During January 2019, UK consumers used plastic cards 28.5 million times to make purchases, equating to £1.461 billion in spending.

Each second of that month, an average of 319 credit and debit card purchases were made. During this past February, the average adult in the UK used credit cards, unsecured loans, motor and retail finance, and overdrafts to borrow £4,235. The total amount of credit card debt during that month alone was an unbelievable £55.3 billion.

Discover How Your Credit Card Debt Can Be Sorted Out

Problems managing debt

Many UK residents cannot manage their debt, with one going insolvent or bankrupt almost every four and a half minutes. Credit Action publicized these and other statistics that illustrate how serious UK credit card debt has become. The agency formerly called the Association for Payment Clearing Services indicated that there are now more credit cards in circulation within the UK than there are people living in the region.

An estimated 14 million Brits make everyday purchases with credit cards and when they make late payments, skip payments, or overcharge their financial status declines. Eventually, the purchase cost may greatly exceed the sales price of an item. Consumers who find themselves with too much unsecured credit card debt should get help immediately.

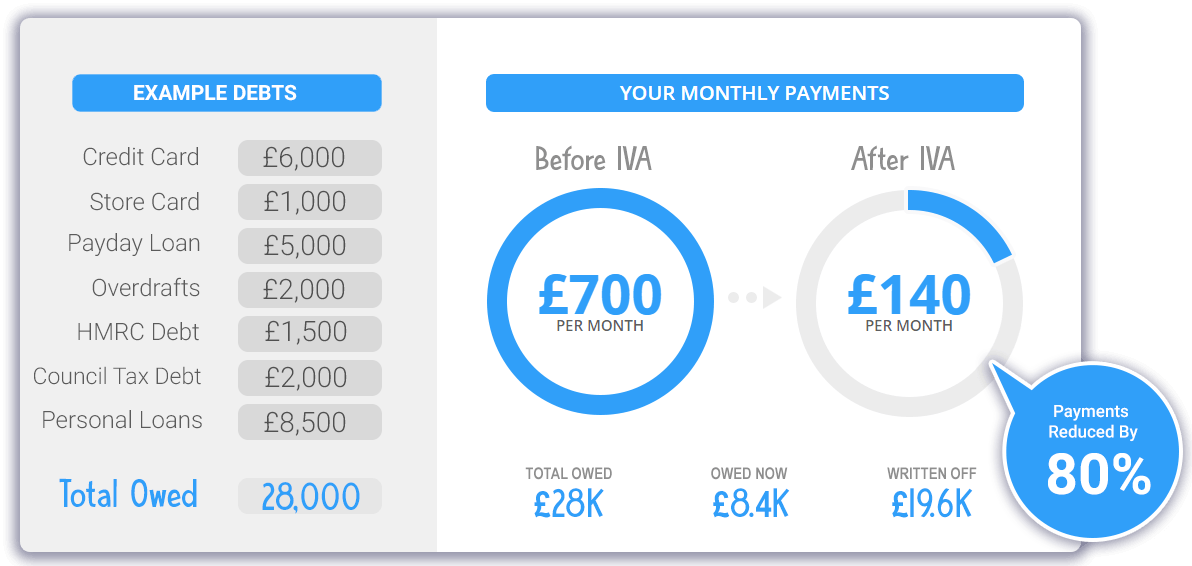

Graphical Representation Of An Effective Debt Solution

Benefits of our debt solutions:

- Write off debt and lower monthly repayments

- Frozen interest and charges.

- No more calls or pressure from creditors.

- A fixed agreement typically lasts 5 years.

- Protection from unsecured creditors.

- An IVA may be an available debt solution.

How To Manage Credit Card Debt

Redoing the personal budget may make credit card debt manageable. When other expenses are reduced, enough cash may be released to pay off credit card balances. Other consumers transfer their card balances to a credit card with an introductory zero percent balance transfer interest rate. Interest will not accrue during the introductory period, allowing the individual to repay the debt during this time, potentially without incurring additional charges.

These solutions are not suitable for everyone, so a consultation with a debt management professional is recommended. This expert reviews the amount of unsecured debt, including credit card debt, to determine which debt management solution is most appropriate. A Debt Management Plan (DMP), a Debt Relief Order (DRO), and an Individual Voluntary Arrangement (IVA) are some of the most common ways to manage credit card debt.

The Available Options In More Detail

DMP

A DMP is an informal debt solution administered by a debt management company or charity that negotiates a set monthly debt payment with each creditor. The debtor issues one monthly payment covering all debts. The debt management company receives this payment and allocates the proper amount to each creditor according to the DMP guidelines. The goal is for the debtor to fully repay all credit card debts.

Even though a creditor does not have to accept a DMP, many realize that they may not otherwise receive full repayment. People in debt should inquire whether the debt management company charges a fee and offers professional advice. Receiving objective information from an expert in the field allows people to identify a debt management solution without feeling pressured.

Consumers will understand how severe their debt issue is and feel reassured that their financial situation will improve with the help of an experienced professional

DRO

The formal arrangement called a DRO was established as an inexpensive alternative to bankruptcy. Low-income residents with less than £15,000 in qualifying debts should explore this tool created by insolvency legislation. A DRO usually entitles them to a one-year repayment amnesty and prevents creditors from taking action during this time. When the DRO ends, included debts are written off so the individual can begin with a clean slate.

An intermediary, who is an authorized independent debt adviser, is the only person who can grant a DRO. The £90 filing cost can be paid in several instalments. Before a DRO application is completed, people in credit card debt may wish to contact Jubilee Debt Management.

Our debt experts will identify whether a DRO is an appropriate solution. If so, they will explain debtor restrictions and help to signpost you to an intermediary who will assist with the completion of the DRO application.

IVA

The IVA is another formal insolvency program, this one designed for the repayment of a reduced level of qualifying debt. A write-off of the remaining amount of qualifying debt occurs at the end of the IVA period. Residents of England and Wales who are at least £8,000 in debt and have reliable income (or disposable assets) may qualify to enter this legally binding agreement.

With an IVA, repayments are negotiated with creditors and the debtor issues a single payment each month to cover all included debts. This arrangement resembles a DMP but with an IVA, an Insolvency Practitioner is responsible for creditor negotiations and payment allocations.

The only factor limiting IVA repayment amount is the financial situation of the individual in debt. With an IVA in force, creditors may freeze charges including interest and they are not permitted to attempt further action to collect debts. Two fees must be paid to establish an IVA and these are deducted from the amount creditors receive through debtor payments. A typical IVA runs for five years (6 years for some homeowners).

A DMP, DRO, and IVA have different advantages and disadvantages. Before pursuing these solutions, consumers should obtain complete details regarding each. This prevents surprises or unexpected restrictions that can increase feelings of frustration already being experienced due to the financial situation. Jubilee Debt Management professionals review the negative and positive attributes of each solution. They also help consumers determine which option is most appropriate.

Jubilee representatives are different from others in the industry because they provide professionally qualified advice. Each debt management option is covered in detail, and the representative never places pressure on the consumer. The information is provided by a Jubilee debt expert, but the decision is made by the individual in debt. This is the best approach because a debt management solution will not be successful unless the person using it is comfortable with it.

People who have fallen behind with making payments on credit card balances should get professional assistance now. By addressing the situation as soon as possible, debt becomes easier to handle than it will be if balances on credit cards increase.

Read the information on our site and contact us to learn more about managing credit card debt.