Are you close to losing control of your finances or perhaps they have already spiralled out of control?

There is a debt management option available that can help get creditors off your back, avoid bailiffs, and provide you with financial peace of mind knowing that your debts could be all paid off within five years.

The solution is an Individual Voluntary Arrangement or IVA. Like all debt plans, there are advantages and disadvantages of an IVA. To find out if the benefits of an IVA outweigh the cons for your circumstances, read our short guide to make an informed decision.

Find out how much debt you could write off – just answer 5 quick questions

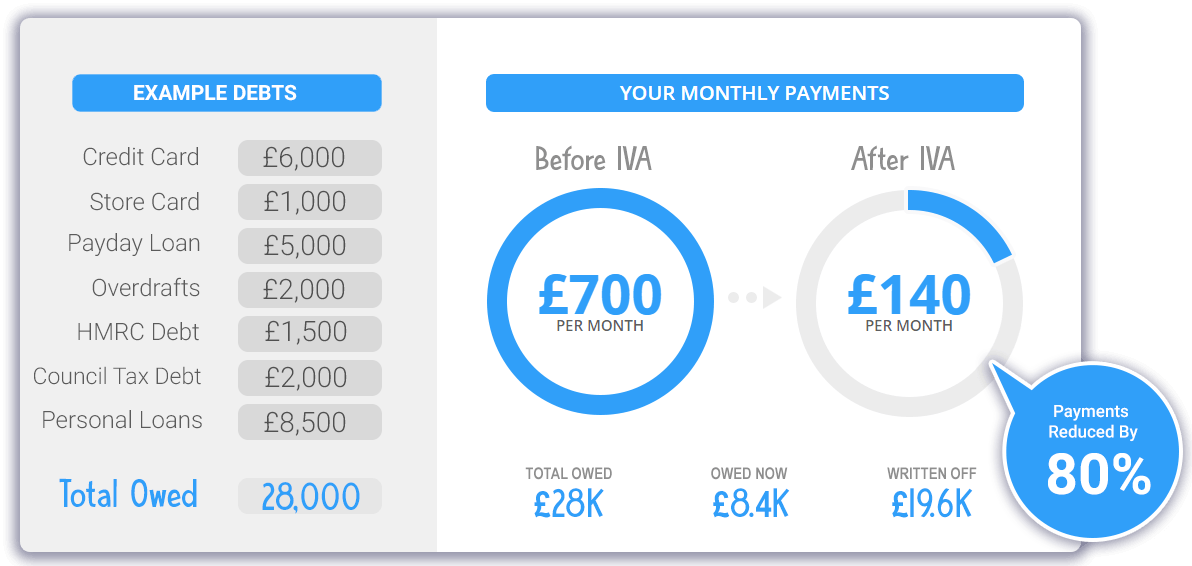

How An IVA Could Radically Reduce Your Debts

Is an IVA My Best Option?

An IVA is a legally binding and formal agreement approved in a court of law. Once creditors agree to and sign off on an IVA, no further legal action can be pursued, and no additional fees or charges can be added to the outstanding debt. Debtors commit to paying back a portion of the outstanding debt in one regular monthly payment over five years, which must be adhered to.

An IVA does not require a minimum or maximum outstanding debt size. However, fees, such as the cost of an Insolvency Practitioner (IP) to administer the plan, must be considered, meaning anything below £10,000 might make alternative solutions more viable.

Below are both IVA pros and cons so you can decide whether an IVA is suitable for you.

Pros of an IVA

Stops your debts from increasing

As soon as an IP starts working to put an IVA in place, they will quickly apply for an interim court order. As soon as this is approved, your creditors cannot move forward with legal action, such as requesting bankruptcy, while the IVA is set up.

Once the IVA gets approval, it means that your monthly payment is now fixed for the duration of the plan unless your circumstances change. Importantly, creditors are no longer able to add additional interest and charges to the original debt.

Affordable repayments

When an Insolvency Practitioner puts together your statement of affairs as part of your IVA proposal to creditors, they will make sure that the payments are affordable as it is in no one’s interest for your payment plan to fail. Your income and outgoings face scrutiny, and IVA payments must ensure you have sufficient funds to make the monthly payment and maintain an acceptable lifestyle where you can pay your bills and support your day-to-day living.

Eliminates legal action

Upon approval of your Individual Voluntary Arrangement, your creditors are unable to take any further legal action against you or contact you directly to request additional payments outside the IVA. An IVA needs a majority of 75% of creditors to approve your proposal to put an IVA in place. Provided the majority agree, the minority of disagreeing creditors are overruled and bound by the legally binding terms of the IVA.

Protect your assets

When you enter an IVA, an Insolvency Practitioner will have looked at your assets as part of your statement of affairs. It is not likely that you will have to sell your home or car when entering an IVA. However, if you hold a lot of equity in your property, you may be asked to release funds through a home equity release loan as part of the IVA to pay off some of your creditors.

An end to your debt

As part of your IVA, you undertake to pay back a percentage of your outstanding debts which is agreed by your creditors. After 5 years, at the end of the IVA it is designed to pay off all your debts. You will no longer owe money to your creditors, be debt-free and can work to rebuild your credit score and make a new start.

The end of stressful phone calls

Once you enter an IVA, your creditors are no longer able to contact you directly about your outstanding debts. Instead, the IP deals with a creditor now, including all correspondence and administration.

Protect your job

If you have an IVA, there is no restriction to the type of job you can undertake. It differs from bankruptcy, where there are restrictions. If you have been declared bankrupt, specific jobs such as civil servant roles and jobs in the financial sector will remain out of limits.

IVA Cons

Negative credit rating

Once you enter an IVA, your name is in the record on the Insolvency Register which can be viewed by the general public. Furthermore, a mark is entered against your name on your credit report confirming insolvency. Insolvency has a significant impact on your credit score as you flag up as struggling to pay back your debts, meaning that getting any further credit will be more difficult.

Windfall clause

A windfall should, on balance, be considered a disadvantage of an IVA. If you receive an inheritance, a company bonus, or any other payout above £500, your IP will bring this in as part of your IVA. It will pass to your creditors, which could see your IVA arrangement finish early, with surplus funds being returned to you, which is good. Unfortunately, you have no control over any windfall as it is in the hands of the IP.

Annual reviews

As part of the legally binding IVA arrangement that you signed, your financial status is reviewed annually throughout the five-year IVA debt plan. You are legally bound to increase your payments into the IVA if the review shows you have the means to do so.

Banking restrictions

Restrictions on your bank account are one of the main negatives of an IVA. Under the arrangement, only a basic bank account is permitted, meaning that you cannot have a credit card, chequebook, or overdraft facility on the account.

No option for cancellation

When you entered an IVA, you committed to a formal, legally binding agreement passed in a court of law to make monthly repayments to your creditors over 60 months.

The failure to maintain these payments will result in severe consequences, with the administrator of your plan (the IP) having the power to terminate your IVA and recommend that bankruptcy proceedings start.

Budget restrictions

When an IVA is put in place by an IP, it is designed to make payments manageable and so less likely to fail by making sure you have a surplus of funds to be able to pay your bills and live from day to day. However, the surplus money will only limit you to a modest lifestyle throughout the plan.

Not all debts can be included

An IVA is not a blanket agreement to clear all your debts. It is designed first and foremost for unsecured debt which includes credit cards, personal loans, and utility arrears. Secured loans are not considered for inclusion as part of an IVA. It means that debt that has an asset attached to it must remain outside an IVA. A mortgage and a car loan are two examples of lending that link to an asset.

To find out more information about whether an IVA could be a suitable debt option for your situation, we can help you here at Jubilee Debt Solutions. Contact us today, and our professional and hard-working team will be happy to provide debt advice and discuss the debt management solutions available to you.

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 60-second Form

Final thoughts – Is It Worth Getting An IVA?

Hopefully after reading this short guide on the pros and cons of an IVA, you will have a better idea of whether IVAs may be appropriate for you.

If you want an end to stressful calls from creditors and wish to protect your assets and protect your job, none of which are covered by taking the path to bankruptcy, then an IVA is a viable debt solution.