Do both you and your partner have debt problems and fear bankruptcy?

Did you know that you can jointly work on a debt solution to help you become debt-free in 60 months? Read on to find out how a joint IVA can help provide you with financial peace of mind.

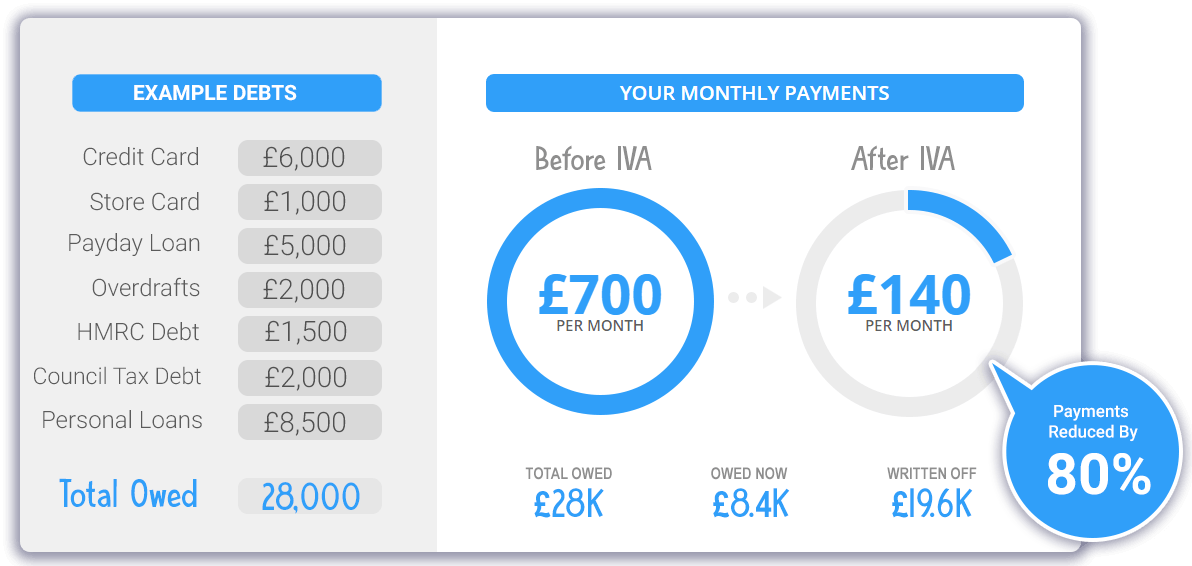

Your 60-Second Debt Joint IVA Calculator Test

How An IVA Could Greatly Reduce Your Debts As A Couple

How Does An IVA Work?

An Individual Voluntary Arrangement (IVA) is a debt management solution designed as an alternative to bankruptcy. It needs to be set up by an Insolvency Practitioner. It is a legally binding agreement between your creditors and you to pay back debts over a period, typically five years. It is approved by a court, meaning the creditors must abide by the terms.

What are Joint IVA’s?

Under insolvency legislation, a couple cannot offer a joint proposal to creditors for an IVA. However, they can individually present a proposal to creditors if they are both insolvent. If both proposals are approved, they can be jointly arranged, administered, and paid into individual payment plans using the same Insolvency Practitioner. All repayments under an IVA are first paid to the Insolvency Practitioner who then distributes the monthly payment to creditors, keeping a small portion to cover fees for administering the IVA.

Joint Proposals For An Interlocking IVA

A joint IVA is also known as an Interlocking IVA, as creditors must approve both sets of proposals they receive from each partner. If a creditor accepts one proposal but rejects the other, then both proposals are considered as rejected.

An interlocking IVA recognises the financial dependency of two partners upon each other. Each partner may have their creditors and their separate assets such as a car. Also, they may have joint debts due to holding joint assets such as a house.

When applying for an IVA, a Statement of Affairs put forward to creditors by each partner will differ relating to assets and liabilities. A Statement of Affairs will also include a joint income and expenditure statement where the joint living expenses of the partners are proportionate to each of the couple’s separate income. The calculation of the monthly payment takes account of the disposable income resulting in the higher-earning partner paying a more significant proportion of the arrangement.

For creditors, interlocking proposals for IVAs are often seen as attractive as the administration costs are lower than if each partner submits a plan for their own separate IVA. Additionally, jointly owned assets, such as a house, are handled in a similar way, which may not be as uniform in two separate IVAs.

Is A Joint IVA Right For Your Circumstances?

An Interlocking IVA may be appropriate for your circumstances in any of the four following scenarios:

- You have at least two separate creditors.

- You do not want direct dealings with your creditors.

- Your debts are more than £10,000. Due to the fees involved, for smaller sums, other debt solutions may be applicable.

- You have sufficient funds to make an IVA monthly payment.

The Advantages Of An Interlocking IVA For You As A Debtor

For a couple who have debt concerns, an interlocking IVA can be a viable solution to tackling your debt issues:

- A single lower and affordable monthly payment

- Stop legal action and the stigma of bankruptcy.

- An IVA is confidential between you and your creditors; unlike bankruptcy, there is no reporting in local newspapers.

- You receive full protection from creditors who cannot bring further action once an IVA is in place.

- All interest and charges cease.

- IVAs can help safeguard both your car and home.

- Any unsecured debts typically clear within 60 months

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 60-second Form

Do You Need To Live Together To Apply For A Joint IVA?

An interlocking, joint IVA is usually used by cohabiting partners who may be married, unmarried or civil partners.

However, cohabiting partners need not be in a relationship. Two financially independent people who cohabit could technically apply for an interlocking IVA.

Joint IVA and Divorce or Separation

If a cohabiting couple is romantically involved but split up during an IVA, it does not mean that the debt plan arrangement will fail. The two interlocking IVAs can be administered separately, allowing both former partners to make separate payments. The only risk lies with one partner being unable to maintain payments due to moving out and having additional living expenses.

Are There Alternatives to an IVA?

There are alternative solutions to an Individual Voluntary Arrangement, and include the following:

Debt relief order:

A debt relief order (DRO) is for those who owe less than £20,000, have few to no assets and have no more than £50 available to pay for debts after they have paid their monthly bills and other living expenses.

Debt management plan:

A debt management plan reduces the cost of monthly debt. The administrator of a debt plan negotiates an affordable single monthly payment with your creditors. A debt management plan has more flexibility than an IVA, as the monthly payment amount can be changed, and the plan can be cancelled.

Bankruptcy:

Bankruptcy is often the fastest and cheapest way to rectify an outstanding debt issue. It does have consequences including having your name listed in a local paper, a negative impact on your credit rating and even implications when trying to get a job.

Debt consolidation:

A debt consolidation loan is an option if you have a fair credit rating and is available jointly or individually. The consolidation replaces several unaffordable debt payments through a single, more manageable amount.

Cash Windfalls and IVA’s

The windfall is typically paid to creditors if you receive a cash lump sum, such as an inheritance during an IVA, whether individually or under an interlocking arrangement. Even when an IVA has finished, creditors may be entitled to some windfall proceeds. Reliable debt advice is available from Citizen’s Advice should you receive a cash windfall.

What are the Next Steps?

If you decide that an IVA may be appropriate for your situation, two routes can take you forward. You can either contact a licenced Insolvency Practitioner directly. An approved list is available on the UK government website, or you can contact your nearest Citizen’s Advice Bureau for guidance on your situation.