Thousands Of People Are Discovering Alternatives To Bankruptcy

If you are struggling with debt, you should only ever consider bankruptcy as a last resort option. Only use bankruptcy if you cannot repay your debts/creditors within a reasonable timeframe.

There are strict bankruptcy criteria. As an individual, you must owe a minimum of £5,000 and reside in England, Wales, or Northern Ireland. People living in Scotland will not be able to take the bankruptcy option but can research Sequestration or Scottish Trust Deeds instead. Bankruptcy will include all of your outstanding debt. However, it would help if you understood that you’d likely need to surrender your home and high-value possessions to pay back what is owed to your creditors.

The process usually takes twelve months, and in conclusion, all of your debts will be paid off. However, your bankruptcy status will be on the public record. If debt is causing you sleepless nights, stress and anxiety, it’s essential to research the many types of debt relief solutions before deciding on bankruptcy.

IVA Vs Bankruptcy?

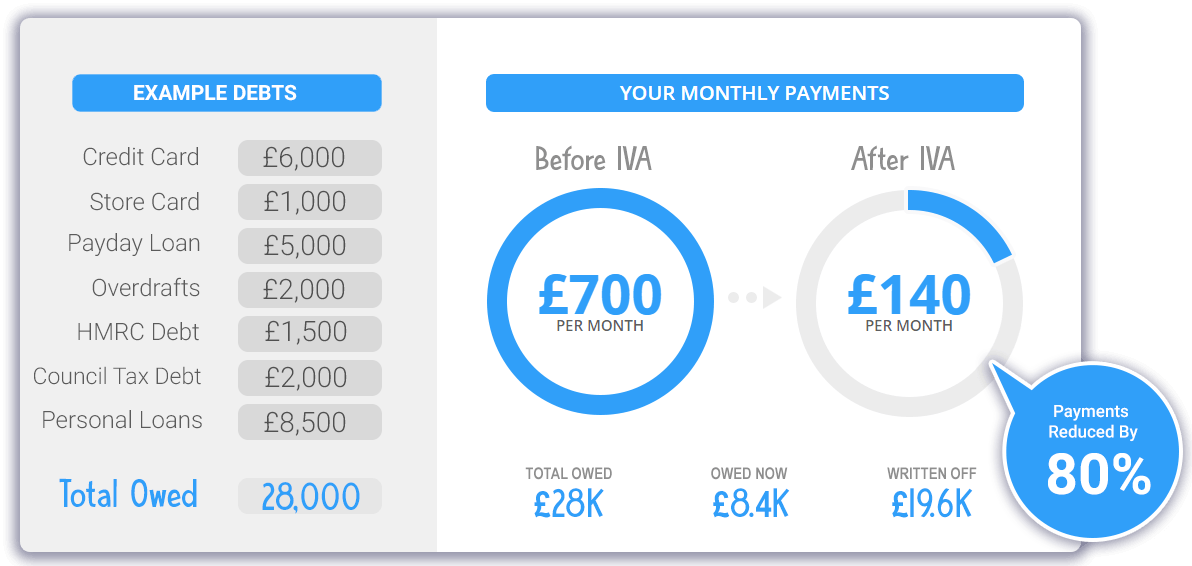

If you’re looking for a government-approved alternative to bankruptcy, you should consider an Individual Voluntary Arrangement (IVA). This effective financial solution will protect your home and other assets while enabling you to write off up to 80% of problematic debt using specialized legislation

Going Bankrupt, Thinking IVA? – Check If You Qualify

How An IVA Could Radically Reduce Your Debts

Bankruptcy is a way to deal with debts that you cannot afford to pay

It is typically viewed as a last resort, partly because it might involve using assets like the home and possessions to pay creditors.

Bankruptcy must be applied for, fees involved, and the covered individual is subject to certain restrictions. Once bankruptcy is over, the covered debts are discharged so they will not need to be repaid. This debt management solution might have a severe and lasting impact on credit, so consult us before applying for it.

Our debt experts may propose other solutions that allow you to tackle debt without as much harm to your credit score or other important areas of your life.

Bankruptcy Basics

This page applies only to bankruptcy in England and Wales. If you live in Scotland, you should read about “sequestration” instead.

Only a court can declare a person bankrupt. Individuals, sole traders, and partners can apply to be made bankrupt, but the procedures vary for a partnership or company. A creditor can petition the Court to make a person bankrupt if they owe at least £750.

Once the Court issues a bankruptcy order, the receiving party is considered bankrupt. Being made bankrupt may put you at risk of losing your business or home, depending upon your circumstances. No payments are made to covered creditors during the bankruptcy period, but you might be asked to contribute towards your debts from income, assets or windfalls.

How Bankruptcy Works

After a bankruptcy order is issued, you’ll have turned over any financial interest in the property and some valuable assets to the trustee appointed to manage the bankruptcy. This individual is either an authorized debt specialist or a Civil Servant referred to as an Official Receiver.

Appointing a trustee does not occur automatically so the Official Receiver initially fills this role and may also become the trustee depending upon your circumstances. You might be required to attend an interview to provide details regarding your assets, debts, and financial status.

If your affairs are straightforward, this meeting might be held over the telephone

The Official Receiver uses the information provided to protect assets for creditor benefit, assess whether you can afford to contribute towards your income debts, and evaluate your conduct before bankruptcy. If there is significant evidence of deliberate carelessness, dishonesty, or criminal behaviour on your part, the restrictions imposed during bankruptcy may be extended.

If you have bank accounts, these may well be frozen by the bank. Opening new accounts with a central High Street bank may not be possible while the bankruptcy order is in place. However, Barclays currently offer an account to undischarged bankrupts, and other “paid-for” accounts are available to bankrupts.

Creditors are informed of the bankruptcy and must make a formal claim to the trustee regarding the money they are due. However, they are not permitted to request payment from you directly.

The trustee may pay approved creditors by disposing of or selling your relevant assets and property (many households and other goods are excluded from this). If an Income Payments Agreement or Order is used, any spare income may help pay creditors for as long as three years. The bankruptcy period usually lasts for 12 months, but it may end earlier or be delayed due to lack of cooperation or failure to adhere to the restrictions.

Restrictions And Responsibilities During Bankruptcy

While in bankruptcy, you will be subject to certain restrictions. For example, bank accounts and credit cards must be disclosed to the Official Receiver. Payments should generally continue for all debts excluded from the bankruptcy order. Several restrictions remain in place following the bankruptcy discharge.

For example, assets which might be used to pay debts and costs are not necessarily immediately returned. If an Income Payments Agreement or Order is used, any spare income may help pay creditors for as long as three years. Bankruptcy can potentially affect some careers depending upon your profession and employment contract.

If you run a business, your trustee may require its closure and the dismissal of all employees. You must complete relevant VAT and other tax returns if the business remains open. Employees may issue a claim to the trustee for any holiday pay and wages unpaid through their National Insurance Fund claims.

Some employment contracts, including those for Financial Conduct Authority-controlled roles, charity trustees, and solicitors, might not permit a job incumbent to be bankrupt.

THOUGH YOU MAY BEGIN TRADING AGAIN, YOU MUST ADHERE TO SEVERAL RESTRICTIONS DURING BANKRUPTCY:

- Cannot act as a company director

- Court permission is required to develop, promote, or manage a company

- Must inform those you deal with of the bankruptcy if you manage a business

- Must inform a lender of the bankruptcy if you want to borrow more than £500

- Must re-register for VAT

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 60 second Form

How Bankruptcy Affects Your Home

One of the most common questions customers have for us is how bankruptcy will affect their living situation.

The truth is that you may need to sell or leave your home to help pay debts included in the bankruptcy order. This is more likely if there is considerable equity in your home or if the monthly costs are deemed to be excessive for your area or for your needs.

Control of assets, including owned property, is passed to the trustee during bankruptcy. The trustee may receive a beneficial interest in the property, which is your share of the property value after secured debts are repaid. If you are the sole owner, the trustee may also receive the property title listing the legal owner.

The transfers are recorded in the public Land Registry and remain there until the property is no longer included in the bankruptcy estate. This may be done if selling the home is the only way for the trustee to pay creditors. The mortgage and secured loans will be repaid first, and the bankruptcy estate will receive the surplus.

You cannot sell the property yourself without permission or claim any money raised during a sale by the trustee for your share of such an asset. Even if you only rent, bankruptcy might affect your housing situation if your tenancy contains a personal insolvency clause.

Positives And Negatives Of Bankruptcy

DESPITE BEING A LAST RESORT, BANKRUPTCY HAS SOME POSITIVE FEATURES:

- Typically only lasts for 12 months until discharge

- No direct payments made on covered debts while bankruptcy order is in place

- Covered debts are discharged when the bankruptcy period ends

- Can keep certain assets include household items and material and most equipment required for vocation, business, or employment (often including a vehicle)

- Pension usually not included in bankruptcy

- Self-employed individuals may begin trading again, though possibly subject to restrictions

THE NEGATIVE ASPECTS OF BANKRUPTCY INCLUDE:

- Must turn over certain assets of value, such as a financial interest in the property

- Must submit credit cards and bank accounts information to the trustee

- Does not cover all types of debt (student loans, child maintenance payments, and court fines are usually excluded)

- May have to close business in some circumstances

- It can affect the working situation for some types of employees and professionals

- It affects the ability to get credit, even after the bankruptcy has been discharged

- Listed in Individual Insolvency Register

- Bank, mortgage companies, landlord, insurance providers, and pension providers might be informed

Applying For Bankruptcy

Bankruptcy processes in Northern Ireland and Scotland are different from those in England and Wales. The steps involved in applying for bankruptcy in England and Wales are as follows:

- Complete a Debtor’s Bankruptcy Petition and Statement of Affairs, Debtor’s Position as part of the bankruptcy petition. The reason for bankruptcy must be included in the bankruptcy petition. Assets, debts, and creditor contact information must be listed on the Statement of Affairs.

- Find the bankruptcy court located nearest where you trade or work (wherever you have been located for the longest within the previous six months) which covers you geographically. Contact the Court to schedule a date and time to submit your documents and pay the fees. Provide the original and two copies of the forms to the Court. Keep a copy of each form for your records.

- Pay bankruptcy fees of £175 for court costs and £525 for bankruptcy management costs (at the time of writing). If you receive income support, the court fee may not apply. Check with the Court in advance what types of payment will be acceptable.

- The Court will review the bankruptcy petition and decide whether it needs further information, whether it should reject the petition, reject it and order a bankruptcy alternative, or, most commonly, issue the bankruptcy order that you have applied for. If the petition is denied, you will not be refunded the fees, but if an alternative is recommended, these fees may be used to any charges that apply.

Bankruptcy In A Nutshell

- You must apply through a bankruptcy court which covers the area in which you are based.

- £700 fee

- No payment of covered debts during the bankruptcy period

- Can lose home, business, and assets in some circumstances

- It may affect employment for some

- Your existing bank accounts are usually frozen

- Published on Personal Insolvency Register

- Debts are typically discharged after 12 months if not repaid through asset and property sales

- Credit reporting agencies maintain bankruptcy records for six years

You may be considering bankruptcy if you cannot repay your existing debts. We recommend that you contact us first so we can review your financial situation and determine whether there are alternatives. Debt management is complex, but Jubilee Debt Management experts understand the nuances. We will consider your level and type of debt and provide you with debt management options in a no-pressure way that allows you to remain in control of the situation.

Alternatives to Bankruptcies UK and Bankruptcy Pros and Cons UK

When facing financial difficulties, it’s important to explore all available options before considering bankruptcy. This guide delves into various alternatives to bankruptcy in the UK, discussing their pros and cons. Additionally, it provides an overview of different loan options, including interest rates, loan to value (LTV) ratios, and reviews.

Understanding Bankruptcy in the UK

Bankruptcy is a legal status for individuals or businesses that cannot repay their outstanding debts. While it can provide a fresh start, it also comes with significant drawbacks. It’s crucial to weigh the pros and cons before making a decision.

Pros of Bankruptcy

- Debt Relief: Bankruptcy can discharge most debts, giving you a fresh financial start.

- Legal Protection: Creditors must stop collection efforts once bankruptcy is filed.

- Asset Protection: Some assets may be exempt from liquidation under bankruptcy laws.

Cons of Bankruptcy

- Credit Impact: Bankruptcy severely impacts your credit score, making future borrowing difficult.

- Asset Loss: Non-exempt assets may be sold to repay creditors.

- Public Record: Bankruptcy filings are public records, which can affect your reputation.

Alternatives to Bankruptcy

Before opting for bankruptcy, consider these alternatives which might help you manage your debt more effectively without the long-term consequences of bankruptcy.

Debt Consolidation

Debt consolidation involves combining multiple debts into a single loan with a lower interest rate. This can simplify repayment and reduce overall interest costs. Use a loan calculator consolidation to understand your potential savings.

Debt Consolidation Loan

Consolidating debts into one loan can make it easier to manage repayments. Explore options for a debt consolidation loan rates to see if this solution suits your needs.

Credit Card Debt Consolidation Loan

Using a consolidated credit cards loan to pay off high-interest credit card debt can significantly reduce the amount of interest you pay and simplify your financial management.

Secured Loans

Secured loans use your property as collateral, providing better terms and lower interest rates than unsecured loans. Even with poor credit, you can explore can i get a secured loan with bad credit options.

Loan Options and Reviews

Various loan options are available for those seeking alternatives to bankruptcy. Below is a table comparing interest rates, LTV ratios, and reviews for different loan products.

| Loan Product | Interest Rate | LTV Ratio | Reviews |

|---|---|---|---|

| Secured Loan (Good Credit) | 3.5% | 80% | ★★★★☆ |

| Secured Loan (Poor Credit) | 6.5% | 70% | ★★★☆☆ |

| Debt Consolidation Loan | 5.0% | 75% | ★★★★☆ |

£25,000 Loans

For significant financial needs, a 25000 loan over 5 years can provide the necessary funds to cover substantial expenses or consolidate multiple debts.

Loans for £50,000

For larger sums, a loans for 50000 offers substantial capital that can be used for various purposes, including debt consolidation and major purchases.

Broker Loans

Utilising a homeowner loans broker can help you find the best secured loan products available. Brokers have access to a range of lenders and can provide tailored recommendations.

Secured Loan Instant Decision

For urgent financial needs, bad credit secured loans instant decision provide quick access to funds. Although these loans may have higher interest rates, they offer the convenience of immediate approval.

Homeowner Loans Bad Credit Direct Lender

Working directly with lenders can sometimes yield better terms. bad credit secured loans direct lender options are available for those with poor credit histories.

Secured Loans for Bad Credit

Even with a less-than-perfect credit score, homeowners can explore secured loan for bad credit uk. These loans use home equity as collateral, providing better terms than unsecured loans.

Debt Consolidation Loan Calculator

Using a loan calculator consolidation helps homeowners understand their repayment options and potential savings. This tool provides a clear picture of how consolidating debt can simplify financial management.

Debt Consolidation Loans

Secured loans are a popular choice for debt consolidation. By consolidating debts into one loan, homeowners can streamline their finances and potentially lower their monthly payments. Explore debt consolidation loan rates for more information.

Best Consolidated Debt Loans

Finding the best consolidation loans uk requires research and comparison. Look for loans with favourable terms and rates that suit your financial needs.

Kent Reliance Debt Consolidation for Poor Credit

For those with poor credit, nationwide debt consolidation can provide tailored solutions to manage debt more effectively. Kent Reliance offers competitive rates for those with less-than-perfect credit histories.

Mortgages for Poor Credit UK

For those with poor credit, securing a mortgage can be challenging. However, options are available with mortgage interest rates for bad credit. Working with specialists can help find suitable products even with a less-than-perfect credit score.

Pros and Cons of Alternatives to Bankruptcy in the UK

When considering alternatives to bankruptcy, it’s essential to understand both the benefits and potential drawbacks. Debt consolidation loans, secured loans, and remortgaging offer viable solutions, but each comes with its own set of considerations.

- Debt consolidation can simplify your financial management but might extend your repayment period.

- Secured loans offer better terms but put your property at risk if you default.

- Remortgaging can release equity but may come with higher interest rates for those with poor credit.

By carefully evaluating these options and seeking professional advice, you can find a solution that best fits your financial situation and long-term goals. It’s important to stay informed and proactive in managing your finances to avoid the severe consequences of bankruptcy.