Debt collectors can be very unscrupulous and unethical

Sometimes, it has been known for them to bully and harass people who are not even liable for the debt! Threatening someone’s home address with “recovery actions” can be very stressful.

Let Us Understand The Nature Of Your Debt. Please Complete The Simple Form Below:

There is a popular saying that “an ex is an ex for a reason”

In some cases, the reason is that the person amassed a considerable amount of loan and credit card debt during the relationship. This unfortunate situation might reach the tipping point if the debt was accrued while cohabitating or by using credit accounts held jointly.

When the partner has finally had enough, the ex must move on. However, memories of the relationship may remain in the form of unpaid bills, a declining credit score, and calls and letters from collectors. Getting collection agents off your back may become a personal mission.

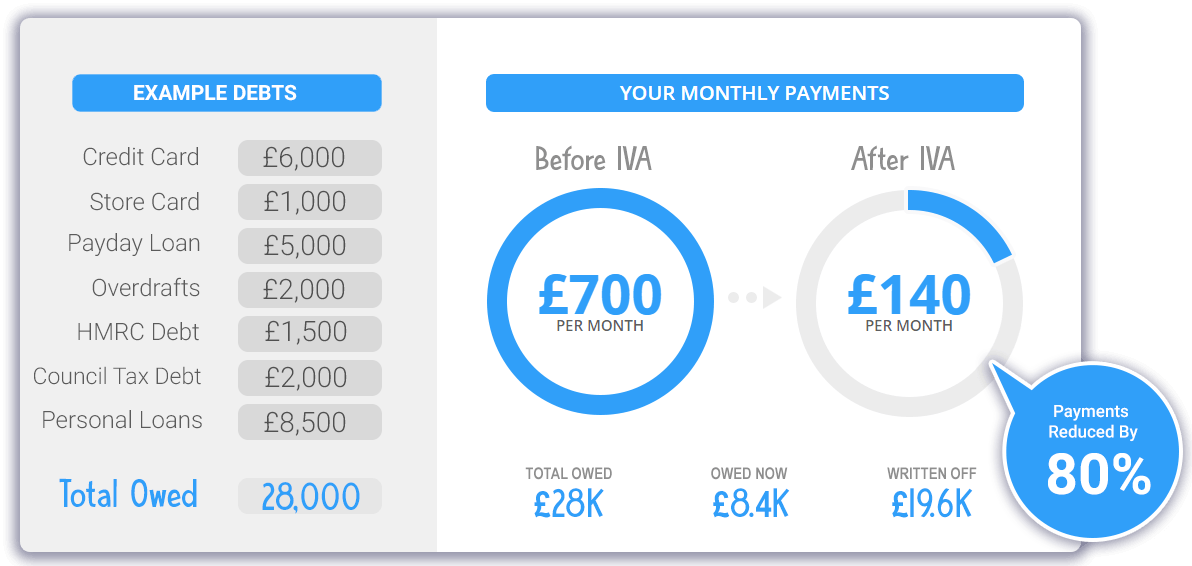

Graphical Representation Of An Effective Debt Solution

Benefits of our debt solutions:

- Write off debt and lower monthly repayments

- Frozen interest and charges.

- No more calls or pressure from creditors.

- A fixed agreement typically lasts 5 years.

- Protection from unsecured creditors.

- An IVA may be an available debt solution.

If The Debt Is Shared

If collectors are trying to find an ex who accrued debt on accounts held jointly with you, there may be no way to avoid them completely. Debt collectors can be very aggressive, and if they are unable to find the ex, you are the next person they will approach to collect money owed.

Their collection attempts often take the form of letters and phone calls from unrecognised numbers. Some collectors go to great lengths, making visits to the home, for example. Before letting this create too much stress, take a deep breath and learn how to deal with it.

The fact is that a joint credit account is the responsibility of both parties who signed the credit agreement. Therefore, if an ex spends the proceeds of a substantial joint bank loan and the relationship ends, each of the account holders can be held fully liable for the debt. If the ex is nowhere to be found, you may find yourself paying for his or her new clothes, shoes, furniture, and other items purchased.

Rather than attempting to prove that these expenses were not yours, you may have to consider fully repaying the debt to prevent damage (or further damage) to your credit history.

If The Debt Is In The Name Of An Ex Only

If an ex was the sole account holder on a debt that collectors are pursuing, there is nothing to fear. If the ex’s whereabouts are known, you may wish to provide the collectors with this contact information and request that they discontinue their calls and letters to your residence. You are under no obligation to provide the contact details of your ex, however.

Once they have an address or telephone number for the ex, they should use this and should leave you alone. If they do not, send them a letter requesting that they discontinue calls or messages to you. By law, lenders are not permitted to harass an individual, particularly someone who does not owe a debt.

When an ex is still on speaking terms, it is nice to give advance notice that debt collectors will soon be calling. This should give the ex enough time to arrange documents and finances to handle the situation. Of course, there is no obligation to provide this notice, but it may make life easier for all involved. One never knows whether an old spark could be rekindled after the ex becomes debt-free.

Addressing The Unscrupulous And Illegal Behaviour Of Debt Collectors

Most debt collection firms operate according to the law, but some are unscrupulous. Debt collection is a business, so collectors do not always care about the unfortunate tales of debtors, nor are they still inclined to make debt repayment any easier.

Collectors might receive a bonus based on the amount of debt they collect. It can be almost impossible to get them to negotiate the amount due unless they have been given some discretion by their employers in this respect. Some collectors demand the full amount of debt plus additional money for their own charges. Though collection firms sometimes purchase debt at a discount, they are in business to make money.

Collection methods typically begin with a letter requesting repayment. An unethical collection firm makes its letters look like court claims or other official government documents, a breach of debt collection guidelines established by the Office of Fair Trading.

Debt collectors also like to make collection phone calls…lots of them. They may call up to ten or more times a day, contacting every phone number associated with the account, including yours. Sometimes, they send a text message and request a return call on a premium rate number, another questionable practice.

Incessant calls and letters might be considered psychological harassment, which could be unlawful. Request that they stop and direct the collectors to the ex who owes the money. Unfortunately, this may not be the last of hearing from them, as many take drastic steps to collect the full amount of debt. Some continue to call and do so at unreasonable times and at work numbers when they have been asked not to.

Other collectors threaten to take action that is actually not within their power. They may even imply or state outright that failing to pay the debt is considered a criminal offence or that anything short of full payment will result in criminal proceedings.

Beating Debt Collectors At Their Own Game

If debt collectors are in hot pursuit to collect debts in the name of an ex only, inform them that the debts are not yours and request that they cease contact with you. If this does not work, send each of them a written letter as documented proof of request not to make further contact.

If the debt is held jointly and contacting the ex is not possible, pay the money if you can afford to and then consider whether it’s worthwhile trying to recover some or all of the money from your ex. It may be a fruitless task, but at least the credit score will not suffer additional damage. Above all else, prevent financial entanglements from occurring with a new partner. After all, one time is bad enough!