Debt collection can be an uncomfortable situation for all involved.

Legal guidelines stipulate what behaviour is acceptable when attempting to collect debts. There are several laws regarding creditors’ harassment of debtors and generally accepted guidelines regarding unacceptable creditor behaviour. Consumers should become familiar with these to identify situations involving unfair treatment.

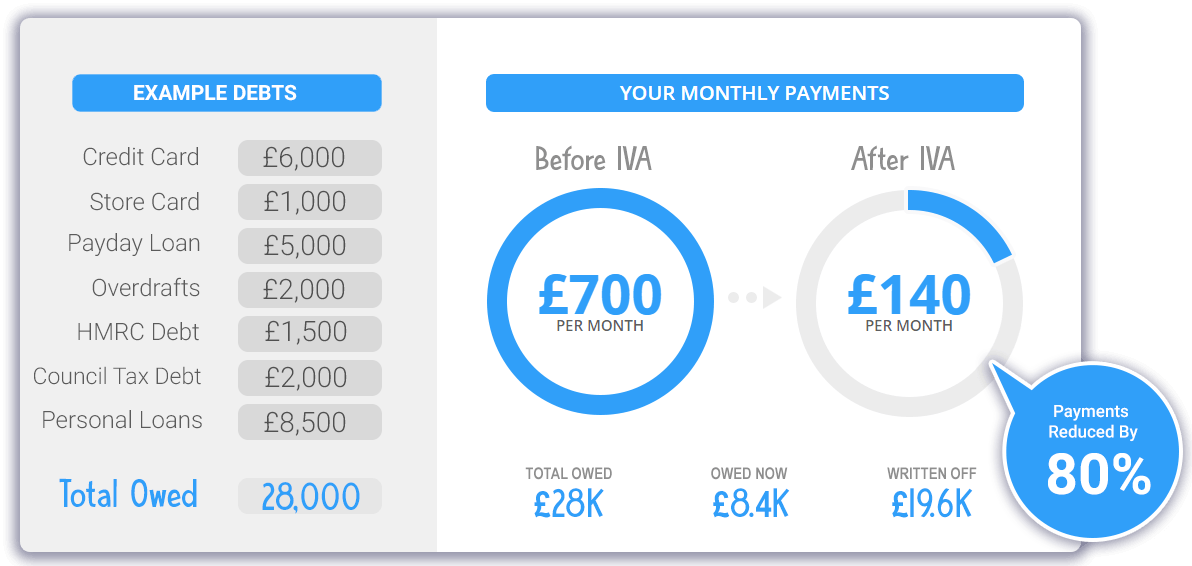

Discover How Crippling Debt Can Be Resolved

Administration of Justice Act 1970

Administration of Justice Act 1970 Section 40 explains that creditors or agents like debt collection companies acting on their behalf commit a criminal offence when they make monetary demands designed to create “alarm, distress or humiliation, because of their frequency or publicity or manner.”

If a creditor falsely implies that criminal proceedings will result from non-payment of a debt, it violates this Act. Creditors who impersonate court officials, bailiffs, or any other parties that they are not are committing an offence. An additional violation involves issuing a document that could be interpreted as being sent by a court.

Worried About Spiralling Debts? Here’s An Effective Debt Solution

Benefits of our debt solutions:

- Write off debt and lower monthly repayments

- Frozen interest and charges.

- No more calls or pressure from creditors.

- A fixed agreement typically lasts 5 years.

- Protection from unsecured creditors.

- An IVA may be an available debt solution.

The Protection from Harassment Act 1997

Engaging in harassment during the debt collection process is also deemed a criminal offence. The harassment may be verbal or written, including repeated calls during non-social times or to the debtor’s workplace. The Protection from Harassment Act 1997 considers it a criminal offence for a person to take any action that is known or should be known, such as harassing another person.

DEBT COLLECTION GUIDELINES

The Office of Fair Trading (OFT) details unfair practices regarding debt collection in its Debt Collection and Debt Management Guidelines. These guidelines apply to accounts in arrears or those with missed payments. They include a section about “contacting debtors at unreasonable times and intervals.”

Acceptable hours for contact are not listed in the document. However, examples regarding intervals and times that may be considered unfair are outlined. Making multiple calls at unsociable hours, contacting neighbours and informing them of the purpose of the call, and contacting a debtor at his or her workplace are included in the examples.

HOW TO HANDLE A HARASSING CREDITOR

Suppose you think a creditor has violated one of the above laws or does not comply with the OFT Guidelines. In that case, you should discuss the issue with the creditor or a collection company representing it. Before making contact, gather call and visit times and purposes and any emails or letters you consider threatening. Use this information to prepare a letter of complaint notifying the creditor or collector that you think it has violated one of the above Acts or the Guidelines.

The letter should include a request that the party immediately stop the behaviour. You should also provide a preferred method of contact and acceptable times to make contact.

If the creditor fails to change its practices after receiving this letter, submit a formal complaint to the Citizens Advice Bureau, Trading Standards, or OFT. If the behaviour of a bailiff, creditor, or collection agency ever becomes extremely threatening or violent in nature, notify the police immediately.