Reduce Monthly Debt Payments and Legally Write Off All Unaffordable Debt (up to 80%)

IVA debt advice: If you’re struggling with debt, an Individual Voluntary Arrangement (IVA) could be the answer to your money worries. With an IVA, you’ll make a monthly payment you can afford – and at the end of the 5-year arrangement, any debt that’s left will be completely written off.

We’ve put together a straightforward guide that explains everything you need to know about IVAs

Including some common questions, some pros and cons, and how to apply for an IVA. If you don’t have time to read our full guide now, why not complete our quick questionnaire below, and we’ll estimate how much of your debt could be written off.

Government IVA? Discover how much debt you could write off

What is an IVA and is it right for you?

An individual voluntary arrangement (IVA) is a way of creating a legally binding agreement between you and your creditors to help you clear your debts.

Individual voluntary arrangements are available to residents of England, Wales, and Northern Ireland. If you live in Scotland, a Trust Deed is a similar solution.

Since an IVA is a ‘formal’ (legally binding) debt solution, you need an Insolvency Practitioner to help you apply and deal with creditors.

The good news is, from the point that your individual voluntary arrangement is being set up, your insolvency practitioner will communicate with all your creditors for you, which means:

No more calls and no more debt collection letters

According to National Debtline and Stepchange Debt Charity Scotland, debt is one of the biggest causes of stress and anxiety for people in the UK. Writing off your debts with an IVA will almost instantly put you back in control and stop your financial worries. You’ll pay off only as much as you can afford, and when the IVA is finished, any debt left is completely written off.

You don’t have to panic about any large upfront fees to set up an IVA either. There are costs involved, but insolvency practitioners build these into your affordable monthly payment.

Why not see if you qualify for an IVA now? Answer a few quick online questions and see how much debt you could write off.

How Our IVA Debt Advice Could Greatly Reduce Your Debt

Benefits Of Individual Voluntary Arrangements:

- There are no upfront fees to find

- The insolvency practitioner helps you determine an affordable repayment amount

- The insolvency practitioner deals with creditors, asking them to agree to the revised payment in the proposal

- During IVA establishment, the insolvency practitioners may be able to help secure a court order preventing creditors from taking further collection action

- If your circumstances change, you may be able to take a payment break or adjust your payments

- Covered creditors may not take further action to collect the money they are owed

- When the agreed terms have been met, the IVA typically ends and remaining covered debt is written off

Do I qualify for an IVA?

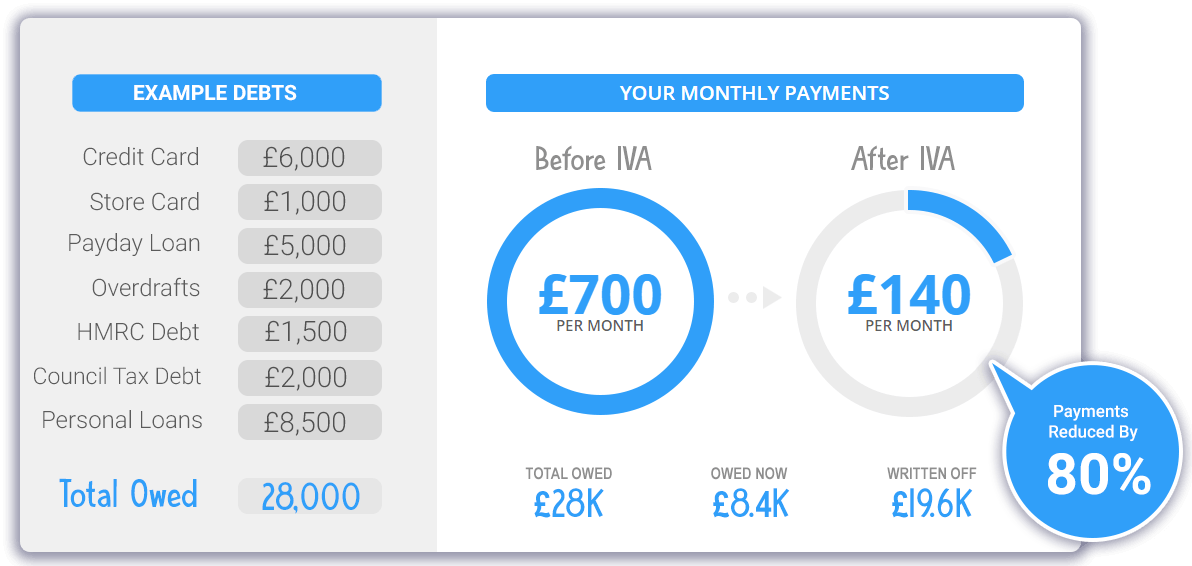

If you’d like to see if you qualify for an IVA, our 60-second form will mean we can give you a quick call with a straightforward answer. Assuming you have debt of £5,000 or more, owed to 2 or more companies, and have a regular income – the answer is likely to be yes. The great news is if you follow our IVA debt advice; an Individual Voluntary Arrangement is likely to be able to write off up to 80% of what you owe.

How do I apply for an IVA?

If you feel like an IVA could be the answer to your debt problems, the first step is always to talk to one of the team here at Jubilee. We’ll ask you a few questions to get a picture of your financial situation; then we’ll chat with you about the full process.

The steps will generally involve:

Step 1: Stopping or pausing any creditor action while your IVA is being set up

Step 2: Discussing your financial information in more depth to work out what an affordable monthly payment could be

Step 3: Putting together a proposal that will be presented to the people you owe money to and the court.

Step 4: A meeting will be called where the companies will vote on whether or not they should accept your proposal. As long as creditors representing 75% of the debt agree, then it will go ahead. This makes the IVA legally-binding.

Step 5: Your IVA is set up, and only your monthly payment needs to be made. You will no longer receive demands or calls from debt collectors or bailiffs.

Some IVA questions and answers

The Jubilee team help thousands of people get back in control of their debt every year. It’s absolutely normal to have some questions and concerns when it comes to your finances.

Take a look at some of the things we’re often asked about IVAs:

How long does an individual voluntary arrangement last for?

Normally, an IVA will last for five years. In some rare cases, it can be extended to six years.

When you consider that personal loans and credit card repayments can often drag on for seven years or more, an IVA is often a much quicker way of getting back in control of what you owe your creditors.

How does an IVA affect your life?

One of the biggest life changes Jubilee customers report to us is a huge reduction in stress that an IVA offers. You don’t have to worry about ignoring letters and phone calls from creditors – and any action (including legal action) they’re taking against you will stop.

While your IVA is in force, there are rules around not taking any further credit – like payday loans or credit cards. It’s not impossible to get credit if it’s needed, but you’ll have to get permission from your insolvency practitioner before you apply.

Essentially, having an IVA means you’ll just need to communicate with your insolvency practitioner about your personal finances. It’s their job to make sure you’re paying the one payment you can afford, so if your finances change (for better or worse), they’ll be there with advice and can make any adjustments to your IVA that might be needed.

When your IVA is complete, any debt that is left will be completely written off – and you’ll be free to start rebuilding your credit.

What happens if I don’t know all the companies I owe money to?

Don’t worry – it’s easy to lose track of debt, especially when it’s been passed to collection agencies.

As well as providing you with professional advice, your IVA company will be able to check with all the different credit reference agencies to create one full list of companies and amounts you owe.

Can I still have a bank account with an IVA?

Yes, but you might benefit from changing it if you have debts with your bank or another bank or company closely linked to your bank.

Nowadays, debit cards are used more frequently than cash – so you don’t have to worry about losing your bank accounts if you have an IVA. However, if your bank or a company they’re linked to is one of your creditors, you may find that they can take it directly from any money you have in your account.

In situations like these, the insolvency practitioner’s advice might include opening a different account – but you won’t be left without a bank account. You can learn more about the insolvency practitioners association here.

Will I lose my home with an IVA?

No, you will not. A major benefit of an IVA is that you will not be forced to sell your home.

In some cases, where someone has a lot of equity in their home, they may be required to remortgage to release that equity to use as a lump sum to pay their creditors. Insolvency practitioners that are experienced with IVAs will be able to tell you if this is likely though – so you can decide whether it’s an option you’d like to explore before you make a final decision whether to apply or not.

Is an IVA a good idea?

Individual voluntary arrangements aren’t right for everyone – but for tens of thousands of people every year, it’s an effective way to write off up to 80% of what’s owed to creditors and can have a positive effect on future living costs.

As with all debt solutions, it’s important to get professional debt advice – to help make sure an IVA would work for you and your personal circumstances. We’re always happy to talk to people who are considering an IVA – and we follow strict government rules to make sure you’re not pressured in any way.

When you talk to the team here Jubilee, you’ll get all the information and advice you need to decide whether an IVA or any other debt solution could work for you.

Will my monthly payments and interest and charges go up or down?

They might but interest and charges won’t.

Part of your insolvency practitioner’s role is to make sure you’re only paying what you can afford. So, if your cost of living suddenly increases or your income drops, your monthly payments could be adjusted to make sure you can still afford to live.

Likewise, if you’re suddenly promoted or win the lottery, you may be expected to pay back a little more towards clearing your debts.

You will normally have a review of your financial circumstances each year. This gives you a great opportunity to seek any on-going advice you might need.

How badly does an IVA affect credit rating/credit scores?

An IVA is recorded on your credit file, so your credit rating will go down.

However, for many people who are struggling with debts, action from creditors and debt collection agencies will already mean that your credit score has been damaged, so an IVA might not make as much of an impact as you think.

Even though your credit report record runs for six years, you’ll find that most lenders are concerned with your recent credit – so as your IVA gets older, your score will gradually go back up. When your IVA is marked as ‘complete’ – it will look even better.

After six years, the IVA will be removed from your credit report completely.

What does IVA stand for?

IVA stands for ‘individual voluntary arrangement’.

Although an IVA is a formal, legally-binding debt solution, it’s called an ‘individual voluntary arrangement’ because, unlike bankruptcy, you cannot be forced into taking one.

What is an insolvency practitioner (IP) and why do I need one to apply for an IVA?

An IP is a licensed, authorised and regulated professional who is qualified to offer debt advice and help to people or companies who are considering ‘insolvency’. Insolvency is the term used when a person officially declares that they cannot repay money they owe.

Since insolvency is a serious step that can see large amounts of debt written off, the law says that only an IP can offer debt advice and support to someone setting up an IVA.

Will anyone know I’ve got an IVA?

Debt solutions like IVAs and bankruptcy are recorded officially on the ‘Personal Insolvency Register’.

Although this is accessible by members of the public, it’s normally only used by financial professionals – so it’s unlikely anyone would search for you.

That said, some professions require that you declare any financial difficulty you run into. Financial services companies, the police, the prison service, and some government departments will require you to declare your IVA, and in some cases, it could jeopardise your employment in these kinds of roles.

What happens if I come into a lump sum of money during my IVA?

If you inherit, win, or otherwise come into a lump sum of money while during an IVA, you should let the insolvency practitioners handling your case know so they can offer professional advice.

Depending on how much it is, you may be required to make a lump sum payment towards clearing your debts – but this would depend completely on the amount of money and the debts involved.

Comparing an IVA to other debt solution arrangements

An IVA isn’t the only way to get back in control of your debts. Here, we’ve looked at how an IVA compares to some other popular debt arrangements in England, Wales, and Northern Ireland.

IVA vs Debt Management Plan

We’ve talked about an IVA as a ‘formal’ debt solution; a way of handling debts that is agreed by everyone involved and then protected by law when it comes into force.

A debt management plan is a little different, as it’s considered an ‘informal’ way of dealing with your debts. This means it will not be recorded on the personal insolvency register or your credit file, and instead, it is simply agreed with each individual creditor.

With a debt management plan, you’ll be expected to repay everything you owe – but your monthly payments and the repayment term will usually be adjusted to fit around what you can afford. An IVA will usually last for five or six years with any remaining debt written off at the end – but a debt management plan will usually last as long as it takes to pay off the full amount.

Since an individual voluntary arrangement is protected by law, all action from your creditors will stop, and they cannot demand more than they are being paid. With a debt management plan, your creditors are really just acting on goodwill – so they can demand that the arrangement is changed if they decide to.

We can offer advice on setting up a debt management plan if this is what you decide to do.

IVA vs Bankruptcy

We’re often asked if an individual should go bankrupt or choose an IVA. In actual fact, bankruptcy and IVAs designed for different personal financial situations.

If you can afford to pay back something towards your debts (even if it’s not as much as your creditors might want) – then an individual voluntary arrangement will often be the best option. However, if you simply cannot pay anything towards your debts, bankruptcy could write some or all of your debt off with no payments.

Although bankruptcy might sound more appealing since there could be no monthly payments needed, you could lose control of your possessions and face having your home, car, or other property sold to try to settle as much debt as possible. Bankruptcy will have more of an impact on your credit file too.

If you decide you’d like to explore bankruptcy as an option, we can help.

What kinds of debts can be included in an IVA?

Individual voluntary arrangements are designed to help people handle ‘unsecured debts’ – the name given to money owed for things like personal loans, credit cards, payday loans, and other debts that are not secured against a property or an object.

These debts can include:

- Credit card debt or unpaid credit card balances

- Money owed to family or friends

- Personal loans

- Overdrafts

- Catalogue debts

- Debts owed to HMRC

- Income tax arrears

- Council tax arrears

- Payday loans

- Other unsecured debt

- Debts relating to overpayments of benefits

- Gas and electricity bill arrears

- Water bill arrears

- Many types of credit agreement

There are certain debts and types of debt that cannot be included in an IVA. They include:

- Secured loans

- Mortgages (if you still live in the house)

- Child support arrears/maintenance arrears

- Hire purchase agreement (if you still own the product)

- Student loans

- Guarantor debt

- Limited company debt

- Rent arrears for your current home

- Police fines or court fines

- Car finance (if you still own the car)

- National insurance debt

- Log book loans (if you still have the car)

Arrears on financial commitments like child support payments or secured loans will need to be discussed with the lender or agency in question. These are considered ‘priority debts’ and should be addressed urgently. Don’t panic though; if you’re contacting us about an IVA, we’ll be able to give you further advice relating to these types of payments.

What is an IVA: A Summary From Industry Experts

We appreciate that there’s a lot of IVA information to take in – so we’ve summed up the key points here for an iva proposal:

- An individual voluntary arrangement is designed for UK residents who have a significant debt level and cannot afford their current monthly repayments for unsecured debts.

- An individual voluntary arrangement normally lasts for five years.

- An insolvency practitioner regulated by the financial conduct authority must handle the IVA process for you. They will negotiate with people and company you owe money to and agree on an overall amount you can afford to repay each month. All data protection regulations will be adhered to during this time.

- As long as creditors representing 75% or more of the debt agree, your IVA will be set up.

- When an IVA is set up, the people or companies you owe money to will no longer be able to pursue you for repayments and any action they have brought against you will stop.

- At the end of the IVA, any debt that remains is completely written off – giving you a chance to start rebuilding your finances. We can offer you free advice without obligation.

Disadvantages of an iva:

- Unlikely to be available if your unsecured debts are less than £8,000.

- Only an authorised individual can establish it.

- You must prove that you can afford regular debt payments and your budget will be restricted during the term of the IVA.

- When you cease making payments directly to your creditors, your accounts will fall into arrears or further into arrears.

- Insolvency practitioners charge a fee to negotiate with the people and companies you owe money to and to manage the IVA.

- Creditors representing more than 75% of the debts must approve it.

- Any debt not included in the IVA such as hire purchase agreements will remain outstanding afterwards.

- An IVA will be recorded on your credit file and will make getting credit more difficult in the future.

Get IVA Debt Advice Now From Industry Experts

Almost everyone in the UK has some amount of unsecured debt – and for millions of people, debt is a problem that’s only getting worse with every passing day.

You’re not alone if you’re struggling with debt. We help hundreds of people regardless of employment status apply for an IVA every week. We’re here to offer judgement-free debt advice and help you on your journey to becoming debt-free.

Contact us today for free advice – the first step can sometimes feel tough, but if you take 60 seconds to complete our quick form, you’re one step closing to saying goodbye to your money problems.

Lower Monthly Payments & Write Off Up To 80% Of Your Unsecured Debt – 60 second Form