Starting in July 2026, Jubilee 2000 has a new lender, not featured on comparison sites, that offers bad-credit debt-consolidation loans to UK homeowners. Here are the key features

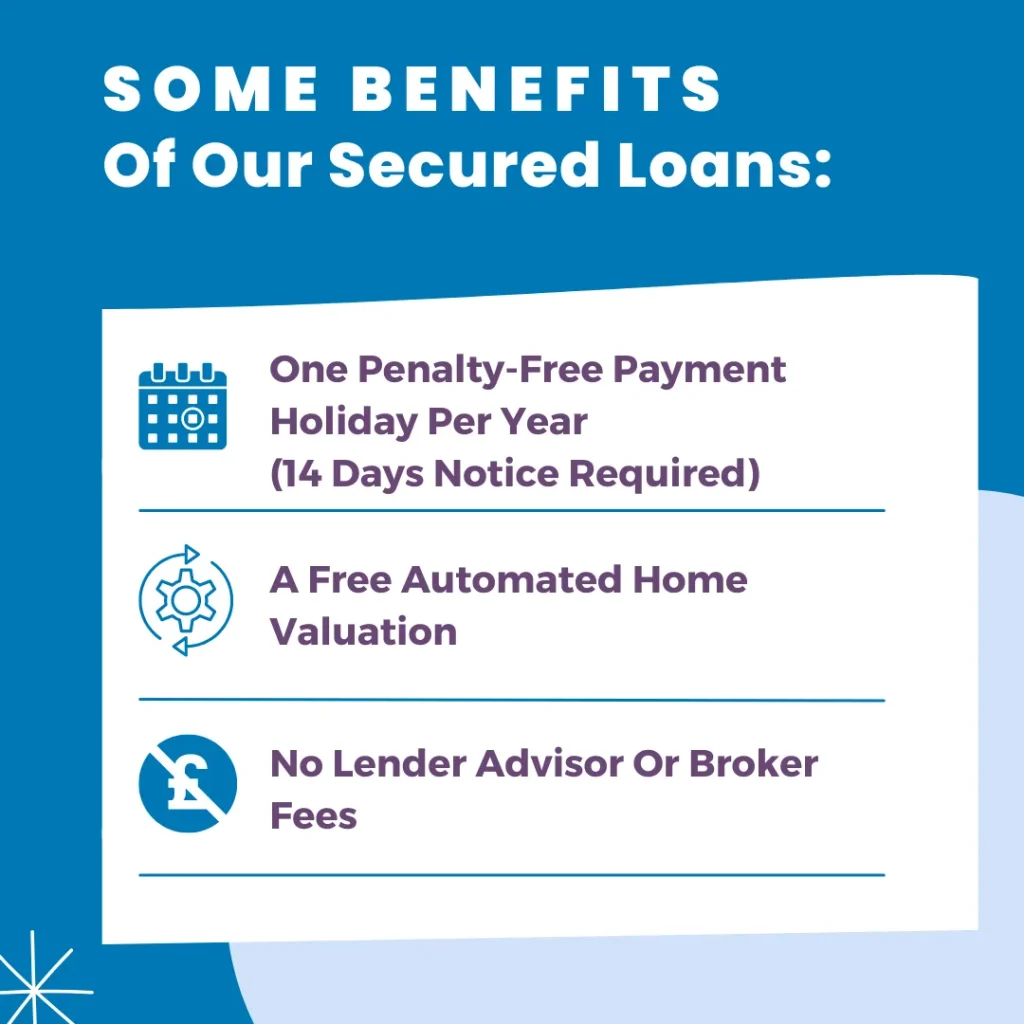

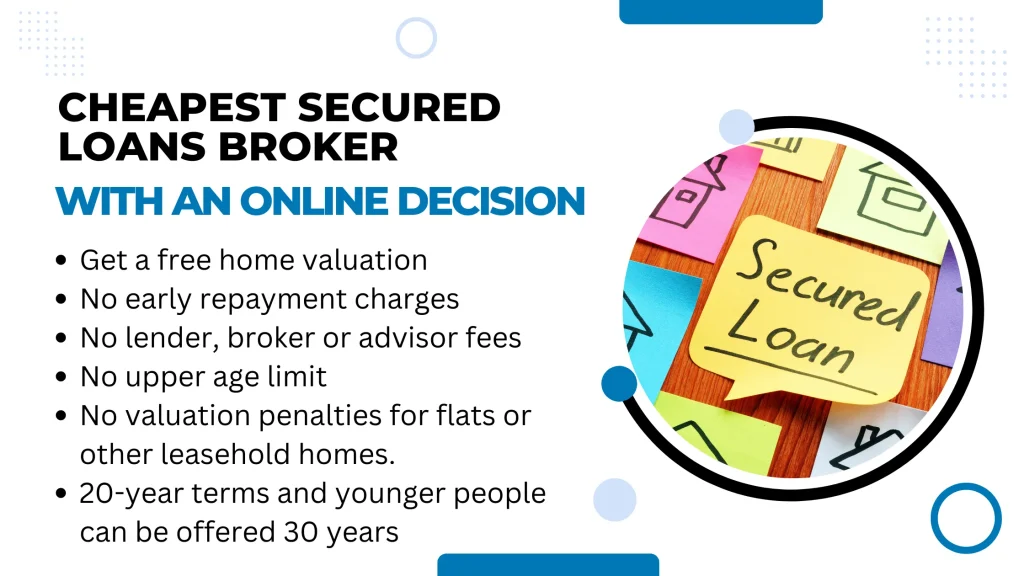

- Direct lender with no lender fees

- Instant decision based on soft credit search in the full application

- Free no obligation home valuation

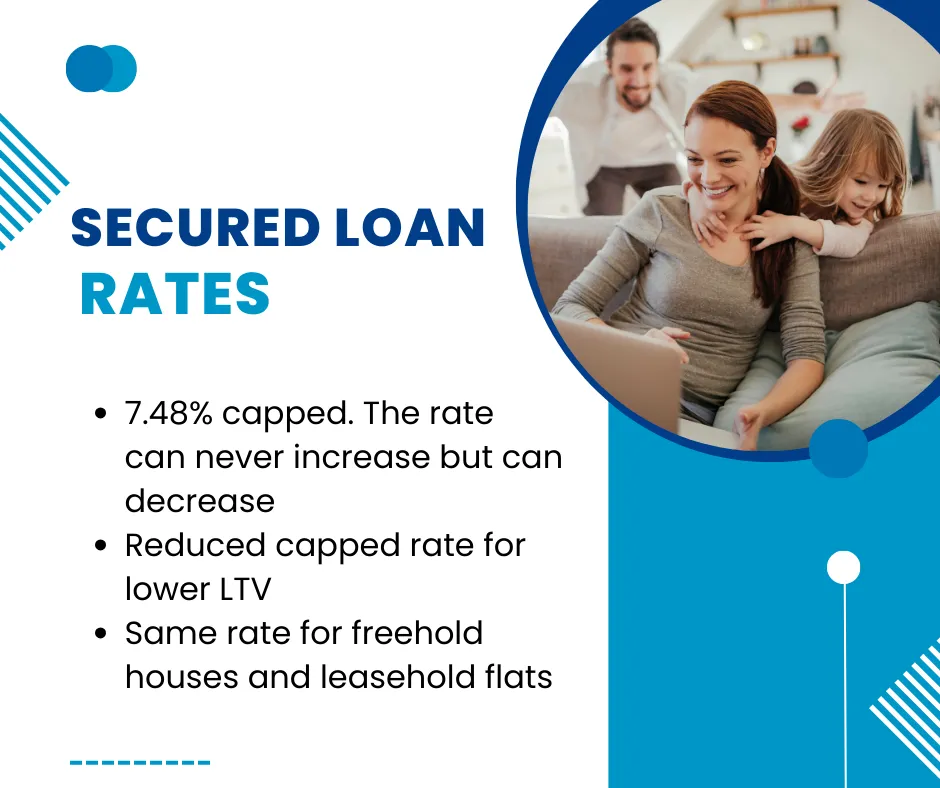

- 7.48% capped rate

- Up to 90% loan-to-value

- 2nd or 3rd charge on your home

- For existing mortgage payers only

- No broker, advisor or completion fees

- A flexible term enables up to one payment holiday per year

Please complete the form below for a decision in principle:

"*" indicates required fields

Getting a debt consolidation loan with bad credit

A bad credit history does not have to stop a homeowner from looking at debt consolidation. The starting point is usually the property’s equity, the mortgage balance, and whether the new monthly payment feels comfortable alongside the normal household bills.

A broader debt consolidation loan guide can help you see how a single secured loan may replace several credit card, loan, or store card payments.

Many applicants use a secured loan because it can give lenders more comfort than an unsecured loan. That is why secured loans for bad credit can still be worth considering where there is enough equity and the repayments fit the budget.

What usually matters to the lender

The lender will usually look at property value, mortgage balance, income, regular outgoings, and existing credit commitments. In principle, a soft search decision can be useful because it provides an early view without leaving the same mark as a full hard search.

Where you prefer to avoid a broker route, a direct lender secured loan for bad credit may keep the application more straightforward.

Some people also want to apply without involving a guarantor. A guide to a debt consolidation loan with no guarantor may be useful when the borrowing is secured by the home, rather than by another person’s promise to pay.

Rates, loan-to-value, and the size of the loan

The rate offered often reflects the loan-to-value, the credit profile, and the term. A lower LTV can be more attractive to a lender, while a higher LTV may still work if the income and property position are strong.

The current Bank of England Bank Rate is 3.75%, so a rate around two percentage points above that would be about 5.75%. Actual secured loan pricing can sit above or below that level depending on the lender’s appetite, the LTV, and the credit file.

For a closer look at pricing, the page on debt consolidation loan interest rates explains why secured, unsecured, capped, and fixed options can produce different monthly payments.

| Loan route | Indicative rate range | Typical use |

|---|---|---|

| Secured debt consolidation loan | 5.76% – 8.24% | Combining credit cards, loans, and store-card balances |

| Higher LTV homeowner loan | 6.84% – 9.48% | Larger borrowing where there is enough property equity |

| Unsecured consolidation loan | 12.65% – 24.90% | Smaller borrowing without using property as security |

Working out how much to consolidate

It helps to write down each balance, each current payment, and each interest rate before starting the application. That makes it easier to compare the existing monthly cost with one new loan payment.

If your balances are modest, the guide to a £10,000 loan to clear debts may suit the borrowing you have in mind.

Where the balances are larger, a homeowner loan for £25,000 debt gives a more suitable reference point.

For substantial card, loan, and car-finance balances, a large debt consolidation loan may show how higher borrowing can be set up over a longer secured term.

Before you apply, a secured debt consolidation calculator can help you estimate interest and monthly payments for different loan amounts.

How can the application move quickly

Good preparation can make the process feel much smoother. Have payslips, bank statements, mortgage details, proof of identity, and the latest mortgage balance ready before the lender asks for them.

The page on how long a secured loan takes explains why automated valuations and complete documents can shorten the path from decision in principle to completion.

Some borrowers prefer a fast online route, and an instant decision secured loan can give an early answer before the full underwriting work is completed.

What to do with credit card balances

Credit cards are often the first debts people want to consolidate because rates can be high, balances can move slowly, and several payment dates are easy to miss. A credit card debt consolidation loan can turn those separate card balances into one planned repayment.

The main benefit is simplicity. One payment is easier to track, and a fixed or capped secured loan can make the monthly budget feel calmer.

Readers who want the practical upside can also compare the benefits of debt consolidation loans before deciding which debts to include.

Where the goal is to shorten the overall plan, the guide on how to pay off debts with a consolidation loan sets out how term, rate, and payment size work together.

Homeowners, landlords, and remortgage options

A standard homeowner loan is usually secured against the main home. The page on how homeowner loans work gives a simple explanation of equity, loan-to-value, and second-charge borrowing.

Landlords may need a different route, especially where the borrowing is connected to a rental property. The buy to let secured loan guide covers borrowing against a residential rental property.

Some homeowners compare a secured loan with a debt consolidation remortgage, particularly where the existing mortgage rate, early repayment charges, and new mortgage term need to be weighed together.

Using a broker or applying directly

A broker can be useful where income is unusual, the credit file has older issues, or the property type needs a more careful match. A secured loan broker with an online decision tool may help you compare options before a full application is submitted.

Another route is to use a lender that handles the application directly. The guide to debt consolidation loans for bad credit explains how a direct-lender approach can work when the borrower wants to consolidate existing credit commitments.

Questions people ask before applying

Can I get a consolidation loan with bad credit?

Yes, homeowners with previous credit problems may still have options. The lender will usually consider home equity, income, current mortgage performance, and whether the proposed payment is affordable.

What credit score do I need?

There is no single score that suits every lender. Some lenders focus more on equity, affordability, and recent conduct than on the score alone.

Can I use the loan to repay cards and personal loans?

Yes, many secured consolidation loans are used to repay credit cards, unsecured loans, store cards, high-rate car finance, and similar commitments.

Where can I read more before applying?

The debt consolidation frequently asked questions page is useful if you want short answers before completing the form.