Are you a single mum and struggling with your finances to the point that they are now out of control?

Do you worry about how you will be able to continue providing a stable home environment for your children?

You are like many UK single mums experiencing similar issues, and there are financial solutions to your problems. Carry on reading to find out further about the challenges facing single mothers and financial solutions such as IVAs.

Your 60 Second Debt IVA Calculator Test. Do You Qualify?

What Financial Challenges Do Single Mums Face?

As a single mum, maintaining a strict budget to run a household with children is essential. With potentially only one source of income if no spousal maintenance is available or just relying on government benefit will result in a challenging financial environment.

Throw into the equation unexpected costs and the pressure to provide enough food and adequately clothe your children can present substantial economic challenges that if you do not have discipline will soon spiral out of control.

Why do Single Mothers have Financial Problems?

Spending behaviour is the number one cause of financial problems for single mothers. With no plan in place to manage the monthly budget, money can evaporate unnecessarily.

A monthly budget includes setting aside money for:

- Groceries

- Household bills

- Unexpected costs such as replacing household appliances

- Children’s clothes, shoes, and school uniforms

- Existing unsecured loans

- Travel costs

For mothers that do not adhere to a monthly budget, finances can quickly become unmanageable. If the case, it is vital to get to the root of your spending problem by analysing your spending habits.

It is essential to differentiate between what are necessary purchases and what constitutes a luxury purchase. You can do this by tracking every single time you spend money either manually or using a spending app available on either Google Play or the App Store. After a month, it will give you a clear indication of where your money goes.

If you have left it too late and your debt repayments are already uncontrollable, it may be the time to think about a debt management solution to address the issue.

How An IVA Could Radically Reduce Your Debts

What is an IVA, and how does it work?

An IVA is a formal arrangement agreed in a court of law to pay back a pre-agreed amount of debt to your creditors over a fixed period.

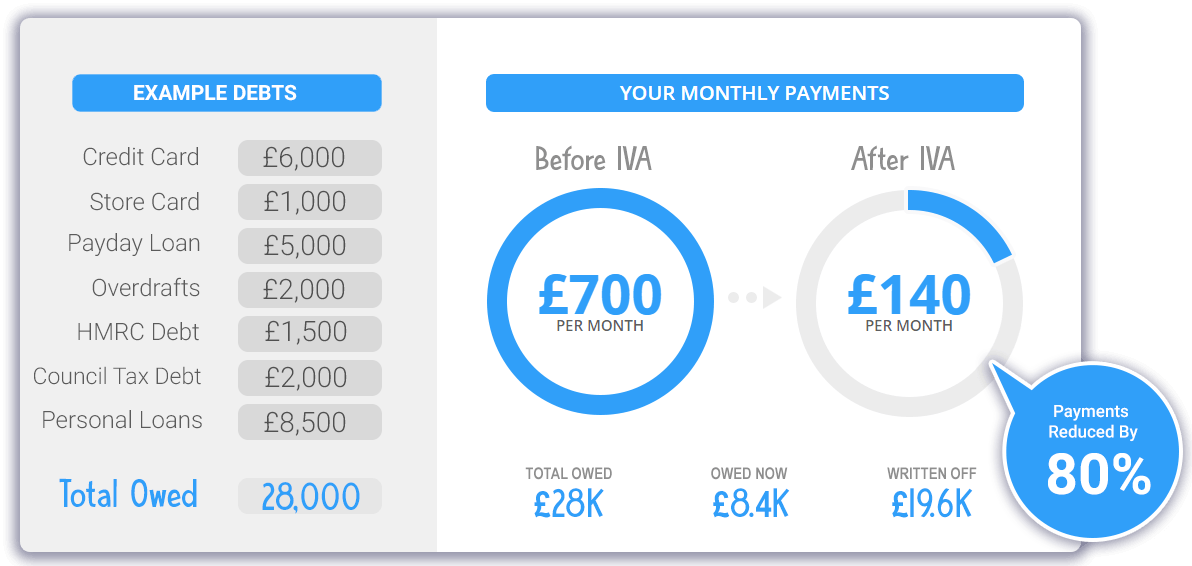

The services of an Insolvency Practitioner are mandatory to put an IVA in place who will put together a Statement of Affairs which includes monthly income, assets, and liabilities. A proposal is then put forward to creditors to offer to pay back a reduced amount of debt which can see as much as 80% of the outstanding amount written off.

As A Single Mum Is An IVA Appropriate For Your Situation?

An Individual Voluntary Arrangement may not be relevant for your situation, and either a free debt service such as CAB or the National Debt Service, or an insolvency practitioner will be able to provide guidance.

Generally, there are four essential criteria to meet to qualify for an IVA:

- After you have paid all your bills and living expenses, an Insolvency Practitioner will insist that there must be at least £50 of surplus income available to make a monthly IVA payment.

- You need to have outstanding debt to at least two different lenders to put in place an Individual Voluntary Arrangement.

- An IVA can set up with debts as little as £7,000. Due to the fees associated with an IVA, however, to make it a cost-effective solution it is not recommended to set up an IVA for less than £10,000

- An IVA is a solution if you are unable to pay back your unsecured debt in a time frame that is not deemed acceptable.

Lower Monthly Payments & Write Off Up To 80% Of Your Debt – 60 second Form

Are There Any Other Options Available?

An IVA may not be appropriate for your circumstances, and there are other debt solutions available. Again, before agreeing on any financial management plan, it is vital to seek guidance. Debt advice is available from services such as Citizens Advice and the National Debt Service.

Debt consolidation

Is taking all your outstanding loan payments and amalgamating them into one single payment. The aim is to reduce your regular payments through either a lower interest rate or extending the duration of borrowing.

A Debt Management Plan

Is the negotiation of your debts with your creditors by a debt management provider who will attempt to negotiate the debt into one lower monthly payment. A DMP has similarities to an IVA but is an informal agreement and not approved by a court of law. It means that creditors can still take further legal action.

Bankruptcy

Is often considered the final option to take if your debts are out of control and is a declaration of being unable to service your debts. It is quicker to put in place than an IVA but can also mean you lose your home and other assets as your finances pass over to an official receiver.

A Debt Relief Order

or DRO shares standard features with bankruptcy but is for those who have no assets, very little supplementary income and less than £15,000 of outstanding debt. A DRO provides a payment break towards any debt for a year as an initial attempt to see if your circumstances improve, beyond which, any outstanding debt writes off.

What Is The Duration Of An IVA?

- An IVA is structured to last for five years (60 months). It can end earlier if you can provide a lump sum payment to your creditors, in the case that you receive a financial windfall. Conversely in certain instances, it can be extended for a further 12 months to permit you to make the payments set out in the IVA.

How Much Debt Can You Write Off With An IVA?

Your Insolvency Practitioner will know how much they can expect your creditors to accept when they present a financial proposal to pay back your debts. Reduced monthly payments in an IVA can be as low as 25% of the outstanding debt and as high as 80%. The IVA will typically include unsecured rather than secured debt. It includes personal loans, credit cards, bank overdrafts, utility bill arrears and doorstep or payday loans. Secured loans such as a mortgage and other debt like student loans will need paying outside of the IVA framework.

What Are the Consequences of an IVA?

Suppose your creditors successfully accept your proposal for an IVA. In that case, it is still not all plain sailing, and there are consequences associated with having a plan in place which include:

- You cannot apply for new finance above £500 during the IVA.

- The Insolvency Service will record your IVA on the IIR (Individual Insolvency Register) which can be accessed by the general public and contains personal details of those with an IVA against their name.

- Your job may be at risk if you enter into an IVA and to make sure it does not happen, it is vital to check your employment contract before any application.

- If you miss any payments, the Individual Voluntary Arrangement extends to make up the shortfall.

- From the date that the IVA commences is the date that your credit rating is affected. It will remain on your credit file and impact your credit score for six years.

- For the IVAs term, you will need to adhere to a pre-agreed budget as set out in terms of the IVA.

- If you receive additional income or a bonus from your employer, your Insolvency Practitioner may insist this pays into the IVA on top of your regular monthly contribution.

What Happens to Any Assets I Own if I Get an IVA?

- When you enter an IVA, your appointed Insolvency Practitioner will ask for a list of any asset as part of the Statement of Affairs. It does not mean that the assets you own will necessarily include in an IVA.

Every IVA specifically tailors to your circumstances, and usually, you will keep assets such as your house and your car. If however, you own two vehicles, you will need to justify this with the Insolvency Practitioner who may insist you sell one vehicle and the proceeds paid into the IVA.

Throughout the IVA, further assets received such as an inheritance need to be declared to the Insolvency Practitioner who will need to assess whether any of the asset’s value needs paying into the IVA.

- You cannot apply for new finance above £500 during the IVA.

- The Insolvency Service will record your IVA on the IIR (Individual Insolvency Register) which can be accessed by the general public and contains personal details of those with an IVA against their name.

- Your job may be at risk if you enter into an IVA and to make sure it does not happen, it is vital to check your employment contract before any application.

- If you miss any payments, the Individual Voluntary Arrangement extends to make up the shortfall.

- From the date that the IVA commences is the date that your credit rating is affected. It will remain on your credit file and impact your credit score for six years.

- For the IVAs term, you will need to adhere to a pre-agreed budget as set out in terms of the IVA.

- If you receive additional income or a bonus from your employer, your Insolvency Practitioner may insist this pays into the IVA on top of your regular monthly contribution.

Summary

For a single mum, unless disciplined, finances can quickly become unmanageable, putting both mum and family under pressure. It may be possible to get your finances in check through budget planning before any damage is done.

However, for a mother that is already struggling under a debt pile, it may be time to consider a debt management plan to deal with your outstanding loans head-on. A debt adviser from the National Debt Service will be able to provide proper advice on the path forward.