Jubilee offers a variety of home finance products for existing homeowners and home movers.

Remortgages

Regardless of whether you have an excellent credit score or a poor credit score, you may need to remortgage to get a better rate, release equity for debt consolidation, or maybe because of a change of personal circumstances.

Secured Loans for good and bad credit scores

It doesn’t matter if you want a loan of £50,000, a loan of £25,000 or even a higher amount. A secured loan is ideal if you want to keep your existing mortgage and borrow a larger amount of money. There are many options, including direct lenders with no fees, applications with an instant decision or online decisions.

If you have sufficient personal income and a less-than-perfect credit score, bad credit secured loans are very achievable, especially for debt consolidation.

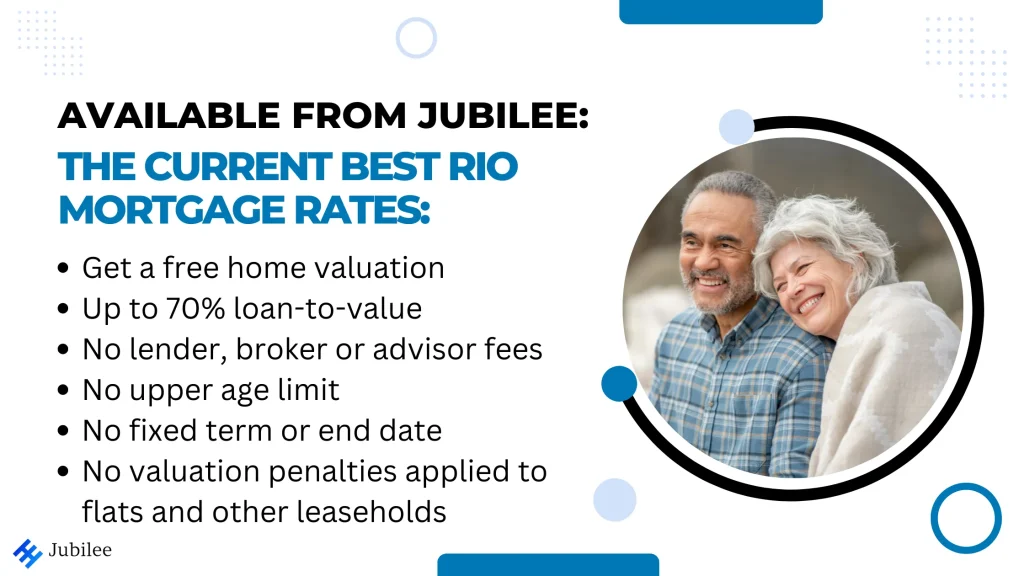

Retirement mortgages

Many people in retirement are approaching the end of the term of a standard mortgage each month. This does not necessarily mean that their income is low.

This is where retirement and interest-only retirement mortgages are ideal for pensioners with sufficient personal income. Some have excellent interest rates, like mortgages for younger people.

There are specific deals for people over the age of 55, over 60, over 65, over 70 and even over 75.

Home Equity Release for people over 55 years old

For people in retirement, especially those with a modest income, a home equity release or a lifetime mortgage could be an ideal way to raise capital or repay an existing mortgage at the end of its term or that can no longer be serviced. There are some big banks like Santander and Halifax and some dedicated lifetime mortgage lenders like One Family.

Some lifetime mortgage lenders allow interest-only payments.

Equity release under 55 years old

Jubilee has a new lender that offers equity release under 55 years old at excellent rates close to equity release rates offered to older people.

The lender is highly accepted even for flats and other leasehold properties.

Jubilee has access to various lenders and private solicitors who lend their own money to certain people in certain circumstances.