Do you have concerns about your financial situation? Did you know that an IVA online calculator can be a practical first step in exploring options to manage your debt?

This page explains how such calculators work and whether an Individual Voluntary Arrangement is suitable.

What is An Online IVA Calculator?

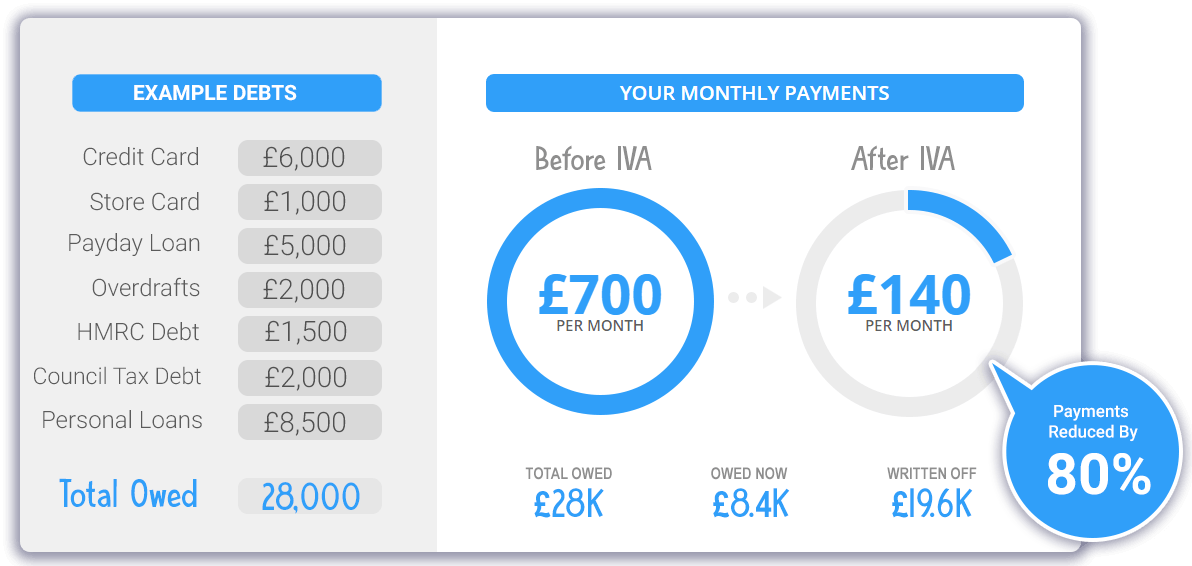

An online calculator for an IVA is a quick way to get an immediate insight into the amount of debt you can get written off and how much you still need to pay back to creditors if you successfully enter into an Individual Voluntary Arrangement.

Why Take The Jubilee IVA Test On This Page?

- We have excellent relationships with prominent UK creditors with exceptional IVA acceptance rates.

- Simple for you – no complicated forms to complete

- Rapid service – Jubilee IVAs typically take 4-5 weeks to get approved

- We’ll happily discuss your financial situation to decide whether an IVA is the right option for you.

Your 60-Second IVA Calculator Debt Test

Your 60-Second IVA Calculator Debt Test

How An IVA Could Radically Reduce Your Debts

How Does An IVA Calculator Work?

In the UK, an IVA calculator approximates the average amount of debt that could be written off by entering an IVA arrangement. Calculators are predominantly free offerings by debt management companies, Insolvency Practitioners, or free debt advice organisations that provide debt counselling, such as the National Debt Service.

All IVA calculators have slightly different parameters set into their calculations, which relate directly to the average amount of money that the calculator provider has managed to write off for their clients.

The average payable debt of 30% of the total amount outstanding is a widely used calculation, and most calculators represent this on their slider controls. As you move the calculator slider up to the level representing your outstanding amount, one box displays the total outstanding amount payable, and the other, the total debt written off.

What Is An IVA In The UK?

In the UK, an IVA is a formal, legally binding agreement between your creditors and you mapping out a proposal to pay back your outstanding debts over a fixed period. As a legally binding document, an IVA receives approval from a court of law, and creditors cannot take further legal action to force the repayment of outstanding sums owed.

How Long Does An IVA Last?

As a formal arrangement, the length of an IVA is agreed upon when creditors accept your proposal. The standard size is five years, but it can be shorter if you offer creditors a lump sum payment to settle the debts.

How Can an Online IVA Calculator Help Me?

As mentioned, an online IVA calculator helps you understand how much you owe and can get written off should you enter an IVA debt arrangement. As such, it is a valuable tool, but it is only the first part of a longer process. A calculator does not tell you whether you will qualify for an IVA.

Speaking to Citizens Advice, the National Debt Service, or an Insolvency Practitioner is advisable to determine if an IVA is an appropriate plan for your circumstances. An Individual Voluntary Arrangement can only be drawn up using the services of an Insolvency Practitioner who will thoroughly assess your outgoings and income and produce a repayment proposal to present to your creditors.

A good Insolvency Practitioner will explain all the options available before entering an IVA and refer you to documentation highlighting if a voluntary arrangement suits you. A practitioner can apply for an interim court order to stop a creditor from taking legal action as the IVA sets up.

It should be pointed out that employing the services of a debt management company is likely to increase the cost of an IVA as they will charge a fee in addition to the fees charged by Insolvency Practitioners.

What Are the Qualifying Criteria For An IVA?

To qualify for an IVA, a proposal containing a statement of Affairs, including monthly income, assets, and liabilities, is presented to your creditors. Through your Practitioner, they then choose whether to accept or reject your proposal.

The following essential criteria generally need to be met as a basis to put forward an IVA proposal:

- The total amount of outstanding unsecured debt must be at least £10,000 to make an IVA economically viable. Lower amounts from £7,000 can be a consideration, but the fees involved make an IVA an expensive debt solution.

- An outstanding amount of borrowing must be in place with at least two unsecured creditors.

- Following all your monthly bills and living expenses, at least £50 a month must be available for an IVA.

- If you cannot pay back all your outstanding unsecured borrowings in a reasonable time frame.

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 60-second Form

Are There Alternatives To An IVA For Debt?

Individual Voluntary Arrangements may not be an option for your circumstances, and there are alternative solutions:

Debt Relief Order

A DRO is similar to bankruptcy but targets those with few to no assets or surplus income and debts below £15,000. Once a DRO is in place, payments towards unsecured debts are suspended for one year; beyond that, if your circumstances are no better, any outstanding borrowings in the DRO are written off.

Debt Management Plans

A DMP is where a debt management provider will speak to creditors on your behalf and negotiate a single, lower monthly payment. It differs from an IVA because it is an informal repayment plan, meaning creditors can still pursue further legal action. A debt IVA is legally bound, meaning creditors cannot pursue further legal action. A debt management plan does have the consequence that it will show on your credit file as having been issued with a default notice.

Debt Consolidation

A debt consolidation loan amalgamates all your separate loans into one manageable payment, which may be at a reduced rate or paid over a more extended period. Financial consolidation aims to reduce your monthly loan payments.

Bankruptcy

Bankruptcy declares that you can no longer pay off your unsecured debts. Bankruptcy can be self-triggered or by a creditor to whom you owe considerable money. It is considered the final option if no other debt solution is viable. It takes less time to put in place than an IVA arrangement, but you can lose assets, including your home and control of your finances is passed over to the official receiver. A final consequence is an adverse effect on your credit rating.

How Much Will I Pay On An IVA?

In an IVA, creditors would expect you to pay back at least 25% of the original debt once the costs of the IVA, such as the Practitioner’s fees, get deducted from the monthly payment. IVA payments are typically based on affordability, but there is also a direct relationship between your outstanding debt and how much creditors expect to be paid.

Summary

An IVA calculator is a useful online tool that approximates how much debt can be written off by entering an IVA arrangement. A calculator does not help you understand how to deal with your financial problems, though, and you should use it as a trigger to receive prompt guidance to get your outstanding debt under control.