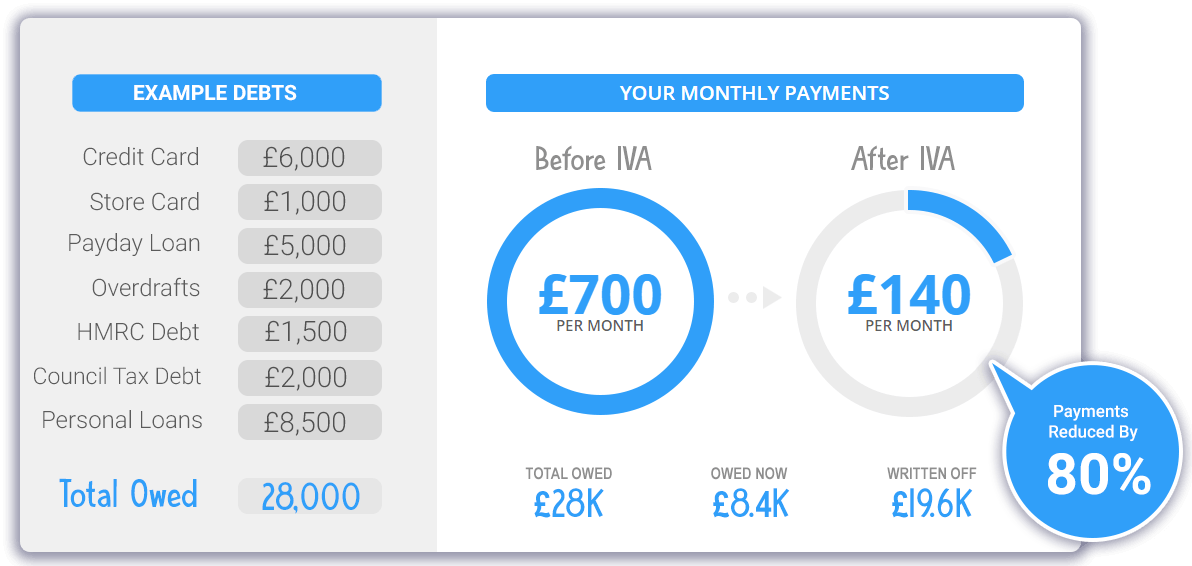

We can help you write off up to 80% of your personal debt

Furthermore, We can help you consolidate all your debts into one affordable payment without you having to borrow any more money or more importantly having to go bankrupt.

Key BENEFITS:

- Government-approved solution

- Freeze interest and charges

- Consolidate debts into one affordable payment

- Protect your assets

No upfront fees

100% confidentiality

Best help guaranteed

Exceptional reviews

Jubilee Can Help You Find A Debt Solution That Suits Your Needs

Struggling to pay your unsecured debts?

Are you struggling to pay your unsecured debts?

Have you had a big change in your personal circumstances?

A reduction in your income? Separated from a partner? Or just poor money management?

Contact us today if you are juggling your finances, overcommitted or have had a big change in your personal circumstances.

Don’t bury your head in the sand, we can help you!

Which debt solution is the most appropriate for you?

Are you in debt over £6,000? Can you afford to pay at least £100 a month towards your credit commitments or £23.88 per week?

We offer government approved debt solutions and you may qualify for an IVA. To qualify for an IVA 75% or more of your creditors will need to approve in terms of debt value.

If approved our debt solutions will legally freeze all your interest and charges and consolidate your debt into one single affordable weekly or monthly repayment.

We can help stop your creditors chasing monies owed and allow you to pay the debt back usually over 5 years. Any money you still owe after this period is then legally written off.

The quickest and easiest way to check if you qualify is to contact us by our online form, which will tell you how much of your debt you could write off and how to proceed. Our friendly experienced team of debt experts are qualified to support you on your debt free journey every step of the way.

Lower monthly repayments.

No more calls from creditors.

An IVA may be an available to you.

Frozen interest and charges.

Our Product Main Benefits

As well as the benefits listed here we are also able to offer protection from unsecured creditors.

A fixed agreement typically lasts about 5 years.

Get help with all types of unsecured debt

We can help you manage debts with some of the biggest UK creditors

Check to see which three Debt Solutions we may be able to help you with:-

Debt Management Plan (DMP)

A Debt Management Plan (DMP) allows you to pay off your unsecured debts in full over a longer period of time with a weekly or monthly payment you can reasonably afford. It is suitable for anyone who has unsecured debts such as credit and store cards, overdrafts and personal loans. We help you work out an affordable monthly or weekly payment and liaise with your creditors to set this up. For a free DMP assesment please click here.

Individual Voluntary Arrangement (IVA)

An Individual Voluntary Arrangement (IVA) allows you to consolidate all your unsecured debts into one affordable weekly or monthly repayment over 5 years. For an IVA to be approved 75% or more of your creditors in terms of debt value will need to approve the IVA proposal. If your creditors approve an IVA the interest and charges are legally stopped and frozen and usually up to 85% of the debt written off. For a free IVA assessment please click here.

Protected Trust Deed (Scotland Only)

A Protected Trust Deed (PTD) is only available to residents of Scotland. It is a formal arrangement between you and your creditors to have one affordable weekly or monthly payment over 4 years. If your creditors approve a Trust deed the interest and charges are legally stopped and frozen and up to 85% of the debt written off. For a free Scottish Deed assessment please click here.

How debt collection agencies or debt collection companies have changed their tactics to recover your cash!

It is a new era for the modern-day debt collection agency or debt collection company such as Lowell, Arrow Global, Cabot Financial, Hoist any many others.

The old school pressuring and bullying tactics debt collectors used to employ such as frequent phone calls sometimes made to your workplace and empty threats have been stamped out by the FCA (Financial Conduct Authority) and replaced with new Treating Customers Fairly policies and identifying vulnerable customers especially with mental health issues.

Have debt collection companies gone soft?

Debt collection agencies such as Lowell usually buy debt from telecommunication suppliers such as EE, Vodaphone, O2, BT & SKY but also collect on behalf of catalogue companies and credit card companies such as Vanquis, Marbles, Capital One and Aqua card.

If you miss payments or default on a credit agreement, then typically the bad debt is referred or sold to a debt collection company and you are issued with a default notice under the 1974 Consumer Credit Act. This will stay on your credit report for 6 years.

If you ignore debt collection companies and bury your head in the sand, then they usually refer you to a solicitor to issue legally proceedings to recover the outstanding monies owed. Lowell Portfolio usually refer to their inhouse solicitors called Lowell Solicitors who issue county court judgements (CCJS) or apply for an attachment of earnings and contact your employer or via your Universal Credits.

If I owe money to a debt collection company what should I do?

Contact us today to see how we can help you consolidate all your debts into one affordable weekly or monthly payments and stop debt collection companies and agencies contacting you and taking further legal action. Our government-approved debt solutions can stop all interest and charges applied by the debt collectors and all letters and phone calls.