Do you want to repay your unsecured debts but pay an affordable amount each month?

A debt management plan may be an appropriate solution. Where appropriate, it reduces monthly payments for unsecured debts so living expenses become more manageable.

This allows you to regain control over your debts, making repayment more affordable so life can get back on track. Rather than dreaming about becoming debt-free, consider using a debt management plan to make this a realistic future prospect.

Positives and Negatives Of A DMP

This plan offers several advantages:

- Reduced monthly payments

- A single monthly payment makes it easier to stay on track with debt repayment

- Creditors may freeze interest and other charges

- Flexible enough to change based on your financial status

- Covered unsecured debts are cleared once the plan fully concludes

However, it also features several drawbacks:

- Not everyone qualifies

- Debts aren’t generally written off, they must be repaid in full

- Creditors are not obligated to participate or freeze interest or other charges

- Secured debts including the mortgage are not covered

- It may lead to an increase in the overall amount repayable

- When you cease making payments to your creditors directly your accounts may go into arrears or further into arrears

- Your budget will be somewhat restricted during the DMP to allow for a reasonable payment to be made to your creditors

- Credit rating is affected because reduced monthly payments are recorded on credit history

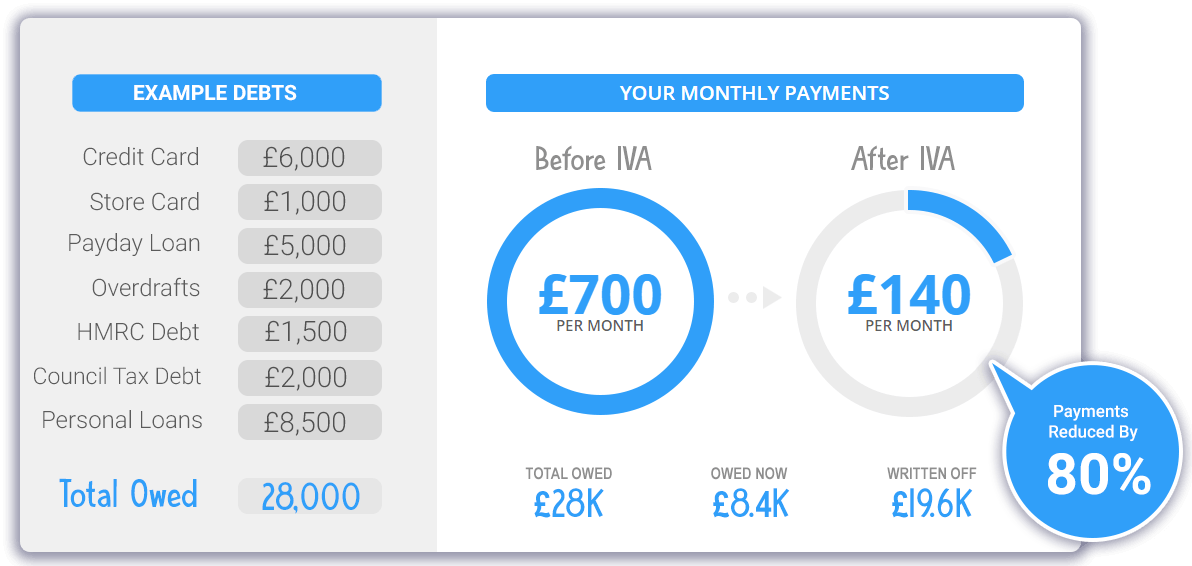

Discover How To Write Off 80% Or More Of Your Debt

Representation Of An Alternative But Effective Debt Solution

Debt Management Plan Basics

When financial difficulties prevent you from maintaining contractual payments to creditors of unsecured debt, a debt management plan makes dealing with your creditors easier. Though you can arrange a debt management plan on your own, having a third party do it might save time and frustration.

The provider works to negotiate lower monthly repayments with each of your unsecured creditors. A good provider also uses their expertise and established relationships with those creditors to encourage them to consider suspending interest and other charges.

The process begins with one of our representative reviewing your financial situation. By creating a budget and determining how much income remains each month, we help you determine whether a debt management plan is the best solution to your financial issues. This also makes it easier for you to control your spending. Our advice is professional and there is never any obligation to take it. We simply provide recommendations—whether you use them is up to you.

WHY CHOOSE A DEBT MANAGEMENT PLAN?

If it has become difficult for you to manage your debts, avoid the urge to do nothing. Ignoring the situation will not make the problem go away. It will actually make it worse, especially if you begin to miss payments. Rather than allowing creditors to pressure you into paying more than you can afford, explore a debt management plan. Reducing payments to a feasible level helps rectify the financial situation rather than worsening it.

A debt management plan should make debt repayment affordable. With a third party arranging the reduced payment, you are spared the trouble. All debts will be combined into one monthly payment, making financial management easier. Taking the appropriate action to repay debts reduces the risk of becoming subject to legal action from creditors. This might help you to avoid additional damage to the credit rating, not to mention the stigma associated with these processes.

ESTABLISHING A DEBT MANAGEMENT PLAN

If you owe unaffordable amounts in unsecured debts like credit cards, personal loans, store cards, and bank overdrafts, you may qualify for a debt management plan. This plan is an agreement between a debtor and creditors for a revised monthly payment.

This payment is based on how much you can afford to pay after accounting for essential living expenses like food and shelter. When you establish a debt management plan, you make a new type of commitment to repay unsecured debts in full. Creditors are asked to freeze interest and other charges during the setup process and many creditors are known to agree to this, making debt repayment more affordable.

Professional DMP providers, arranging debt management plans for their customers, serve as an intermediary, handling negotiations and payments directly with creditors. This plan is voluntary and can only be used to repay debts that are not secured against property or other assets. Once a creditor agrees to the plan, it should not generally contact you other than to provide you with statements and other vital account information.

How A Debt Management Plan Works

If your unsecured creditors agree to participate in a debt management plan, you will know your revised monthly payment for each debt. You submit one monthly payment that equals the monthly instalment due to each creditor plus any agreed fee. The debt management provider then allocates the appropriate amount to each creditor. You have only one payment to submit each month, making debt repayment more convenient for you.

As monthly payments continue, debt balances will typically begin falling. Though you have committed to repay debts in full, you are doing it over a longer period of time, with the aim of making the process more affordable. When the plan concludes, each covered debt will have been repaid in full, leaving you debt-free provided that you have not borrowed more elsewhere.

By adhering to the budget established at the beginning of the process, many people are able to become debt-free and start saving for the future.

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 60 second Form

Features Of A Good Debt Management Company

Put some thought into selecting a company to administer a debt management plan. Using an inexperienced organisation can create more financial headaches. When selecting a provider or operator for a debt management plan look for a company that:

- 1Is authorised and regulated by the Financial Conduct Authority (FCA)

- 2Discusses all available debt management options

- 3Provides objective advice and does not pressure you to choose a solution

- 4Clearly details any costs before the plan is finalized

- 5Explains ramifications of late or missed payments

- 6Explains plan terms and conditions before the plan begins, including the amount of monthly payment and length of the repayment term

- 7Details reasons that it could stop administering the plan

Each of the factors above describes our approach to doing business. In addition to telling you when a debt management plan might be the best solution, we will tell you when it is not. This plan is not recommended if the following statements apply:

- All debts are secured by the home or another asset

- The existing repayment amounts for unsecured debts are affordable

- Amount of available income is too small to establish a reasonable repayment time or permit regular repayments

If we determine that a debt management plan is not the best solution, we will provide alternatives. You can also refer to the guides on our website to explore these offerings. Rest assured that the answer to your debt issues is within reach. After learning more about your financial situation, one of our debt management experts will quickly make recommendations.

THE DEBT MANAGEMENT PLAN IN A NUTSHELL:

- A debt management plan is designed for UK residents who are unable to afford the established monthly payments for unsecured debts.

- The plan does not reduce or write off debts but enables making reduced payments each month until covered debts are repaid in full.

- This plan is an informal solution so it is not legally binding. Creditors are not obligated to agree to it and you may cancel it at any time.

- You make a single monthly payment to your DMP provider and they allocate the appropriate amount to each creditor included in the plan.

- Covered creditors that agree to the plan typically cease further collection actions.

- It may take longer to pay off debts because monthly payments are reduced. If the debt management company takes a portion of payments for its services, the repayment period is further extended.

Think about your financial situation and decide whether a debt management plan is the best solution. If you are unsure, contact us for guidance. If this plan is the best solution, we take the lead in working out your framework. We’ll put you in touch with our debt management partners who will subsequently interact with your creditors.

If your financial situation improves or worsens, they will help adjust the debt management plan accordingly or recommend alternative solutions. Our experts work hard to make debt management as painless as possible. They make no judgments, only offer advice and solutions.

While the plan is in effect, they stay in contact to provide updates and answer questions that may arise. At all times, you’re in a position to know exactly where you stand financially with each covered creditor, providing peace of mind until debts are repaid.

The best time to take control of debt is before it becomes unmanageable. A debt management plan is one way to handle debts that have become unaffordable before things reach a crisis stage. Taking action today can prevent many headaches in the future. Creditors may stop their relentless efforts to obtain payment and you will be on the road to becoming debt-free in the future.