Bankruptcy is sometimes viewed as a last resort for debt management. However, it might be the best choice for some people.

If you are considering bankruptcy and live in England or Wales, read on to find answers to the most common bankruptcy questions. We recommend that you then call us so we can explore your debt management options and suggest the best way for you to work towards debt-free.

Bankruptcy Or IVA, What’s Best? Find Out Below

What is bankruptcy?

The legal process of bankruptcy is used by individuals who are unable to repay their debts. It allows people to free themselves from the burden of debt and get a fresh start. People can initiate bankruptcy themselves, or a creditor who is owed more than £750 can initiate it.

During bankruptcy, some types of assets might be sold by an appointed person, called the “trustee in bankruptcy”. Proceeds are used to cover costs and will subsequently be distributed to creditors to recoup as much money as possible.

Bankrupts with surplus income may be required to contribute towards their debts for three years. Once a bankruptcy concludes, the creditors it covers may not make additional claims for the debt. Bankruptcy has negative aspects for some individuals.

The information is kept on a publicly available register, access to credit is restricted and some people may experience professional or contractual issues connected to their work.

How long does bankruptcy last?

A UK bankruptcy typically lasts 12 months until discharge. However, where it is affordable, individuals with surplus income might be expected to continue contributing to the costs and their debts for a further 24 months (36 months in total).

Income payments are defined in an Income Payment Agreement (IPA) or an Income Payment Order (IPO). Once discharged, an individual is no longer considered to be bankrupt, even if income contributions are to continue. However, the effects of bankruptcy in terms of credit access can last for several years.

How does bankruptcy affect credit rating?

Call Credit, Equifax, and Experian are the three credit reference agencies in the UK. They maintain records regarding credit accounts. Bankruptcy will be recorded on your credit file. This record will remain on your file for a period of six years.

In addition, if a consumer does not make contractual payments on debts, a default notice might be placed on his or her credit file. Accounts included in a bankruptcy will commonly be marked in default but lenders should update this notice once the bankruptcy is discharged.

Graphical Representation Of An Alternative Debt Solution

How does the court process work for a bankruptcy?

You will need to contact the Court that handles bankruptcy work for the area in which you live. This will enable you to make an appointment for your hearing. Upon arrival, you will need to provide the bankruptcy clerk with your properly completed application forms and the relevant fee. The hearing should take place afterwards.

At the hearing, the court formally reviews the application and decides whether to grant your bankruptcy. Provided that you are technically insolvent, have properly completed the application form and have paid the appropriate fee it’s likely that your bankruptcy petition will be granted. You may be asked whether you have taken advice prior to choosing to apply for bankruptcy.

What happens after the granting of a bankruptcy order?

Once the court issues a bankruptcy order, the office of the Official Receiver is notified of the situation. A bankrupt might be asked to remain in Court for a short period to hold an initial telephone appointment with this office. They may then choose to schedule a follow-up telephone appointment with the individual or schedule that the individual attend their offices for an in-person interview to discuss their financial situation.

The Official Receiver gathers information regarding assets, income, expenditures, and conduct prior to bankruptcy. The purpose is to establish whether an individual is in a position to contribute to the bankruptcy costs and debts through their assets and income.

Should I seek bankruptcy advice?

It is essential to obtain professional advice regarding bankruptcy and other debt management options. The Insolvency Service, courts, and other official bodies will not guide the best approach. However, we at Jubilee Debt Management are qualified and happy to do this. We will review your financial situation and offer advice regarding the best debt management solution.

Will I lose everything if I go bankrupt?

If you make yourself bankrupt, some types of assets automatically go into the possession of the Trustee in Bankruptcy. Assets may include (but are not limited to):

- Interests in property, even if the property is jointly held with a partner or spouse building society or bank account balances

- Lump sums from an occupational or private pension if this investment matures during bankruptcy bonds, shares, savings policies, and endowments individual possessions of significant value, such as motor vehicles or expensive jewellery (you might be permitted to replace these with lower-cost versions)

You may also be required to pay a portion of your weekly or monthly wage, as required by a court income payments order or with your consent. The payment listed in an income payments order is based on the contribution of all surplus income and will normally run for three years following the bankruptcy date.

This will mean that your budget for living costs will be somewhat restricted, though you should be assigned sufficient funds to cover necessary and reasonable living costs.

The Trustee is authorized to dispose of relevant assets without your consent where required. You can keep furniture, basic household items, bedding, and clothing. You may also keep items necessary for employment, such as books, tools, and a vehicle.

If you acquire assets during the bankruptcy period, the Trustee must be informed, and the asset might be realized for the benefit of creditors. Qualifying assets might include a significant bingo, football pool, or National lottery windfall, inheritance of cash, property, investments, or valuable assets, and money received after the bankruptcy date but before the date the bankruptcy is discharged.

Will anyone know that I am bankrupt?

A bankruptcy order is no longer ordinarily advertised in a newspaper. However, the details of bankruptcy are included in a public bankruptcy register that can be accessed online. The Insolvency Service maintains this register. Your creditors, individuals, and companies will be informed of the bankruptcy.

These include building societies, banks, secured loan companies, mortgage companies, hire purchase companies, insurance and pension companies, and others you owe money to.

Will my job be safe during bankruptcy?

Some jobs may be affected by bankruptcy. For example, membership in professional bodies may cease, forcing the individual to stop performing in the current role. Refer to the terms listed in your contract of employment, ask your employer for more information and consult any relevant regulatory or professional bodies.

What happens to a bank account during bankruptcy?

Once a bankruptcy order is issued, bank accounts are often closed. You will be allowed to open a new account. A restricted number of banks and other financial institutions will usually be prepared to offer you basic banking facilities for the term until you are discharged.

Will a bankruptcy write off a student loan?

A student loan taken before 1st September 2004 might be included in a bankruptcy. Take advice from your Trustee in this respect. The Student Loan Company should be listed as a creditor, and the individual should stop making monthly payments to this company upon the instruction of their Trustee.

The loan may not be written off through bankruptcy if it was taken out after this date. If payments are being deducted from salary and the individual goes bankrupt, these deductions will continue until the student loan is repaid. Individuals who earn less than the income threshold for student loans will not be required to make payments until their salary reaches the designated level. However, interest will still accrue according to the agreement entered with the Student Loan Company.

What are the debt management alternatives to bankruptcy?

When bankruptcy is not the most suitable choice or the negative aspects serve as deterrents, the following alternatives should be considered:

Establishing an informal arrangement with creditors involves writing to each one to explain your financial status and reach a mutually agreeable solution regarding an affordable repayment plan for the debt.

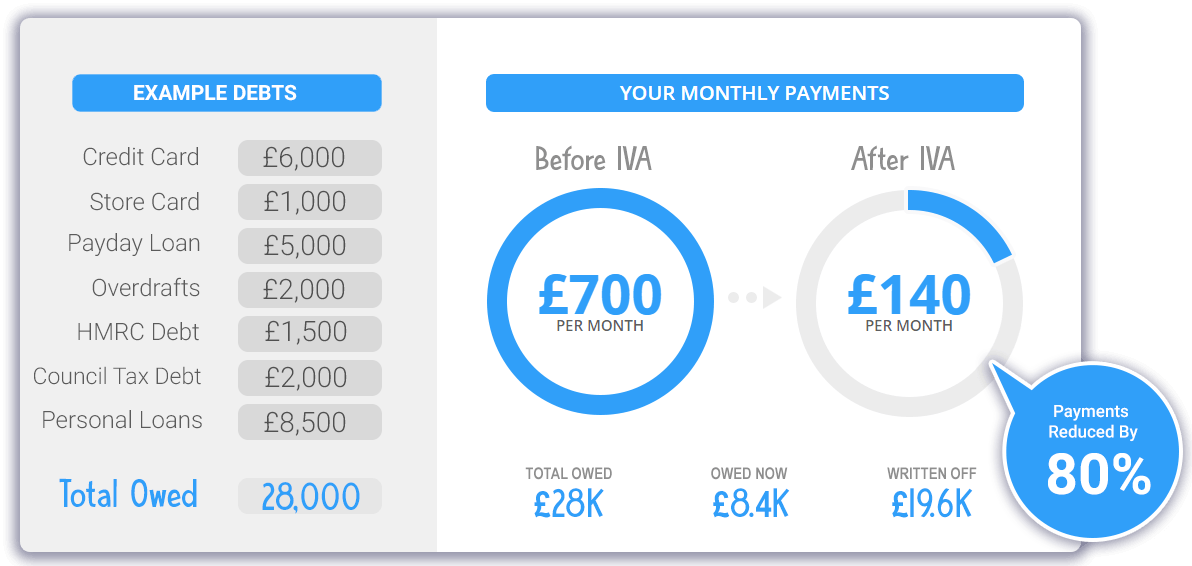

An Individual Voluntary Arrangement, which is also called an IVA. This is a formal and legally binding contract for debt repayment, with terms agreed to by your creditors and via proposals from an Insolvency Practitioner.

Retaining a debt management organization to negotiate a monthly payment amount with each creditor. You must provide the company with the requested information and make monthly debt payments. The company will divide each payment amongst the creditors according to the arrangement. This process continues until the debts and any related interest or charges have been repaid.