Have you received harassment calls, threatening letters, text messages, or visits to your home from Cabot Financial UK?

Don’t let debt affect your life and mental health. Complete the questionnaire below to get support in dealing with Cabot.

Discover How To Write Off Cabot Financial Debt

End The Worrying, Remove Stress, Take Action Today

Who is Cabot Financial?

Cabot Financial is part of the Cabot Credit Management Group and has been around since 1998, making it one of the oldest debt collection agencies in the UK. Although it has many offices throughout the UK, its head registered office is in Kent.

Although you likely have never borrowed money from Cabot Financial, you may owe them money as they buy your debt from the companies you owe them to. Cabot Financial buys your debts at a lower price in the hopes that you will pay the debt in full, which is how they make money.

What companies does Cabot Financial buy debt from?

If you’re still not sure if you owe Cabot Financial money if you have debt with one of the following companies, you likely do:

- N-Power

- the DVLA

- First Utility

- Scottish Power

- Loan companies

- Local councils

- Credit card companies

Online Forums Are Full Of Posts From Scared People Trying To Deal With Persistent Debt Collectors:

Is Cabot Financial Legitimate?

As many people have never heard of Cabot Financial before they reach out, many are unsure about whether or not they are a legitimate company or if they are trying to scam people. Cabot Financial is, however, is authorised by the Financial Conduct Authority (FCA), and they are members of the Credit Services Association (CSA). So, Cabot is, in fact, a legitimate company.

Even though Cabot Financial is a legitimate company, they can still be guilty of misconduct. If you want to complain about them, they have a detailed complaints procedure on their website. If the complaint still needs to be addressed, you can escalate it to the ombudsman. There are two types of ombudsman to contact, depending on your type of debt.

What happens next?

If you have already received a call, email, or letter from Cabot Financial, they have already started collecting your debt. They will start by contacting you continually; even if you block their number, they will call from another. If you try to ignore them, they may even visit your home. While it is legal for them to come, you do not have to let them in.

Cabot Financial is calling or sending a letter in the hopes that they can receive your repayment, whether it’s as a lump sum or through a payment plan. They want you to repay your debt so they can earn some money.

Following this, if you have not repaid your debt or made a deal with Cabot Financial, they can register this failure to make repayments with a credit reference agency. This can damage your credit rating, negatively impacting your ability to take out a loan, mortgage, or another credit card in the future.

Finally, and often in the worst-case scenario, Cabot Financial could take you to court to receive a judgment against you. If the court rules in their favour, a bailiff could come to your home to take anything that equates to the value of your debt. Alternatively, you could lose your home at this stage if you don’t pay off your debt in the agreed-upon time.

Ultimately, ignoring your debt and Cabot Financial will not work, even if you obtained a cease and desist letter to prevent Cabot to stop contacting you. You will still owe the debt, and they can still take you to court. So, the best way to deal with your debt is to face it head-on. Here are some of the ways you can do that.

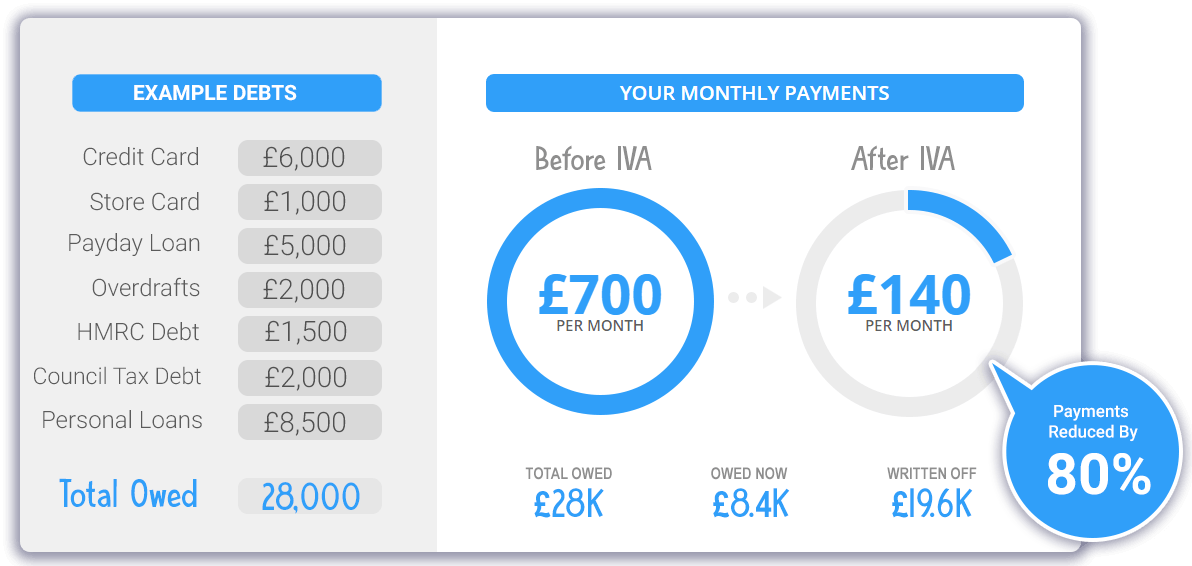

How An IVA Could Radically Reduce Your Debts

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 30-second Form

Create a budget

The best place to start with repaying your debt is to see if you can afford to pay it off and how much you can pay.

You can do this by creating a budget. Include all of your monthly necessities, such as rent/mortgage, utilities, food, insurance, etc. Whatever is left over is essentially spending money or the maximum amount you could afford to put towards your debts.

Once you know how much you can afford to pay a month, you can tell the debt collectors, and they should be willing to set up a monthly repayment plan with you based on the number.

How do I pay Cabot Financial?

You can start making monthly repayments after reaching a repayment agreement with Cabot Financial. You can do this by registering your payment plan on their website’s portal or by paying over the phone.

Whether you’re making a partial payment, monthly payments, or a lump sum, you can pay your debt to Cabot Financial with a credit or debit card, a payment slip, a bank transfer, or a cheque.

What if I can’t afford to pay off my debts?

If you’ve calculated your budget and realized you have no money left over to pay off your debt, Cabot Financial may still be willing to work with you. They could offer you a discounted debt rate if you agree to pay them in full. If you can pay off the total, discounted rate of your debts, get their offer in writing, pay them off, and you will be debt-free!

How else can I write off my debt?

If you still are not able to pay off your debt, even with a discounted rate, you may be able to write it off with insolvency. There are a few different ways to do so; one is applying for an Individual Voluntary Arrangement. An Individual Voluntary Agreement is an agreement made with the government where they will help you write off up to 75% of your debts with Cabot Financial.

Before applying, check if you qualify for the agreement. Your debts must be over £1,700, and you will have to pay back the remaining amount of what is not written off at once or monthly.

Another type of insolvency is a debt relief order. With a debt relief order, your debts will be written off after a year. To qualify, your debt must be less than £20,000, you cannot own a house, and you must have less than £50 after paying for your monthly essentials. Not only is it harder to qualify for a debt relief order, but it will also stay on your credit file for up to six years, making it hard to apply for any loans, credit cards, or a mortgage in the future.

A last resort option tends to be filing for bankruptcy, as it can have a huge impact on your credit history for years. If you have no other options, you can file for bankruptcy if your debts are at least £5,000, and you can pay an application fee of £680 to an Insolvency Service.

If you are approved for bankruptcy, all the assets you own that you don’t need for work will be taken. You will also lose control of your bank accounts to the bank. As you are losing so much, filing for bankruptcy should not be taken lightly.

Summary

In conclusion, Cabot Financial is a legitimate company that buys your debt from the companies you owe it to. If they have contacted you, it is best to answer them as soon as possible to discuss your debt repayment options so they do not take you to court. Don’t let the debt hang over your head; start your journey to being debt-free today!

Cabot Financial Details:

- 1 Kings Hill Ave, Kings Hill, West Malling ME19 4UA

- Main Telephone: 0344 556 0263

- Other Known Numbers: 08009172225, 03445560276, 03331239999, 03445560212, 03445560225, 02078966200

- FCA number: 677910

- Company No. 3439445

- Website: https://www.cabotfinancial.co.uk/

- E-Mail: Use the contact form on the website

Secured Loans to Pay Off Cabot Financial Debt Collectors

Dealing with debt collectors like Cabot Financial can be overwhelming, especially when you have a County Court Judgment (CCJ) against you. Secured loans provide a viable solution for homeowners looking to manage and repay their debts effectively. This article explores the options available for secured loans, interest rates, loan to value (LTV) ratios, and reviews from various lenders.

Understanding Secured Loans

Secured loans are loans that require collateral, typically your home, which reduces the risk for lenders. This often results in lower interest rates compared to unsecured loans. They can be an excellent way to consolidate debt, including debts collected by agencies like Cabot Financial.

Personal Loan 25k

If you need a substantial amount of money, a 25k loan over 5 years can help you manage and pay off multiple debts. These loans typically come with competitive interest rates and flexible repayment terms.

Personal Loan 50000

For larger financial needs, consider a loan for 50k. This can be especially useful for consolidating significant amounts of debt, providing a single monthly payment at a lower interest rate.

Secured Loan Brokers

Using a secured loan online broker can help you find the best loan products tailored to your needs. Brokers have access to a wide range of lenders and can provide personalized recommendations.

Secured Loans for Bad Credit Instant Decision

For those with poor credit, obtaining a loan can be challenging. However, options like fast secured loan provide quick approval and can help manage urgent financial needs.

Secured Loans for Bad Credit Direct Lenders

Working directly with lenders can sometimes yield better terms. Explore secured loans direct lenders options for those with poor credit histories.

Secured Bad Credit Loans

Even with a poor credit score, homeowners can explore secure loan for bad credit. These loans use home equity as collateral, providing better terms than unsecured loans.

Debt Consolidation Options

Debt consolidation involves combining multiple debts into a single loan with a lower interest rate, simplifying repayment and reducing overall interest costs.

Debt Payment Calculator

Using a personal loan for debt consolidation calculator helps homeowners understand their repayment options and potential savings. This tool provides a clear picture of how consolidating debt can simplify financial management.

Debt Consolidation Loan Interest Rates

Interest rates for debt consolidation loans vary based on the lender and the borrower’s credit profile. Consolidation loans can reduce the overall interest rate paid on multiple debts, making them more manageable. Learn more about large debt consolidation loans.

Credit Card Payoff Loan

If you’re struggling with credit card debt, consider a credit cards for debt consolidation to manage your repayments more effectively.

Compare Consolidation Loans

Finding the best consolidation loan involves research and comparison. Look for companies with favorable terms and rates that suit your financial needs. Learn more about best consolidated debt loan.

Remortgage with Debt Management Plan

If you have a debt management plan, you may still be able to remortgage to consolidate your debts. Explore options for mortgages for debt consolidation to find suitable products.

Mortgages Bad Credit UK

Securing a mortgage with poor credit can be challenging but not impossible. Explore options with mortgage bad credit to find suitable products.

Interest Rates, Loan to Value Ratios, and Reviews

The interest rates and LTV ratios for various loan products vary based on the lender, the borrower’s credit profile, and the property’s value. Below is a table comparing interest rates, LTV ratios, lender fees, and valuation fees for different loan products.

| Loan Product | Interest Rate | LTV Ratio | Lender Fees | Valuation Fees | Reviews |

|---|---|---|---|---|---|

| Secured Loan (Good Credit) | 3.5% | 80% | £500 | £300 | ★★★★☆ |

| Secured Loan (Poor Credit) | 6.5% | 70% | £700 | £400 | ★★★☆☆ |

| Debt Consolidation Loan | 5.0% | 75% | £600 | £350 | ★★★★☆ |

References to Secured Loans to Pay Off Cabot Financial Debt Collectors

Secured loans provide a viable solution for homeowners looking to manage and repay their debts effectively. If you have debts collected by agencies like Cabot Financial, consider a secured loan to consolidate and manage your debt repayments.

Homeowner Loans to Repay Cabot Debt Collectors CCJ

Dealing with a County Court Judgment (CCJ) from Cabot Financial can be daunting. However, homeowner loans offer a way to repay such debts while potentially improving your financial situation. Explore options for secured loans to manage and repay debts effectively.

For more information on managing debt and exploring loan options, visit the following links:

- £10 000 loan

- 25k loan over 5 years

- loan for 50k

- secured loan online

- fast secured loan

- secured loans direct lenders

- secure loan for bad credit

- personal loan for debt consolidation

- large debt consolidation loans

- credit cards for debt consolidation

- best consolidated debt loan

- mortgages for debt consolidation

- mortgage bad credit