This page includes the questions most commonly asked about debt management plans, or DMPs, and answers to these questions.

The information provided may answer your questions, but if it does not, please get in touch with us. Jubilee Debt Management experts have the answers and are ready to help you to tackle your debt problem.

Would you please describe a debt management plan?

The DMP is an informal arrangement for people struggling to repay their monthly debt.

A debt management company (or charity) is the administrator. It negotiates with creditors individually and requests a freeze of interest and fees. The debtor issues a single monthly payment to the debt management company.

This affordable amount covers all debts included in the DMP. The debt management company submits the appropriate payment portion to each creditor.

This process occurs every month while (hopefully) the freezes on interest and charges remain in place. The debt management provider asks creditors to refrain from taking collection or legal action during the DMP period, provided that the debtor makes monthly payments as agreed. The provider also handles inquiries and letters from creditors. Once all covered debts are cleared, the DMP ends.

This plan offers several advantages:

- Reduced monthly payments

- A single monthly payment makes it easier to stay on track with debt repayment.

- Creditors may freeze interest and other charges

- Flexible enough to change based on your financial status

- Covered unsecured debts are cleared once the plan fully concludes

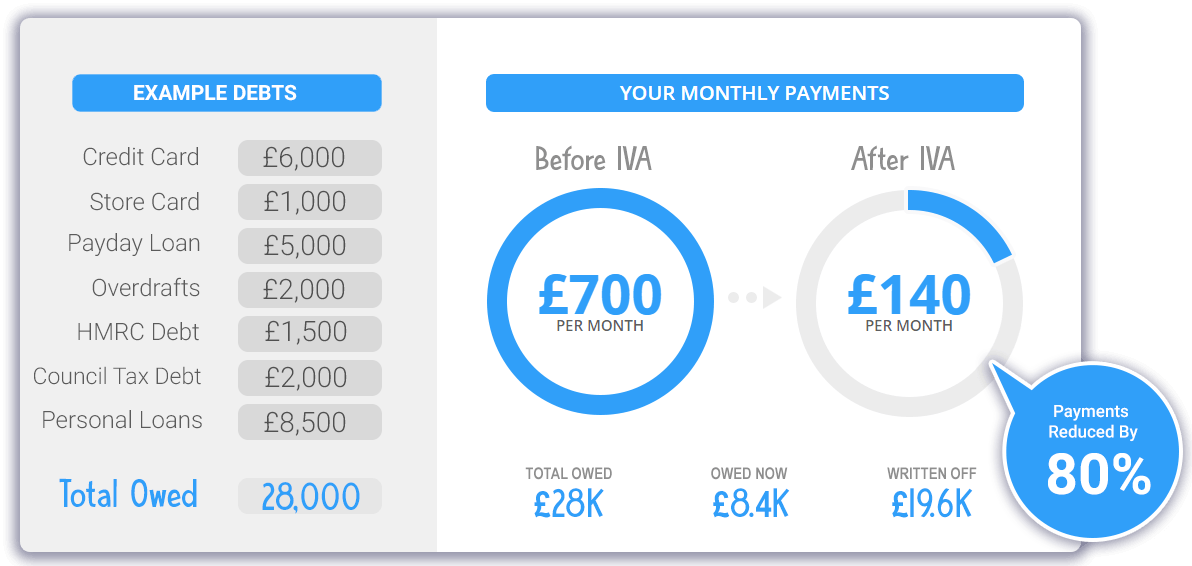

Discover How To Write Off 80% Or More Of Your Debt

Representation Of An Alternative But Effective Debt Solution

What debts are covered by a DMP?

Only unsecured arrears and debts may usually be included in a DMP. Any owned asset does not guarantee unsecured debts. Examples of unsecured debts include bank overdrafts, store cards, personal loans, and credit cards. Mortgages and some types of automobile loans are considered secured debts because an owned asset is used to guarantee them.

If I am a homeowner, will I qualify?

A DMP may be the best solution for you, regardless of whether you live with your parents, rent, or own a home.

Will creditor letters and phone calls continue while a DMP is in place?

As an informal arrangement, a DMP is not binding from a legal standpoint. Therefore, you will probably continue receiving creditor letters and telephone calls. However, this correspondence becomes much less frequent after the DMP is established and you submit regular debt payments.

Why have I received a Default Notice if I am in a DMP?

A DMP usually places you in default on your original credit agreements with covered creditors. Therefore, they are entitled to legally protect themselves by providing you with a Default Notice. While issuing a Default Notice “opens the door” to legal debt recovery action or a debt sale, there’s no guarantee this will happen.

Must I reveal my DMP to my partner?

It is usually best to keep your partner informed. After the initial shock, we typically find that they’re supportive. However, ultimately, it’s your choice whether to share this information with them.

How do I verify that creditors are being paid each month?

Creditor statements will continue to be sent to you periodically. Inspect these to confirm whether interest and fees are frozen. Compare statements monthly to verify declining balances for credit accounts. Your debt management plan provider should also issue statements periodically, and you can request one at any time.

Is it a loan? Is a credit check performed?

No, a DMP is not considered a loan, and a credit check is not required.

Will it affect my credit rating?

Your credit rating will be negatively affected since the total repayments established in creditor contracts will not be made under a DMP. The debts may already have been reported to credit reference agencies by creditors if you’re in default. As you move towards clearing your debts, you’ll have the opportunity to improve your credit rating again.

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 60-second Form

May I change the monthly payment established by my DMP?

Since this plan is informal, you may tailor monthly payments to reflect your financial situation, increasing or decreasing payments as needed when circumstances change.

Must I change banks or cancel direct debits?

To avoid double payments to DMP creditors, direct debit arrangements should be cancelled with them. However, direct debits for expenses like utility bills and car insurance payments not included in the DMP may remain. Switching banks is strongly recommended if your current bank is one of your DMP creditors.

This prevents the covered bank from keeping your wage payments to offset your debt.

Does a creditor have to accept an offer of reduced payment?

No, creditors are not required to accept any repayment offers less than the minimum contracted amount. However, they often accept such an offer if you can prove that you are serious about debt repayment and the amount is reasonable and fair.

Whether or not they have agreed to the reduced payments, they must receive any fees against your account.