Do you live in Scotland and have debts such as credit cards, store cards and personal loans that are spiraling out of control?

Combine All Of Your Unsecured Debts Into One Low Affordable Payment

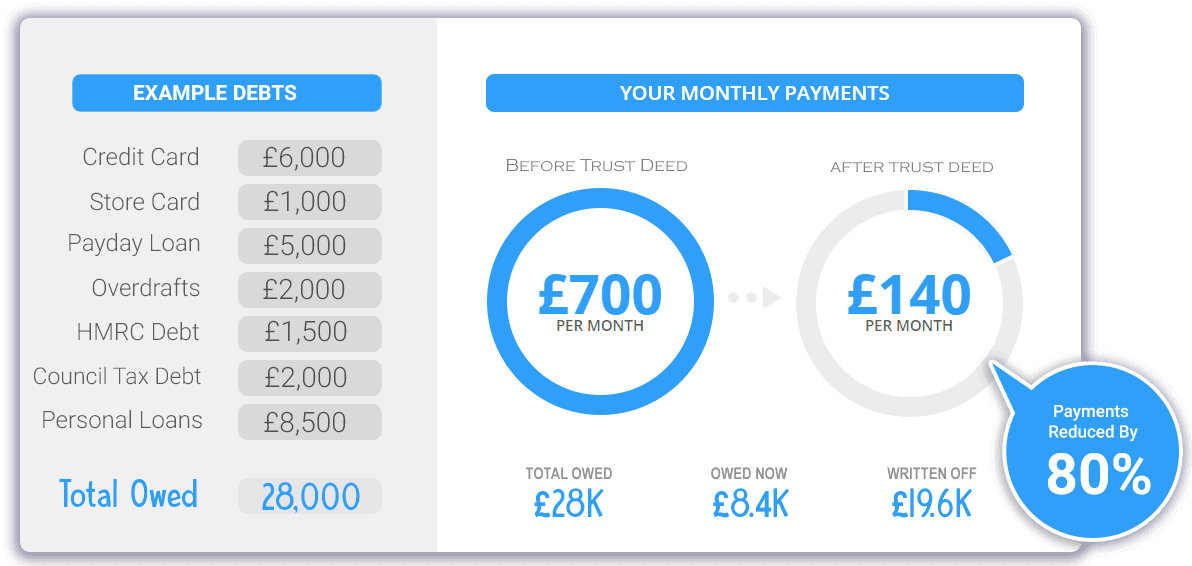

Find Out If Scottish Trust Deeds Are The Right Solution For You

Basic Trust Deed Scotland Criteria:

- You must be a Scottish resident or have left Scotland only recently

- You must be unable to continue fully repaying your debts

- Minimum debt level £5,000

- Unsecured debts, typically credit cards, Loans, Store Cards, Bank Overdrafts, (excluding student loans) Council Tax Arrears can be included.

- The minimum monthly repayment contribution is often set as low as £80.

Graphical Representation Of A Typical Scottish Trust Deed

TYPES OF DEBT JUBILEE CAN ASSIST YOU WITH:

We provide you with an effective solution to the burden of unsecured debts which include the following:

Credit Cards

Personal Loans

Overdrafts

Store Cards

Council Tax Arrears

Unsecured Car Loans

Payday Loans

Catalogues

Scottish Trust Deeds were introduced in 1985 by the Government as an alternative to sequestration (bankruptcy)

They are formal voluntary arrangements, using the Bankruptcy (Scotland) Act 1985.

The Trust Deed can only be administered by a licensed Insolvency Practitioner (IP) who will act as a Trustee and communicate/negotiate with your creditors acting on your behalf. You will pay an agreed amount over typically 48 months and after this time period ends (and you have completed all obligations) you will be ‘discharged’ and your outstanding included debts will be written off.

Once the proposal is drafted, the experience and knowledge of the insolvency practitioner should ensure that the acceptance criteria of the major banks are complied with. If the creditors still do not accept the proposal, then the trustee may still be able to negotiate your case to get it accepted.

FAQ’s

Will I Lose My Home?

Your recommended provider will establish whether or not you have any too much equity in your home as a part of their initial assessment. If you do have equity, then you will be asked whether it will be feasible for you to raise this sum, perhaps with the assistance of a relative or via an extension to the trust deed term.

There are alternative solutions such as Debt Arrangement Schemes which may be more suitable should you have too much equity to make the Trust Deed viable. Your Trustee will establish this prior to signing.

How can I afford to live under a Trust Deed?

A Trust Deed is not constructed in a way to make your life financially unviable and not be able to live on a day to day basis. On the contrary, it is a structured debt management plan to allow you to pay what you can afford, leading to consistent monthly payments and leaving you with enough money to pay your household and utility bills and living costs and expenses.

For creditors, reliability, through affordable monthly payments is essential, and this can only happen if the payment terms are fair. Repayments are calculated using a calculator called a Common Financial Tool, which is part of Trust Deed legislation to ensure that contributions are affordable.

Will my details be published in my local newspapers?

No, your Trustee will only put details of your Trust Deed in the Register of insolvencies.

What is the difference between a Trust Deed and an IVA?

A Scottish Trust Deed is available only to Scottish residents, whereas an IVA is available only to English and Welsh residents. Under a Trust Deed in Scotland, the minimum amount of unsecured debts to qualify is £5,000. An IVA has a higher threshold with a minimum of £10,000 of unsecured debt. The length of the arrangement also differs with a Trust Deed duration being 48 months against the 60 months for an IVA.

Who can set it up?

Only a licensed Insolvency Practitioner can set up and administer them.

Does it matter which Trust Deed Scotland company I use?

Some insolvency companies do not readily offer home visits which we consider to be very important. It’s clear that customer feedback on the various firms in the market varies widely.

Is a Trust Deed a loan?

No, it is a voluntary action which allows you to come to an agreement with your creditors to repay only what you can afford. No credit checks are required and your offer of repayment is based on what is realistic and reasonable for you to repay.

Because you’re expected to pay what you can reasonably afford your expenditure will be restricted during the term of a trust deed in Scotland.

Scottish Trust Deeds and my credit rating

Entering a Trust Deed could have negative consequences on your rating with credit reference agencies. Prospective lenders are likely to see you as a higher risk of defaulting on a loan than someone with an excellent credit reference.

A Trust Deed does show to lenders however, that you have recognised your financial circumstances and are doing something about it. Due to this, even with a Trust agreement, lenders may be willing to provide you with credit.

The duration of a Trust Deed is four years, and during this time, your credit rating is adversely affected. Even when you discharge from the Deed, it will take time to build back up to a good credit score.

Will I be credit checked before acceptance?

Not usually. Since you will not be borrowing any money, there will generally be no need for a credit search.

Can I Enter A Trust Deed If I Already Have Court Action Against Me?

Yes. Entering into a Trust Deed is not prohibited if you have court action against you. If you are facing court action we strongly recommend taking advice as soon as possible. Your choices may become restricted after legal action has progressed.

If I am a homeowner, will I have to release equity in my home?

Depending on the equity you have in your home you may have to release equity in your home into the Trust Deed, usually as part of the final settlement. It’s therefore important for homeowners with equity to have a carefully established plan to deal with the equity when the time comes.

Does it make a difference if I am a homeowner?

No. It makes no difference whether you are a private tenant, homeowner, council tenant or if you are still living with your parents.

Do I have to tell my partner?

It is a private arrangement between you and your creditors. It is advisable, where possible to share this with your partner for your own peace of mind. You may need to check that you have no joint debts or that someone has acted as a guarantor on your behalf. If you have any joint financial arrangements your partner may be made aware. Trust deeds are recorded on public registers.

Can I lose my job?

Unless stipulated in the terms of your employment contract, it is not a requirement to advise your employer that you have entered a Trust Deed. If you do not tell your employer, they will only find out if via name on the Register of Insolvencies in Scotland. However, in some sectors such as the Financial and Legal industry, entering a Trust Deed and not telling your employer may have negative consequences. It is always best to check your employment contract or speak with an HR representative at your employer.

Does it cover all of my debts?

No, not this type of debt solution. They can only cover your unsecured debts and some types of arrears. This is usually things like credit cards, bank overdrafts, store cards and personal loans. It will not cover most student loans. Debts that aren’t covered will remain your liability to repay.

What will happen to joint debts?

If you happen to share the debt with another person, it is known as joint and several liabilities. By taking out a Trust Deed, the other person can also be liable for the entire debt. The joint debt lists on the Deed, but the Trustee will choose not to make payments to repay the debt. If a couple is cohabiting, they may want to have their own separate Trust Deed.

What is the difference between a secured and unsecured debt?

A secured debt is a debt secured against an asset that you own. Typically secured debts will be a mortgage, a secured loan, car HP etc. An unsecured loan is any loan not secured on an asset such as a bank overdraft, a personal loan, a credit card, store card etc.

Do Creditors Have To Accept A Trust Deed?

No. Your creditors do not have to accept, but it will only fail if creditors representing either over 33% in total debt value or over one half in number; object in writing within five weeks of your trust deed being proposed.

A large number of UK creditors have their insolvency debts handled by specialist agencies that are regulated by the financial conduct authority and your Trustee will normally only propose your Trust Deed in line with current guidance.

In the event that your trust deed did fail, you will always be advised on what to do next and also on other Scottish debt solutions such as the Debt Arrangement Scheme or sequestration.

Will the Trust Deed prevent my creditors from taking further recovery action?

Yes. Once a Trust Deed has become protected (PTD), you are protected from all further recovery action by your unsecured creditors provided that you keep up the terms of the repayment.

How long will A Protected Trust Deed In Scotland it last for?

This can vary, but it usually lasts for 4 years. It may be extended if you are a homeowner with equity or if during the agreement, for example, you fell pregnant and were unable to keep up repayment whilst on maternity leave – your trustee could extend the length of your agreement to reflect any period of reduced payment.

What happens if I cannot keep up my payments?

Scottish Trust Deeds are legally binding agreements agreed in a court of law and not keeping up with monthly payments without a valid reason can have serious consequences. If you are struggling to adhere to the terms, it is vital to get debt advice from the Trustee who may be able to find a solution whilst keeping the terms of the Trust Deed in place.

How Are The Trustee Fees Collected?

The fees that the Trustee charges are collected from the payments you make into the nominated account and you will normally have no other fees to pay.

How long will it take Trustees to set up a Trust Deed?

A Trust Deed document and the accompanying paperwork can be set up very quickly by appointed Trustees who are Insolvency Practitioners. The Trustee will handle all the creditors on your behalf, including negotiating the debt repayment terms, dealing with all correspondence from creditors and making payments on your behalf under the terms of Trust Deed.

Will interest and charges be frozen while being set up?

No, but any such interest and charges will be included in the Trust Deed if it is approved and becomes protected.

What happens if the Trust Deed is not approved?

You will have to come to an informal arrangement with your creditors to repay your debts or consider sequestration.

What are Protected Trust Deeds?

A Trust Deed can only become protected if your creditors agree to this as part of the payment proposal terms received from your Trustee. Under a proposal, creditors have five weeks in which to agree to the payment terms. As long as the majority agree, then all the creditors will need to accept the terms.

Once a Trust Deed becomes protected, it means that it is legally binding as it is an official document agreed in a court of law in Scotland. Creditors can no longer pursue you for further payment, add additional charges or penalties to your debt or force you into bankruptcy.

What Happens If A Trust Deed Cannot become Protected?

If creditors do not agree to give protected status to your Trust Deed, it does not mean that an arrangement cannot be put in place. However, an unprotected Scottish Trust Deed allows creditors to change the terms of the agreement by demanding higher monthly payments than you are currently paying or force you to file for bankruptcy.

What am I committing myself to if I sign?

You are entering into a debt solution contract to repay your debts, usually at a reduced rate. As such you agree to:

- Co-operate with the Trustee

- Pay the agreed monthly contribution

- Advise the Trustee if your circumstances change

- Advise the Trustee if receive any unexpected windfalls

What If My Creditors Do Not Accept The Proposal?

Remember not all creditors need to agree to the repayment proposal and should the creditors to the value of 67% of the total unsecured debts agree to the proposal (or more than half in number), the others are still legally bound by its terms regardless.

Are There Other Debt Solutions Available?

Other options are available to you if a Trust Deed does not apply to your circumstances.

Debt Consolidation

Debt consolidation is also known as re-financing. Debt consolidation loans work by amalgamating all your separate unsecured debt into one single monthly payment. Offered by a debt management provider, they work by reducing your monthly debt repayments by extending the loan period or providing finance through a lower rate of interest.

Voluntary Agreements

A voluntary agreement is a simple debt plan agreed directly with your creditors. Unlike a Trust Deed, you deal directly with the creditors while remaining in control of your finances. A voluntary agreement is not legally binding, and your creditors can take further legal action if you are unable to keep up with the terms of the debt agreement. Sometimes, an aggressive creditor decides the current conditions become unacceptable for them.

Bankruptcy

Bankruptcy is the last form of action available to those with unmanageable debt as control of your finances passes over to the Official Receiver. Also known as sequestration in Scotland, bankruptcy is available to those with debts of £3,000 and above. A Form of light bankruptcy called MAP – Minimal Assets Process is also possible to those with debts of £1,500 or more and who have no assets or income.

Debt Arrangement Scheme (DAS)

DAS is a scheme that was set up by the Scottish Government to help you pay back debts without the threat of court action by creditors. Under DAS, you set up a debt payment programme and make a regular monthly payment which is sent on to creditors. DAS is an option if you have enough money to make regular payments, do not want to sell your home and your job may be at risk if you take a debt solution that sees your name put on the Insolvency Register.

Trust Deed Scotland Pros And Cons:

Pros

- Creditor contact: You will no longer receive communication by people that you owe money. Under a Trust Deed, the Trustee will handle the relationship between you and your creditors.

- Bank account: Under a Trust Deed, you will still be able to retain and maintain control over your bank account, which is not possible under other types of debt control such as bankruptcy.

- Ability to pay bills: Under a Trust Deed, you do not have to show that you cannot pay your outgoings as they become due. It is also known as apparent insolvency which you have to explain to apply for sequestration (bankruptcy) in Scotland.

- Employment: Under a Trust Deed, unlike bankruptcy, you are not banned from certain types of work or holding a position in public office.

- Borrowing money: Under a Trust Deed, you are not stopped from being able to borrow money, whether this is a credit card, personal loan, or a mortgage. In reality, it may be hard to get credit approval if you have entered into a Trust Deed.

- Debts wipe out: If you adhere to the payment schedule of a Trust Deed and make all your monthly payments, after 48 months, you are discharged from the agreement with a pre-agreed portion of your debts being paid and the remainder wiping out.

- Enforcement action ceases: By applying for a Trust Deed, it stops your creditors taking legal steps to get back the loan amount that you owe to them. For six weeks, under a moratorium, your creditors can no longer request enforcement such as control of your bank account. Applying for bankruptcy or a Debt Arrangement Scheme are also debt control measures that allow you to put a moratorium in place.

- Keep your home: Under a Trust Deed, if you are a homeowner, you will typically get to keep you home. If you do have lots of equity in your property, you may have to remortgage your home or extend the length of the Trust Deed.

- No further charges: Under a Trust deed, as it is legally binding, your creditors will no longer be able to add additional interest and charges or late payment fees on to your outstanding debt.

Cons

- You have to make regular payments: As part of the debt plan, you have committed to paying a regular monthly contribution over a significant period which for a Trust Deed is 48 months (4 years).

- You cannot become a company director: If you have signed up to the terms of a Trust Deed, you can no longer be a company director of an existing or new company unless the terms of the Deed permit it.

- Not all debts have inclusion: As we have mentioned previously in this guide, not all financial debt can get inclusion in a Trust Deed. Secured borrowing such as a mortgage, hire purchase agreement or a car loan remain outside the remit of the trust plan.

- You may not get protected Trust Deed status: As part of a proposal put forward by your Trustee, creditors may not accept protected Trust Deed status as they are unable to take further legal action throughout the agreement.

- Still, be made bankrupt: If you do not adhere to the terms during the Trust Deed, such as maintaining payments, the Trustee can start bankruptcy proceedings against you.

- Public record: Once you enter a Trust Deed, an entry takes place on the Register of Insolvencies which then becomes a matter of public record meaning the removal of anonymity.

- Credit rating: Setting up a Trust Deed will see your credit rating adversely affected six years from the date that the agreement starts. A poor credit score on your credit file will seriously affect your ability to get future loans or mortgages.

- Selling your assets: Often you will get to keep your home under a Trust Deed; there can however be circumstances if there is equity in the property when creditors will enforce the sale or remortgaging of your home to release funds.

- Full co-operation: The job of a Trustee is to ensure a Trust Deed, which is a legally binding document is adhered. If you do not adhere to the terms, the Trustee may apply to make you bankrupt.

- Self-employment: If you are self-employed, a trustee may choose to get somebody else to run your business rather than letting you run it yourself. In some cases, the Trustee may also recommend that you sell your business if it can release value to pay back creditors.

- Cash windfalls or new assets: If you receive a cash lump sum, such as the proceeds of an inheritance or assets within four years of the start of the Deed, the Trustee can claim these and use them to pay back your creditors.