crucial before making a decision. Generally, these schemes allow homeowners to access the value of their home without having to sell or move out, with the loan repaid upon death or moving into long-term care.

L&G Equity Release rates

L&G Equity Release offers various plans to help you access the funds you need, including lump-sum and drawdown facilities.

Alternatives to Equity Release

Before committing to equity release, consider alternatives, such as downsizing, taking out a retirement interest-only mortgage, or exploring other financial products.

Martin Lewis Equity Release Advice

Martin Lewis’s equity release advice can be invaluable. He often emphasises the importance of understanding all the costs and implications before proceeding and recommends seeking independent financial advice.

Can I Sell My House if I Have Equity Release?

A common question is, “Can I sell my house if I have equity release?” The answer is yes, but you will need to repay the equity release loan from the sale proceeds.

Standard Life Equity Release

Standard Life Equity Release offers competitive products that help you access the equity in your home while retaining full ownership of your property.

Equity Release London

For those living in the capital, specific equity release plans tailored to London’s higher property values offer substantial equity release potential.

Aviva Equity Release Reviews

Checking Aviva equity release reviews can provide insight into customer satisfaction and the reliability of their products, helping you make an informed decision.

Do You Pay Tax on Equity Release?

A frequent question is, “Do you pay tax on equity release?” The answer is no. The money you release from your home is tax-free, though it may affect your eligibility for means-tested benefits.

Scottish Widows Equity Release

Scottish Widows Equity Release offers flexible plans that cater to a range of needs, ensuring you can access the funds you require without compromising your financial security.

Reader’s Digest Equity Release

Articles like Reader’s Digest equity release provide valuable information and real-life experiences from those who have used equity release, helping you understand the potential benefits and pitfalls.

Money Saving Expert Equity Release

Advice from MoneySavingExpert on equity release is highly regarded. They offer detailed guides and comparisons to help you navigate the options and choose the best product for your situation.

Is Equity Release Tax-Free?

A key benefit of equity release is that it is generally tax-free. The funds you release are not subject to income tax, making it an attractive option for those looking to supplement their retirement income.

Halifax Equity Release Under 55

While most equity release products are aimed at those over 55, some options are available to younger homeowners, including Halifax equity release under-55 schemes, which may offer different terms and conditions.