Moorcroft Debt Recovery is a collection agency part of the Moorcroft Group. It is the biggest debt collection agency in the United Kingdom.

Have you received phone calls, letters or even had one of their debt collectors come to your home to harass you about debts? Find out the facts that Moorcroft doesn’t want you to know.

Stop Moorcroft In Their Tracks

End Worry, Remove Stress, Take Action Today.

Who does Moorcroft Group collect for?

If you have a lot of debt, it’s important to know what debt Moorcroft Debt Recovery could be contacting you about. Moorcroft Debt Recovery mainly collects council tax debts, but they also collect County Court Judgment-Related debts, which are quite serious and can lead to bailiff action.

In addition to those types of debt, Moorcroft Debt Recovery also works with specific companies to collect debt, here are some of them:

- Credit cards

- United Utilities

- Virgin Media

- Court orders

- HMRC self-assessment debts

- HMRC tax credit over payments

- O2

- Loan debt

- Npower

Moorcroft Debt Recovery contacted me, what should I do?

When a person receives phone calls or letters to their home from Moorcroft, one of the first things they think is: what do I do? The first thing you should not do is panic. Many people who receive phone calls or letters from Moorcroft Debt Recovery start off by panicking or thinking they are being scammed.

To start, Moorcroft Group is a legitimate company, as it is registered and regulated by the Financial Conduct Authority (FCA). Thus, reaching out to people who have debt with their clients is a legal practice. So, you’re not getting scammed, but you do owe someone money.

Once you have figured out your debts and who you owe them to, a good next step is to speak to a debt advisor about your options. Everybody’s debt is different, and what action you take against it is unique to your situation. A debt advisor will be able to advise you on what specific action you should take.

While discussing your debts with an advisor, you will likely be contacted by Moorcroft Debt Recovery again. Their pushiness can be overwhelming and irritating, so knowing your rights is important. Moorcroft Debt Recovery has the same legal power over you as the company that you owed the money to in the first place.

This means that Moorcroft Debt Recovery can chase you to pay off your debts, but they cannot be aggressive by harassing you or entering your home to demand assets to repay your debt. Essentially, it will be impossible to ignore Moorcroft Debt Recovery, but we can help you learn how to deal with it better.

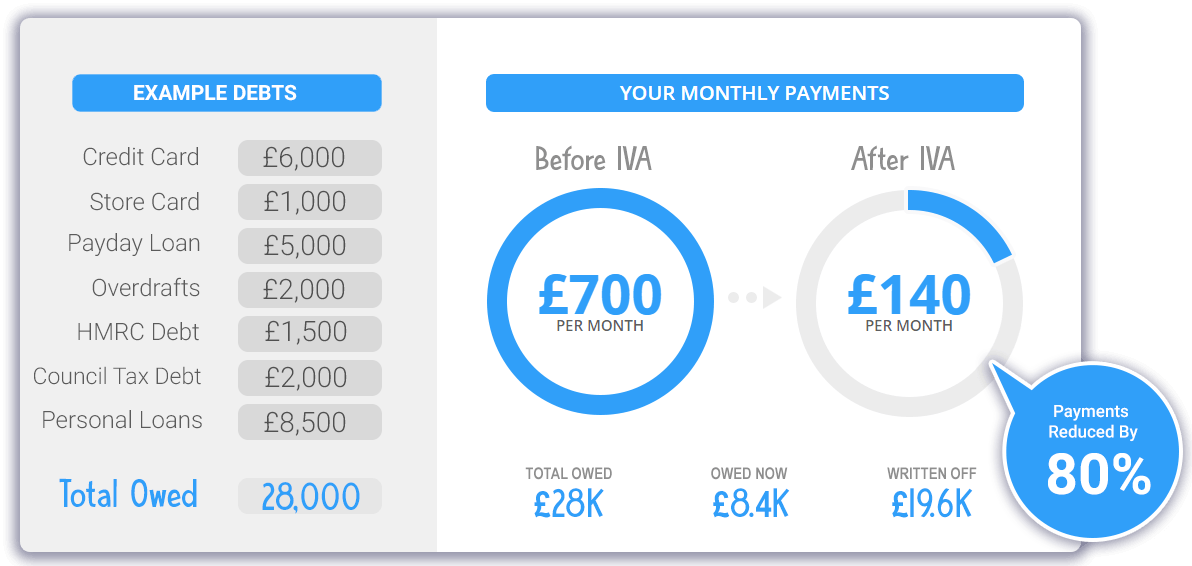

How An IVA Could Radically Reduce Your Debts

Online Forums Are Full Of Posts From Worried People Having to Deal With Persistent Debt Collectors:

How do I deal with Moorcroft Debt Recovery?

As we previously mentioned, everyone’s debt is different, and so is how they deal with it. If you have talked to a debt advisor, they may have advised you to create a debt management plan, apply for an individual voluntary arrangement or a debt relief order, file for bankruptcy, or pay your debt off.

While merely paying your debt off may seem like the easiest and least detrimental solution, it is not feasible for many.

Many people get into debt by buying a home and missing mortgage payments, using credit cards and being unable to pay them off, or even small things like not paying a phone bill for a few months. If a person had money to pay off these debts, they probably wouldn’t be in debt in the first place.

So, what is a more realistic solution to stop Moorcroft Debt Recovery from contacting you? Get your debt written off! The government may be able to help you write off 80% of your debt as they have a scheme called Individual Voluntary Arrangement (IVA). This is an agreement you make with a collection agency to pay back a certain amount of your debt either monthly or as a lump sum.

The rest of your debt will then be written off. Not everyone can qualify for this, but you may be eligible if your debts are over £1,700 and you have more than one debt.

Ultimately, paying off your debts or getting them written off is the only way to get Moorcroft Debt Recovery off your back for good.

Set up a repayment plan

If you can’t get your debt written off or pay it off immediately, other options remain. Moorcroft Debt Recovery’s number one goal is to get paid. If you talk to them and work out a repayment plan, they will likely agree to it. This way, they will still get some money at one point or another rather than getting nothing from you.

Your repayment plan will depend on your debt and how much you can pay a month. Do not agree to any repayment terms with Moorcroft Debt Recovery that you cannot commit to. Missing these debt repayments can cause even more of a headache than you had before.

Moorcroft Debt Recovery may also accept a partial repayment of your debts. This means they will take a certain amount from you and write off the rest of your debt. This can be a good option for those who cannot afford to pay off their debt, but this may show on your credit score.

A partial debt settlement will show on your records, making it harder to get a loan, a new credit card, or a mortgage. The best way to find out if and how much of your debt you can repay is by creating a budget.

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 30-second Form

How to create a budget

If you don’t already have a monthly budget for how much money you can spend and how much of your debt you repay, now is an excellent time to create one.

Start by writing out your expenses, such as how much you spend on utilities, groceries, and other necessities. What income you have left after budgeting for necessities should then be allocated to paying off your debt.

You may not want to allocate all of your leftover income if you will put some into savings. In this case, take a percentage, say 50% of your leftover income and allocate that to debt repayment.

Whatever number you come up with is the one you should discuss with Moorcroft Debt Recovery to get them to stop contacting you.

What happens if I can’t pay Moorcroft Debt Recovery?

If you can’t immediately repay your debts, get them written off, or even set up a repayment plan, you may wonder what action Moorcroft Debt Recovery will take. Unfortunately, they will continue to contact you. Many have tried blocking the number Moorcroft Debt Recovery calls from, but they will call from another number. They will start to send debt collectors to your door as well but don’t forget you do not need to let them in legally.

Moorcroft Debt Recovery has been known to pretend to be bailiffs at people’s doors to try to get people to open up. They can only send bailiffs to your door if they have already taken you to County Court. If the collection agency took you to court and the County Court Judgement favoured Moorcroft Debt Recovery, bailiffs can then come and repossess some of your assets to pay off your debts.

Other debt options – debt relief order

Although we discussed applying for an individual voluntary agreement and various ways to repay your debt, these are the only options for paying or getting rid of your debt with Moorcroft Debt Recovery.

If your debt is less than £20,000, you don’t own a house, and you have less than £50 of leftover money a month, you may be eligible for a debt relief order. A debt relief order is a one-year agreement in which you do not have to make any repayments to Moorcroft Debt Recovery.

Similarly, Moorcroft Debt Recovery cannot add interest to your debt or chase you for it. When the year is over, your debts to Moorcroft Debt Recovery will be written off. This may sound like a good deal, but the debt relief order will stay on your credit history for six years.

Having a poor credit history will impact your ability to get a mortgage, new credit cards, or other loans. If you are not in a position to repay your debts to Moorcroft Debt Recovery, a debt relief order may be a good choice for you.

Filing for bankruptcy

You have likely heard of filing for bankruptcy before, but do you know the nitty-gritty details of doing so? It is not a decision that should be taken lightly, but filing for bankruptcy when owing debts to companies such as Moorcroft Debt Recovery may be the only option for some people.

You can file for bankruptcy if your debts are at least £5,000. You can apply with an Insolvency Service for a fee of £680. However, the fee must be paid before you can declare bankruptcy, which deters many people from filing.

If your application is approved, your assets will be taken unless you need them for work, such as when using your car to commute. You will also have to give up control of your bank accounts. With so many conditions and losses, especially with how bankruptcy will negatively affect your credit history, filing for bankruptcy should only be a last resort when trying to get rid of your debt with Moorcroft Debt Recovery.

Can I lose my home to Moorcroft Debt Recovery?

If you cannot pay your debt to Moorcroft Debt Recovery and they are threatening to take you to court to repay your debt, you are likely wondering if not repaying your debt could lead to you losing your house.

Unfortunately, losing your home is a possibility, albeit a small one. The chance of you losing your house is small because the debt you owe is likely unsecured, meaning it is not secured against assets such as your house. This is only if you do not owe a secured debt, such as a second mortgage.

So, Moorcroft Debt Recovery could take you to court to appeal to them to secure your debt against your house, but it is unlikely to come to this.

What if Moorcroft Debt Recovery is breaking the law?

Although Moorcroft Debt Recovery can be intimidating as it persistently chases debtors, it operates under the law. If you do, however, feel that Moorcroft is doing something illegal or mistreating you, you can complain about them.

Reaching out to someone in charge at Moorcroft is a good first step. They may assign you a new caseworker instead. If that doesn’t help, contact the Financial Ombudsman Service instead. This is a government body that will look into your complaint against Moorcroft.

Frequently Asked Questions

How does Moorcroft Debt Recovery make money?

Like many collection agencies, Moorcroft buys your debt for a lower price from the companies you owe it to. Their aim is to get more money from you so they can earn money.

Can Moorcroft Debt Recovery take me to court?

Yes, they can. But, you cannot go to jail for your debts owed.

Is Moorcroft Debt Recovery able to come to your house?

As they are not bailiffs, they can come to your house, but they have no legal power over you or your assets. This means you do not need to talk to them or let them in.

Will Moorcroft give up?

Although you may think Moorcroft will give up if you ignore them for long enough, they won’t. If they don’t chase you, they won’t make money. That being said, debt collectors can only chase a debt for a maximum of 6 years.

Are debts written off on their own?

Your debts are only likely to be written off after the 6 years is up. Otherwise, you can apply to get part of your debt written off.

How can I pay Moorcroft?

If you do have the means to pay Moorcroft, you can pay them online, over the phone, by bank transfer, cheque, or credit card.

Moorcroft Debt Recovery Limited

- 2 Spring Gardens, Stockport SK1 4AA

- Main Telephone: 0161 475 2970

- Moorcroft Debt Recovery general enquiries – 0330 123 9765

- Other Known Numbers: 01619687065, 01614752875

- Reg Number: 1703704

- Website: https://www.mdrl.co.uk/

- E-Mail: customerrelations@moorgroup.com