Have you been receiving threatening letters or phone calls from Lowell Financial LTD?

Lowell Financial Debt Collection hopes to collect the full debt owed from you in order to earn money themselves. If Lowell solicitors or debt collectors start to contact you, it can be intimidating. If you need help, continue reading to learn more about how to deal with Lowell Financial Limited and your debts.

Stop Lowell In Their Tracks. Write Off Their Debt Quickly

Stop Worrying, Remove Stress, Take Action Today

Is Lowell Financial LTD a legitimate company?

If Lowell Portfolio or Lowell Financial LTD has contacted you, you may be wondering whether they are a legitimate company. They are, in fact, a legitimate company as they are authorised and regulated by the Financial Conduct Authority (FCA). Once Lowell Financial buys your debt, they are legally allowed to contact you to try to collect it.

If you have debt from your credit card or companies such as Capital One, O2, or Littlewoods, Lowell Financial LTD will likely buy it to then cash in on your debt. So, if a debt collector from Lowell Financial reaches out to you don’t be stressed, we’ll tell you what will happen next.

Should I pay Lowell Financial?

Once Lowell Financial LTD has contacted you, they will not stop until you pay off your debt to them. They may call you, send letters, and are known to also show up to people’s houses. While this can be intimidating, it is not illegal. Fortunately, you don’t need to answer your door to any debt collector legally. Unfortunately, Lowell Financial can take legal action against you if you ignore all of their attempts to contact you.

If you do not pay your debt to Lowell Financial, they may take your case further by registering your inability to pay your debts with credit reference agencies. This can bring down your credit rating and stay on your credit file for years, making it hard to take out any loans, a new credit card, or even a mortgage in the future.

Not only that, but Lowell Financial is able to take legal action against you by taking you to court. If the county court makes a judgment in support of Lowell Financial and you still do not pay your debt, a bailiff could show up at your house to seize your assets to pay off your debts.

Lowell Financial LTD is a debt management company. This means they manage people’s debt by purchasing it at a lower rate from the company the person originally owed it to.

Ultimately, the answer is yes, you should pay Lowell Financial if you can. Here’s how!

How An IVA Could Radically Reduce Your Debts

Online Forums Are Full Of Posts From Anxious People Having To Deal With Persistent Debt Collectors:

Paying your debt with Lowell Financial back

If you have the means to pay your debt to Lowell Financial LTD back, you need to first discuss with them how you will pay it back: with one lump sum payment or by creating a payment plan. Once you decide what you can comfortably afford to pay, you can pay your debt back over the phone or online with a Lowell login and reference number.

All you need to do is log in with your reference number and set up your payment with a credit or debit card, a bank transfer or a cheque and you’re on the road to being debt-free! While this sounds like a relatively straightforward process, many people are in debt because they do not have enough money to pay off their debts in the first place. If this sounds like you and you need further debt advice to deal with Lowell Financial, keep reading!

What happens if you can’t pay your debt to Lowell Financial back?

Before you think about paying back your debts, you need to budget your money. To create a budget, write down your household income and all the money you expect to spend each month on necessities such as utilities, groceries, commute, and anything else. Then, subtract these expenses from your income. Whatever money you have left over will be the maximum amount you can put towards paying off your debts.

You can then talk to Lowell Financial LTD to create a monthly payment plan based on your budget. They will likely agree to your repayment terms, as Lowell Financial LTD only makes money if you pay off your debts. So, it is in their best interest to take what they can get if you decide not to pay any of your debts.

Similarly, if you can’t repay your debt, Lowell Financial may even offer to help you by giving you a discount on your debt if you pay it in full, or they may agree to partial repayment. Partial repayment means you pay Lowell Financial only an agreed-upon portion of your debt, and they will write off the rest. While this may be a good option if you cannot afford to pay in full, it will show on your credit history.

Your credit history will show a partial debt settlement, and while that may not be as bad as having something like bankruptcy on your file, it can still make it harder to apply for a loan, credit cards, or a mortgage.

If you create a budget and realise you still cannot pay off your debt to Lowell Financial either in full or in partial payment, here is some further debt advice.

Lower Monthly Payments & Keep The Debt Collectors From Your Door – 30-second Form

Other debt options

If you cannot afford to pay off your debt to Lowell Financial, you may be able to write it off.

This can be done by exploring other debt repayment options, such as applying for an Individual Voluntary Agreement (IVA), a Debt Relief Order, or bankruptcy.

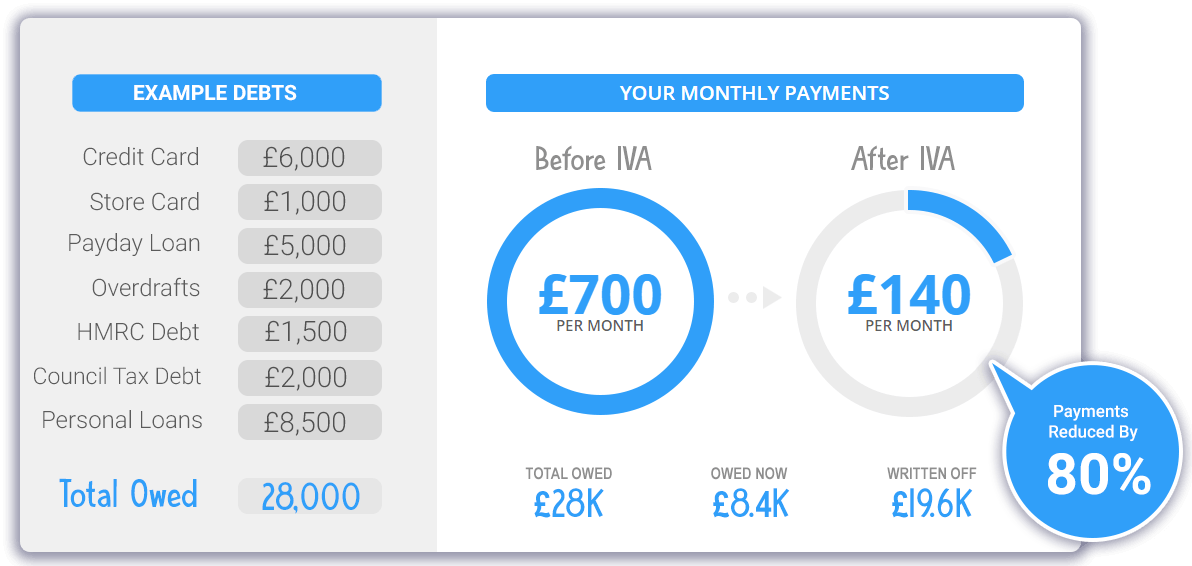

If you apply for an Individual Voluntary Agreement, the government may be able to help you write off 75% of your debt. To qualify, your debts must be over £1,700. The agreement is made with a collection agency that states you have to pay back a specified amount of your debt monthly or all at once, and the rest of it will be written off.

To qualify for a debt relief order, on the other hand, your debt has to be less than £20,000, you can’t own a house, and you have to have less than £50 leftover each month. If you agree to a debt relief order, you don’t need to make any repayments for a year, and at the end of the year, your debts will be written off.

A debt relief order does not come without its own set of problems, as it will stay in your credit file for six years. This will, in turn, make it harder to get approved for a mortgage, any credit cards, or new loans.

If any of the previous repayment options do not apply to you, your last option may be to

This can be done by exploring other debt repayment options such as applying for an Individual Voluntary Agreement (IVA), a Debt Relief Order, or bankruptcy.

If you apply for an Individual Voluntary Agreement, the government may be able to help you write off 80% of your debt. To qualify, your debts must be over £1,700. The agreement is made with a collection agency that states you have to pay back a specified amount of your debt monthly or all at once, and the rest of it will be written off.

To qualify for a debt relief order, on the other hand, your debt has to be less than £20,000, you can’t own a house, and you have to have less than £50 leftover each month. If you agree to a debt relief order, you don’t need to make any repayments for a year, and at the end of the year, your debts will be written off.

A debt relief order does not come without its problems, as it will stay in your credit file for six years. This will, in turn, make it harder to get approved for a mortgage, any credit cards, or new loans.

If none of the previous repayment options apply, your last option may be to file for bankruptcy. Filing for bankruptcy should not be taken lightly, as it can negatively affect your credit history for years, and many qualifications are necessary.

First, your debts need to be at least £5,000. Then, you have to pay a hefty application fee of £680 to an Insolvency Service. Such a high fee is meant to deter people from applying casually, but it often puts many people off as they cannot afford it.

If you can pay the application fee and are approved, all of your assets you do not need for work will be taken. Control of your bank accounts will also be taken. As there are so many conditions to filing for bankruptcy, it typically does more harm than help to do so. It should only be a last resort for those who cannot afford to pay their debt to Lowell Financial.

Filing for bankruptcy should not be taken lightly, as it can negatively affect your credit history for years, and many qualifications are necessary.

First, your debts need to be at least £5,000. Then, you have to pay a hefty application fee of £680 to an Insolvency Service. Such a high fee is meant to deter people from applying casually, but it often puts many people off as they cannot afford it.

If you can pay the application fee and are approved, all of your assets you do not need for work will be taken. Control of your bank accounts will also be taken. As there are so many conditions to filing for bankruptcy, it typically does more harm than help to do so. It should only be a last resort for those who cannot afford to pay their debt to Lowell Financial.

Can Lowell Financial take my home?

Although we discussed plenty of repayment options, you may still be unable to repay Lowell Financial.

Many people wonder if they will lose their homes in this case. Unfortunately, losing your home is a possibility.

Don’t worry too much as the possibility of losing your home is small. Losing your house is only a strong possibility if your debt is secured to it, such as with a second mortgage. Most debt is unsecured, so it is not attached to your house.

That being said, Lowell Financial may take you to the county court to secure your debt against your house. If this happens, your house could be taken, but again, it is unlikely.

Lowell Financial is breaking the law

Some people believe Lowell Financial is breaking the law because they can be quite persistent in contacting them. If you want to prevent Lowell Financial from contacting you, you can send them a cease and desist letter. This will not make your debt go away, though.

If you feel like they are doing something illegal, it is possible to report them to the government body Financial Ombudsman Service. They will then look into your complaint and proceed accordingly.

Ultimately, the best way to help yourself is to pay off your debt to Lowell Financial one way or another, so you never have to hear from them again.

Lowell Financial Ltd

- Ellington House 9 Savannah Way Valley Park West, Leeds LS10 1AB

- Main Telephone: 0333 556 5550

- Lowell Portfolio Ltd (FCA number 730071)

- Lowell Financial Ltd (FCA number 730175)

- Website: https://www.lowell.co.uk/